We’ll cut right to the chase.

Capital structure matters.

For young public companies, understanding who owns the shares and at what price is even more important to stock prices than correctly forecasting the fundamentals of the business.

In an effort to figure out what is going on “under the hood”, we dove deep into the capital structure of the largest cannabis stocks to provide a visual guide to share dilution in the cannabis industry.

What we learned:

- Future stock sales could be an anchor on the stock price of companies with lots of dilutive “options” (warrants, convertible debt etc.)

- A stock trading well above the option strike price could come under pressure once those shares go free trading and insiders sell to lock in big gains.

- A stock trading below the option strike price doesn’t have to worry about near-term insider selling pressure, but could have its upside capped.

- Buy stocks with low dilution, options not yet in the money and fast revenue growth.

- Avoid stocks with heavy dilution, options deep in the money and slow revenue growth.

Why Cheap Stock is a Weight on Stock Prices

Dilutive securities, whether they are options, warrants, or convertible bonds, all serve as an anchor tethering the stock price to the conversion price of the options.

To understand why, you need to put yourself in the shoes of an early investor.

Unless you are looking at a high-flying tech stock with professional venture capitalist backers with 5-10 year time horizons, many of the early backers are likely rich people simply looking to grow their money as quickly as possible.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]For high net worth investors in a $10 stock sitting on warrants that convert at $0.50, it can be very hard to justify why they shouldn’t sell their shares today and realize a 20x gain instead of waiting for an additional 1x-2x upside which could take months or even years.[/su_panel]Cheap shares do two things:

- When the stock price is far above what insider’s paid, insiders have an incentive to sell to lock in big gains. This selling pulls the stock price down towards the cost basis of the insiders.

- Lots of cheap stock priced at or above the current stock price will act as an anchor on any increase. Insiders convert their options and sell anytime the stock creates a juicy return opportunity by going too far above their cost.

Early Investors can be a Blessing or a Curse

Early investors, including founders, are the ones who help companies get off the ground.

Without their startup capital, most cannabis stocks would have never made it to the public markets.

For companies with early investors who share the founders’ long-term vision, these first investors provide stability to the shares and potentially a source of additional cash down the road.

However, if investors are only in it for a quick flip, they may look to sell early on to lock in significant profits instead of waiting for the company to mature.

Insider selling can quickly become an anchor on stock prices as early investors own millions of shares, compared to daily volumes of 400,000 shares for the average stock in this report.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]If early investors have a cost basis of $1 while the stock is trading at $10, they don’t care if they push the price down to $9 due to their heavy selling volume, they still are making a killing. Only recent investors feel the pain as they are now sitting on a 10% loss. [/su_panel]Cheap shares on their own aren’t a problem. Any company not in financial distress will have issued shares far cheaper than the current market price.

For companies with years of profitable operations under their belts, dirt cheap founder shares have already changed hands multiple times or are locked up in a vault in an effort to maintain insider control of the company, ala Jeff Bezos or Sergey Brin.

The closer a founder’s cost basis is to the current stock price, meaning the lower his potential gain, there is less incentive for insiders to sell.

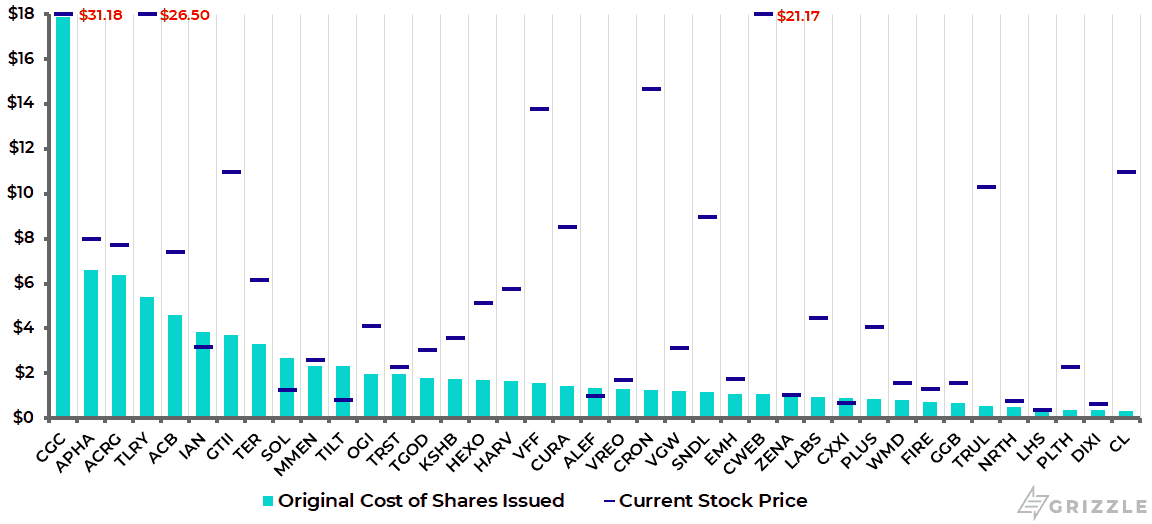

Thanks to the magic of financial disclosure, we can tell how close current share prices are to the cost basis of insiders (presented below).

There are three main takeaways from the chart:

- All companies issued low-cost shares to early investors, but the more stock a company issued after its IPO the higher the cost basis is all else equal.

- Years since IPO matters more than the original cost of the shares. Over time insiders who want to sell, do, and those that remain believe in the upside of the business and plan to sell shares only sparingly. In general, larger Canadian LPs are well past share lockup, while CSE stocks with short trading histories have to contend with insiders sitting on gains and future share dilution from options.

- If the current stock price is below the cost of insider shares and the stock isn’t in financial trouble, selling pressure is likely close to peaking.

What Insider Shares Cost Compared to the Current Stock Price

Early Fundraising Continues to Impact Future Stock Prices

The first companies to enter the cannabis space knew they were fighting for a piece of a massive global market.

To make sure they had a seat at the table, everything had to be done fast; construction, product creation, distribution, and most of all, sales growth.

But speed comes at a cost, in this case quite literally.

Cannabis companies needed cash and lots of it and they raised these funds by issuing shares, options, warrants and most recently debt that has the option to convert into shares.

They were effectively borrowing from the future to pay for the present.

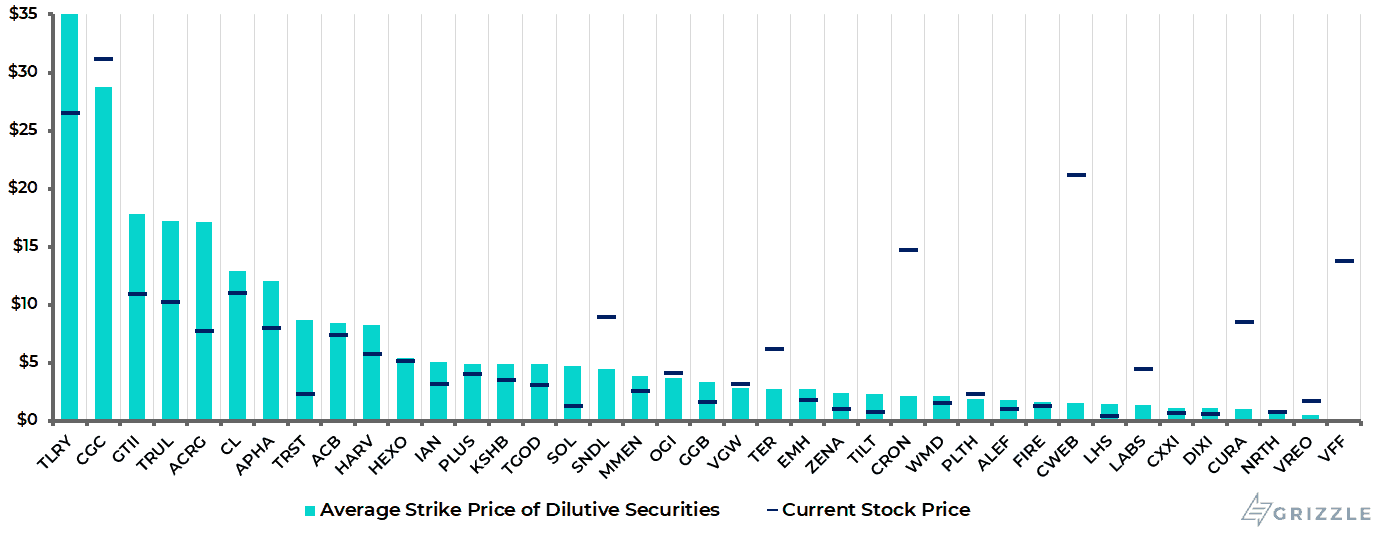

As these companies grow, pushing the stock price higher, the options are converted at one price and can now be sold in the open market for a much higher price, creating continued selling pressure.

The deeper in the money an option is, the higher the chance it will be converted and sold for cash.

In the chart below you are looking for a stock price at or below the strike price of dilutive shares.

Average Strike Price of Dilutive Shares Compared to the Current Stock Price

A stock price much higher than issued options isn’t a bad sign on its own and only makes up one piece of the puzzle.

The other, more important piece is to know how many dilutive securities have been issued.

Stock A: Trading for $10.00 with $1 warrants that add 5% to the share count

Stock B: Trading for $3.00 with $1 warrants that add 30% to the share count

Answer: Stock A is a much better buy because of the small amount of dilutive stock that can be issued. Even though the $1 warrants are deeper in the money than for stock B they can likely be sold in the open market by insiders without moving the stock price very much.

The problem with warrants and convertible debt as a borrowing vehicle is they create a block of shares that will likely be sold into the market instead of held for the long term.

Lenders aren’t interested in becoming a part-owner of a cannabis business. They would rather collect their interest and move on to the next lending opportunity.

Volume and Cheap Shares Go Hand in Hand

Where cheap shares create problems is when a stock’s volume isn’t high enough to accommodate sales of all those diluted shares. In this scenario, share supply will outweigh demand and cause the stock price to fall.

Putting it all together, the table below looks at how many days it would theoretically take investors of each company to sell their dilutive securities based on the company’s average volume.

Company’s with low volume and lots of options could see a fall in their stock price if insiders sell too many shares at once.

Like concertgoers all trying to squeeze through one exit door, too many sellers with not enough volume can potentially do a number on the share price.

| Ticker | Average Daily Volume (‘000) | Total Dilutive Shares (‘000) | Days it Would Take to Sell all Dilutive Securities at the Current Daily Volume |

| TER | 41 | 45,100 | 1,097 |

| TILT | 450 | 268,771 | 597 |

| CL | 200 | 118,405 | 592 |

| HARV | 400 | 137,531 | 344 |

| VREO | 75 | 24,686 | 329 |

| MMEN | 500 | 164,005 | 328 |

| ALEF | 454 | 138,081 | 304 |

| DIXI | 167 | 45,685 | 274 |

| CXXI | 200 | 52,554 | 263 |

| FIRE | 556 | 122,806 | 221 |

| IAN | 350 | 75,364 | 215 |

| PLUS | 55 | 11,489 | 209 |

| GGB | 350 | 62,429 | 178 |

| LHS | 300 | 52,676 | 176 |

| ACRG | 96 | 16,370 | 171 |

| PLTH | 150 | 20,453 | 136 |

| SOL | 100 | 10,575 | 106 |

| ZENA | 634 | 63,770 | 101 |

| CURA | 450 | 39,725 | 88 |

| WMD | 338 | 22,087 | 65 |

| TGOD | 1,410 | 81,584 | 58 |

| NRTH | 632 | 29,807 | 47 |

| EMH | 433 | 18,091 | 42 |

| KSHB | 414 | 16,412 | 40 |

| GTII | 200 | 6,500 | 32 |

| VGW | 568 | 17,343 | 31 |

| LABS | 1,080 | 22,942 | 21 |

| SNDL | 2,150 | 40,827 | 19 |

| CWEB | 507 | 7,423 | 15 |

| HEXO | 3,740 | 51,298 | 14 |

| CGC | 4,120 | 55,234 | 13 |

| ACB | 12,000 | 159,561 | 13 |

| APHA | 4,580 | 47,398 | 10 |

| OGI | 1,100 | 10,621 | 10 |

| TRUL | 200 | 1,470 | 7 |

| TLRY | 1,550 | 11,063 | 7 |

| CRON | 4,590 | 32,055 | 7 |

| VFF | 885 | 4,809 | 5 |

| TRST | 2,420 | 10,593 | 4 |

We think the days to sell numbers in the table above are actually higher in real life.

There are other people besides insiders who want to sell the stock for one reason or another, so to assume an insider will be the only one selling is very naive.

If we were being conservative, we’d say the days to sell is at least double what the table above implies.

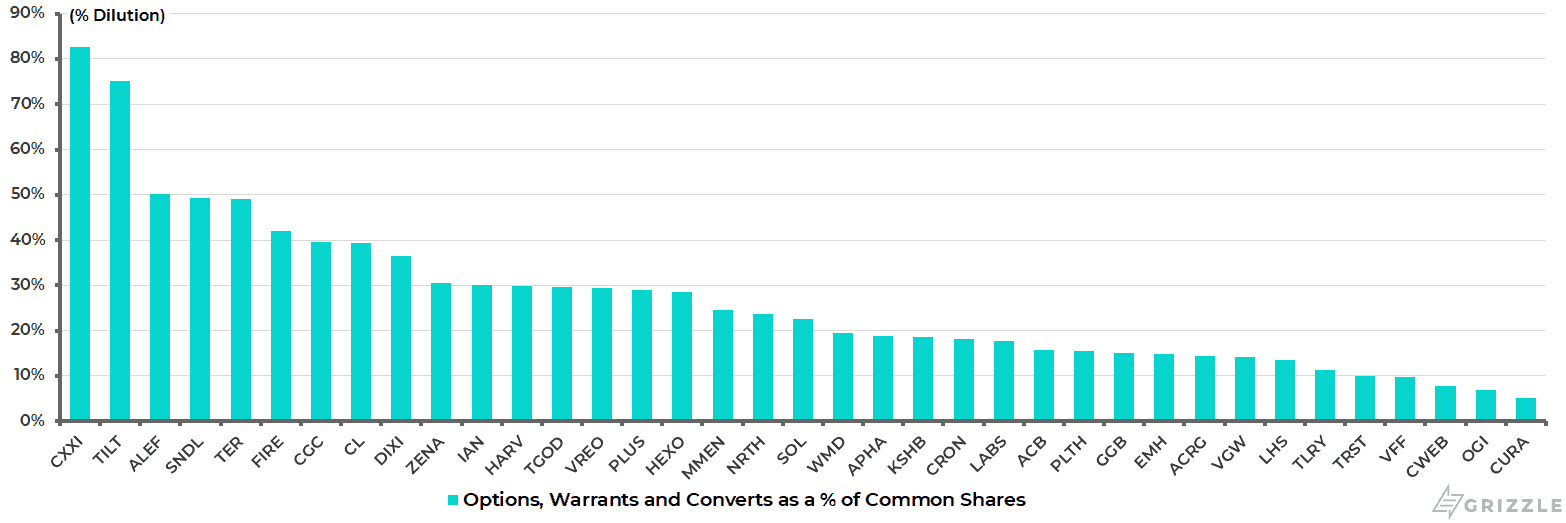

Options Warrants and Convertible Bonds as a % of Basic Shares

Cheap Shares Don’t Automatically Kill A Stock

This article may make it sound like cheap shares automatically ensure no stock can ever go up, but in reality, every stock once had cheap founder’s shares, even global leaders like Amazon, Apple, and Google.

The stock price of real companies with real business models can go up even with early investors and lenders holding cheap shares, warrants and convertible debt.

Companies that consistently grow revenue and earnings make their shares more valuable and as a result, early investors can successfully sell their shares to new investors for far more than they paid.

Solid companies also draw increasing interest from institutions that push up trading volumes, allowing large insider stock sales to take place with a minimal impact on prices.

At the end of the day, we recommend you use the data in this report to identify companies with the following characteristics:

- As few dilutive securities as possible.

- Longer than a year of trading history to ensure all early investors who wanted to sell out have already done so.

- Rapid revenue growth and a business model you believe in.

- A strike price for warrants/converts above the current stock price so both lenders and management are incentivized to push the stock higher not lower.

Find a company that checks all these boxes and you are setting yourself up well for consistent share price gains.

Is Cheap Stock to Blame for the Recent Industry Selloff?

The ongoing selloff in cannabis stocks is driven by far too many factors to say cheap shares and insider selling is solely to blame, however, we think this capital structure data may provide some clues about when the selling may stop.

A stock trading below the average strike price of dilutive securities and near the average cost of founder’s shares is closer to the end than the beginning of its decline unless the global economy takes another turn for the worse.

With many stocks in our charts showing these two characteristics, late August could go down as an ideal time to choose the stocks you believe in and build a position.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.