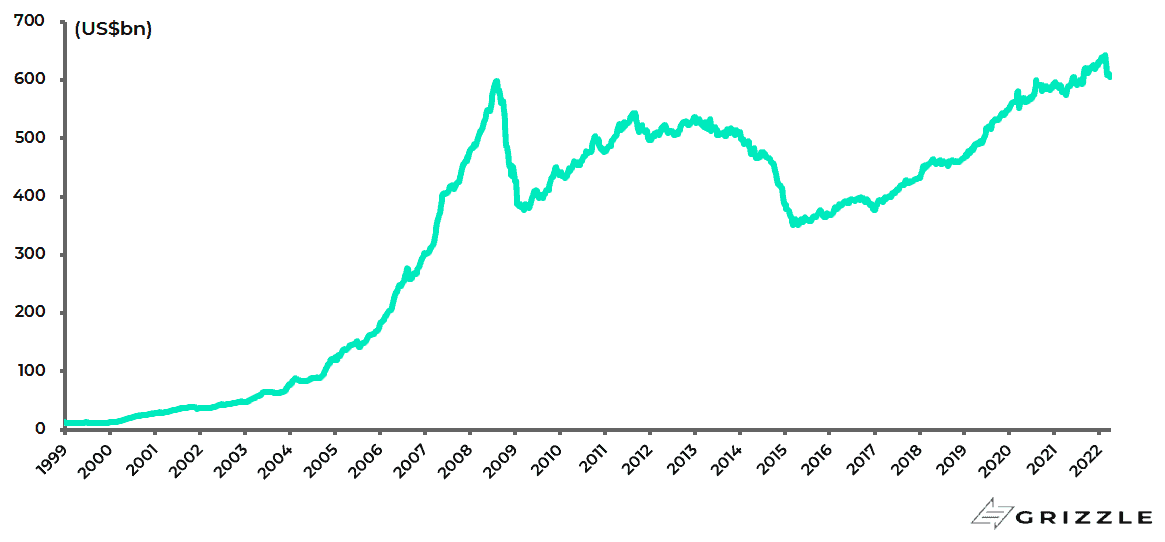

There is an air of Western triumphalism in the air as regards the effectiveness of Western sanctions against Russia, most particularly the freezing of Russia’s US$609bn of foreign reserves.

Russia international reserves

A good example of this is a recent op-ed article in the Washington Post (“War in Ukraine has created a new financial weapon in the West” by Sebastian Mallaby, 2 March 2022)

There is no doubt that the weaponisation of the US dollar is an extremely powerful tool for the US to employ.

The latest American move follows a number of other similar measures in recent years with the first this writer can remember the US$8.9bn fine levied on French bank BNP Paribas back in 2014 for dealing with Iran.

Still, it has to be wondered about the longer term ramifications of this latest move, and how other countries with large foreign exchange reserves will view the matter if, one day, they are suddenly deemed to be out of favour in Washington.

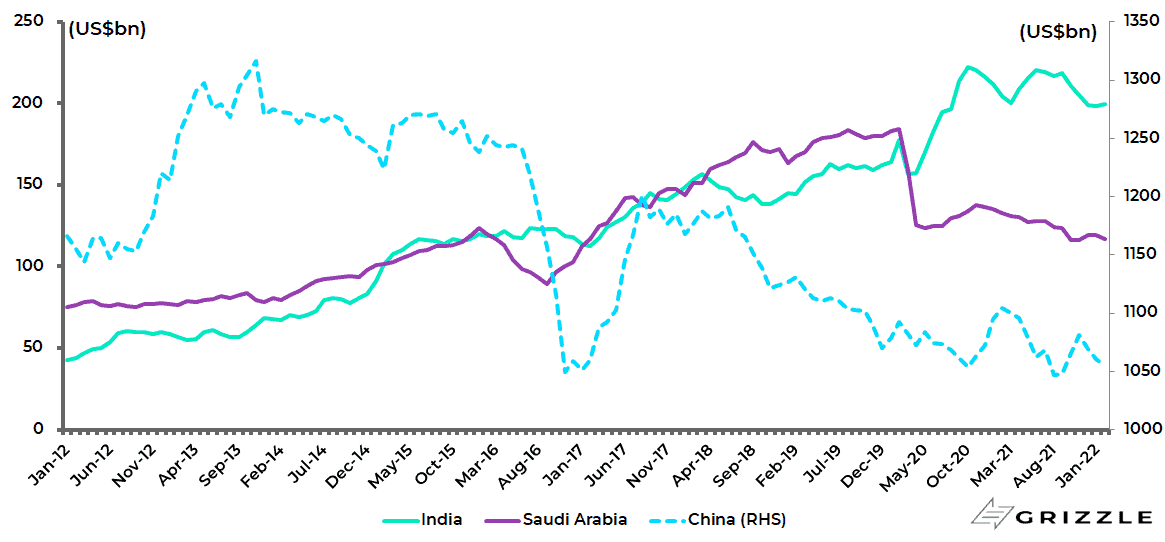

This is not just a reference to China (US$3.2tn of foreign exchange reserves) but also, for example, Saudi Arabia (US$441bn of reserves) and India (US$604bn of reserves).

Interestingly, both China and India abstained from the UN vote last month demanding Russia immediately end its military operation in Ukraine.

Yet all these three countries still have a substantial portion of their foreign exchange reserves in US Treasuries.

China, India and Saudi’s holdings of US Treasuries totaled US$1.05tn, US$200bn and US$117bn respectively at the end of February.

China, India and Saudi Arabia holdings of US Treasury securities

They also have probably much larger exposure to the US dollar, as a percentage of their reserves, than was the case with Russia.

There is, consequently, a growing possibility that foreign exchange reserves denominated in dollars may be making a long term peak as countries question the value of accumulating such “assets”, which at the end of the day are a claim on someone whereas ownership of gold bullion, or indeed Bitcoin, is an IOU on nothing.

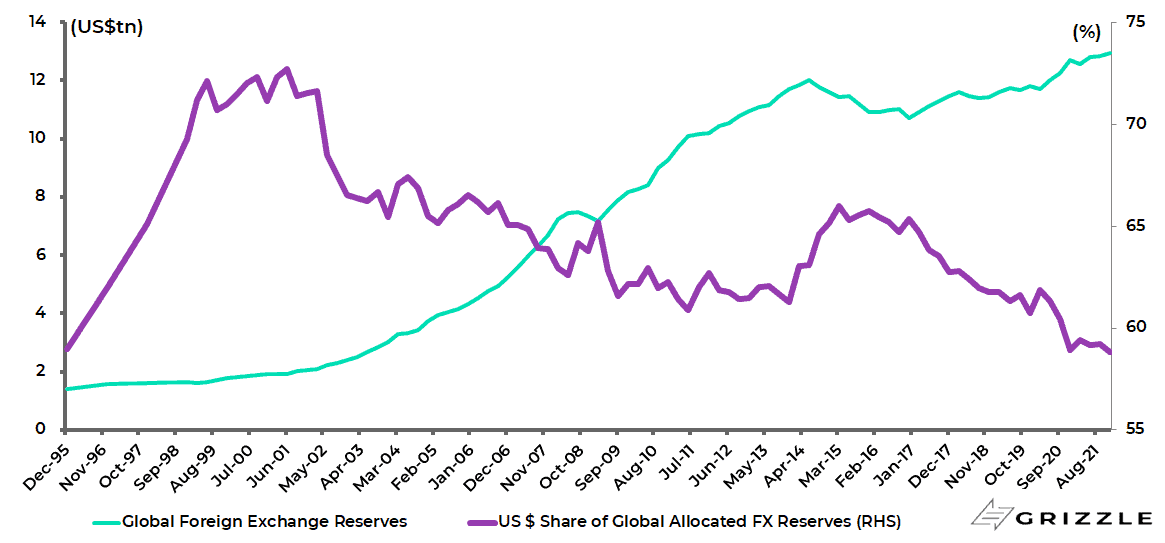

For the record, global foreign exchange reserves rose to a record US$12.94tn at the end of 4Q21, the latest data available, while the US dollar’s share of world FX reserves declined to a 26-year low of 58.8% at the end of 2021, according to the IMF.

Global foreign exchange reserves and US dollar’s share

Does Quantitative Easing Really Protect the US From a Foreign Bond Buying Strike?

China has been advocating a move to a global currency system based on the SDR ever since 2009 when then PBOC Governor Zhou Xiaochuan wrote an article published by the BIS saying that the US was abusing its privileged position as the issuer of the world’s reserve currency by launching quantitative easing, a policy Beijing has always criticised (see BIS article: “Reform the international monetary system”, 23 March 2009).

Yet Mallaby, the author of a distinguished biography of Alan Greenspan, views quanto easing as having given Washington an additional weapon in terms of any threat by China to dump its Treasury bonds.

He argues that quantitative easing demonstrated how the Fed “could print money and buy the bonds that China wanted to sell”.

The result he says is increased “creditor impotence” in the sense that creditors, such as Russia, no longer have leverage whereas what matters is having a financial system that commands global trust, based on an independent central bank and an independent legal system.

This writer would beg to differ on all counts.

In the long term, trust in the US system will have been diminished in many parts of the world, in terms of the willingness to hold US dollar assets as a result of the latest action; while it cannot be assumed, as regards quanto easing, that markets will never question central bank credibility if central bank balance sheet expansion continues.

Indeed that is one reason why some Fed governors are anxious to reduce the size of the Fed balance sheet from the current size of US$8.97tn and why quantitative tightening is, for now at least, back on the Fed’s agenda.

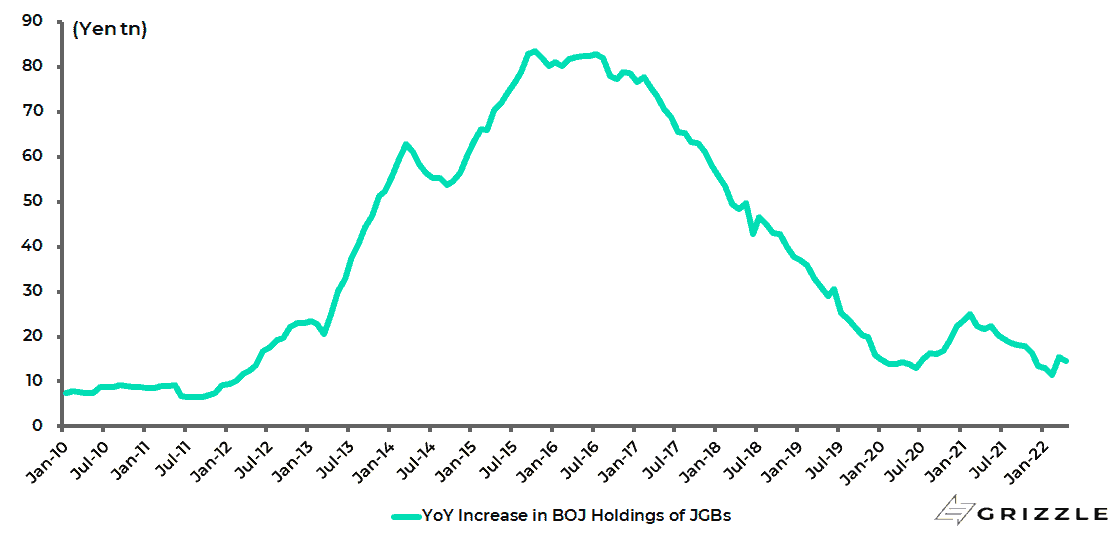

It is also the reason why the Bank of Japan had, until the past three weeks, reduced dramatically the scale of its JGB buying in recent years.

YoY increase in Bank of Japan’s holdings of JGBs

This is because the Japanese central bank is in danger of reaching the practical limits of that policy given that it owns 48% of JGBs outstanding and given that it is not, by law, meant to engage in debt monetisation.

Ukraine has caused the delinking of Russia and China from the US Money System

Meanwhile, the seeming de-linking of Russia, the world’s third-largest oil producer, from the US dollar system should prove a major catalyst in terms of the efforts already underway by both China and Russia to reduce their dependence on the dollar in terms of trade.

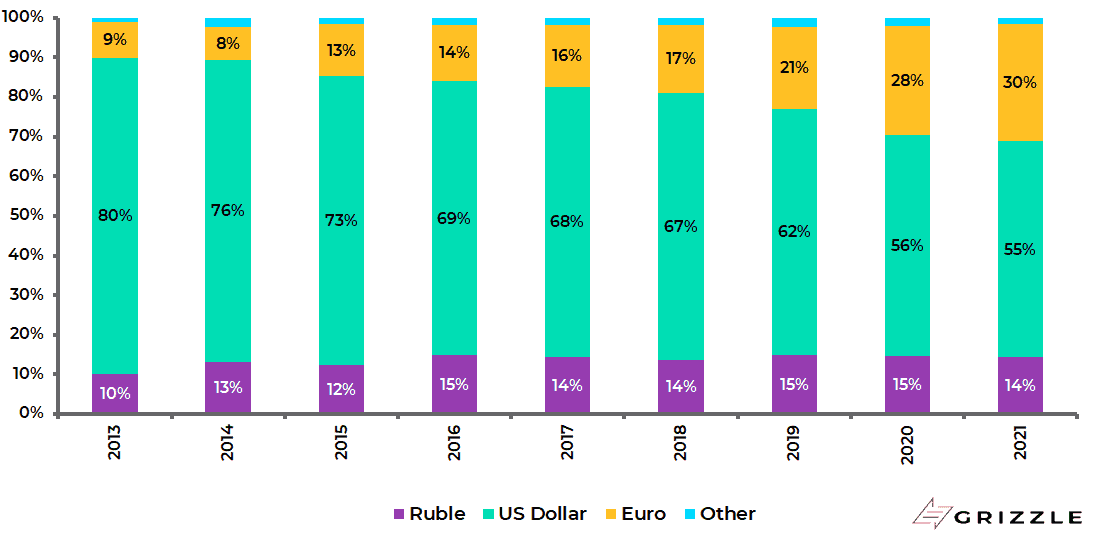

The US dollar’s share of Russian export receipts has declined from 79.6% in 2013 to 54.5% in 2021, while the euro’s share has risen from 9.1% to 29.7% over the same period, according to the Bank of Russia.

Share of Russian exports by currency

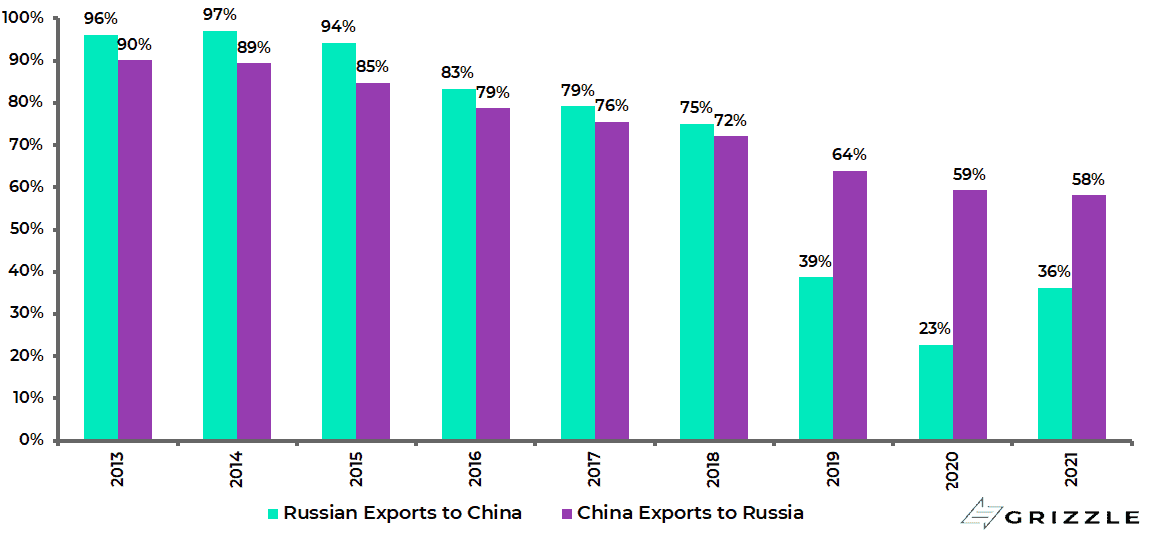

Similarly, the dollar’s share of Russian exports to China has declined from 96% in 2013 to 36% in 2021, while the dollar’s share of China exports to Russia is down from 90% to 58% over the same period.

US dollar’s share of Russia-China bilateral trade

This writer’s longstanding base case is that the capital account is likely to remain closed so long as China is run by the Communist Party.

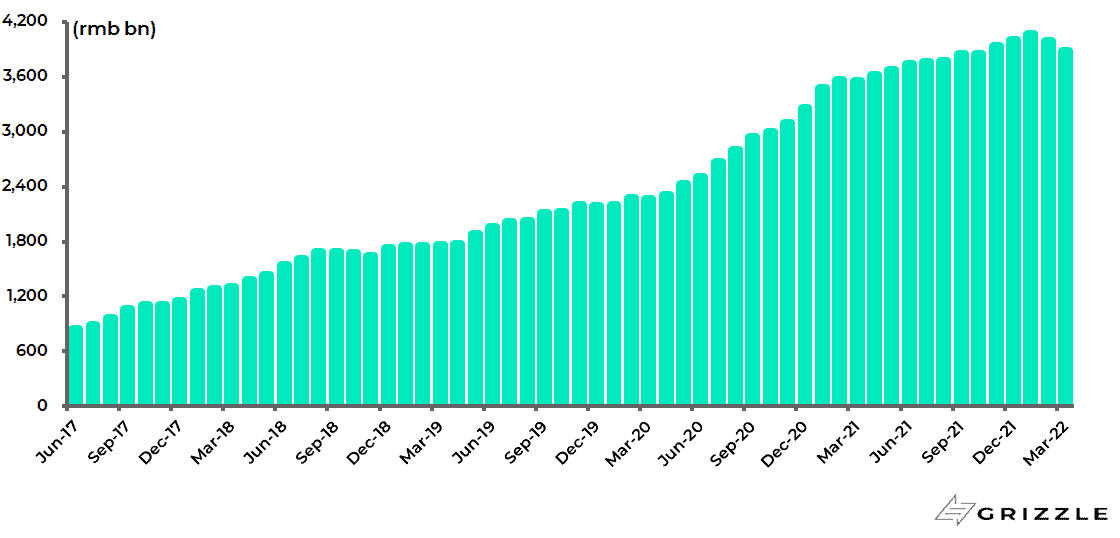

Still, China has been developing its own bond market as an alternative reference point for fixed income investors, and foreign flows into China bonds, particularly government bonds, have continued until of late.

Foreign holdings of China bonds increased by Rmb749bn in 2021 and by Rmb66bn in January to a record Rmb4.07tn at the end of January, though they have fallen by Rmb193bn in the past two months to Rmb3.88tn at the end of March.

Foreign holdings of China bonds

Indeed China bonds have done a much better job preserving capital in US dollar terms than have G7 government bonds since the onset of the pandemic.

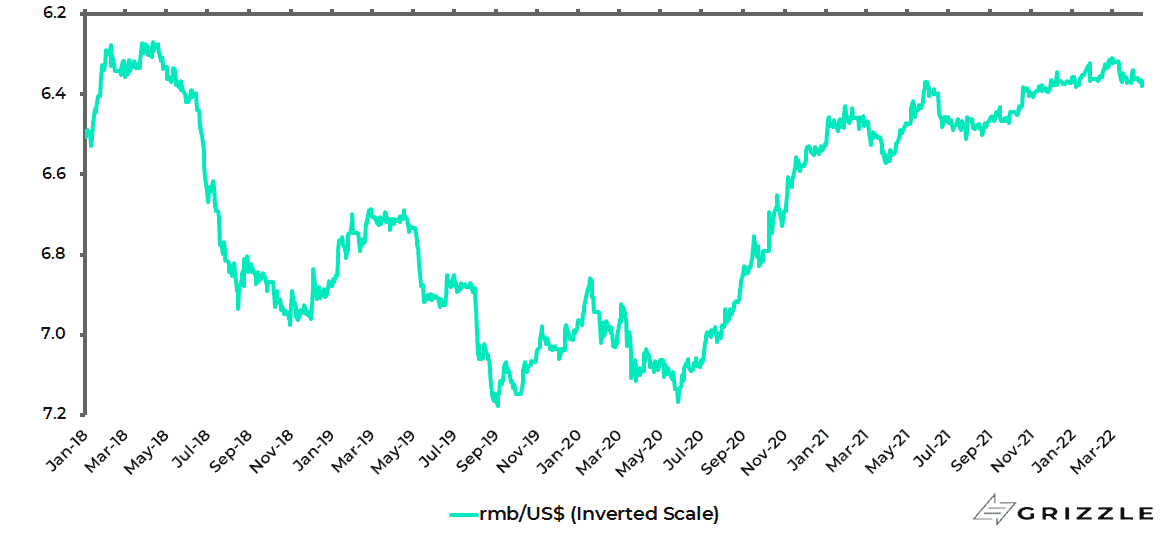

It should also be noted that the renminbi has remained stable despite the “risk off” dollar rally triggered by the Russian invasion of Ukraine.

The renminbi has depreciated by only 0.2% against the US dollar so far in 2022, after appreciating by 2.7% in 2021 and 6.7% in 2020.

This safe haven action again confirms the PBOC’s status as the nearest thing the world now has to the old Bundesbank.

Renminbi/US$ (inverted scale)

Low Inflation in China Leaves Room for Interest Rate Cuts

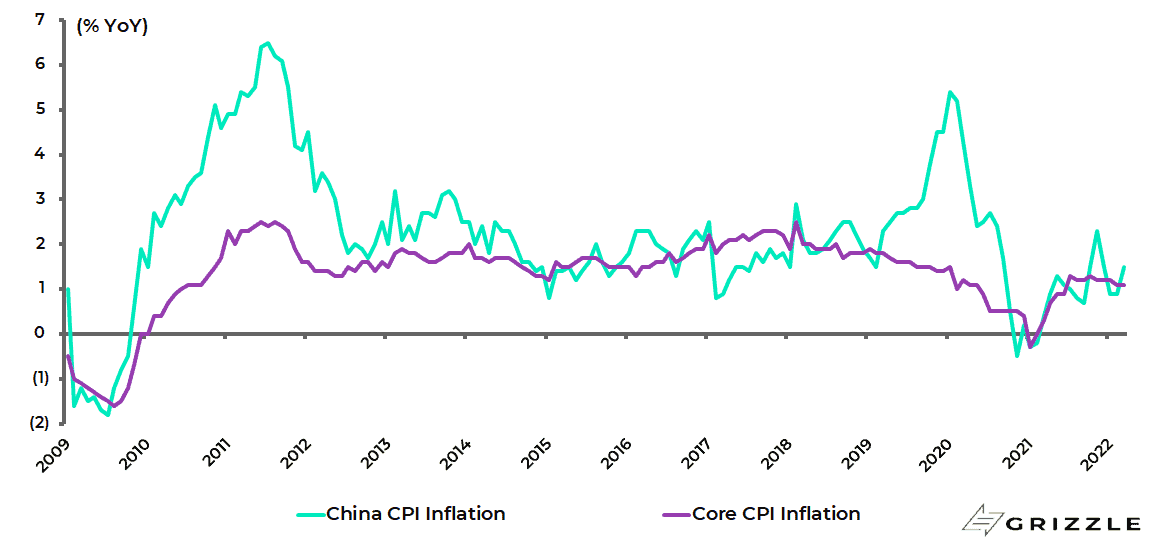

It also remains the case that, in stark contrast to the G7 world, inflation in China remains conspicuous by its absence.

This is why China now has room to ease.

China headline CPI rose by 1.5% YoY in March while core CPI was up 1.1% YoY.

China CPI inflation

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.