With the focus on Turkey and the potential related fallout in other emerging markets in recent weeks, it is easy to forget about the Eurozone. Yet the current Italian government is likely to trigger a renewed existential crisis in the Eurozone once the Europeans return from the beach and the Italian Government comes up with a budget for 2019 which is likely to put it in direct conflict with the Maastricht Treaty.

Broken Bridges Under the Euro

The collapse of a motorway bridge in Genoa last month resulting in 43 deaths, and Italian Interior Minister Matteo Salvini’s exploitation of that event by blaming Brussels-imposed austerity, is a reminder of what is coming.

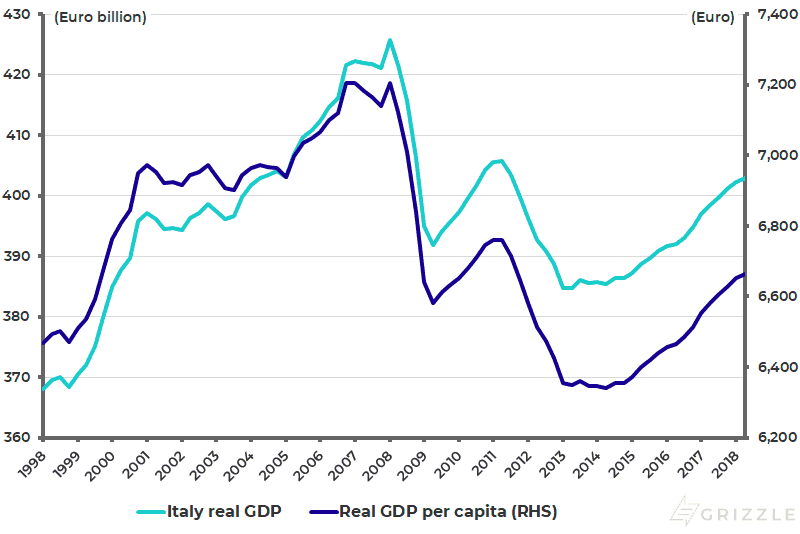

Having driven over that particularly rickety bridge on more than one occasion, this writer is not surprised to hear about what happened. Similarly, driving through Italy in recent years always serves as a reminder just how poor Italy has become under the euro. Remember, Italy has recorded almost no growth since the formation of the euro at the beginning of 1999, nearly 20 years ago. Italian real GDP has risen by only an annualized 0.4% since 1Q99 and is up only an annualized 0.1% in real GDP per capita terms over the same period (see following chart).

Italy Real GDP and Real GDP per Capita

The Italian issue is raised again in part because it is timely with the end of the summer holiday season. The view here remains that a systemic event in financial markets is more likely to be triggered by Italy and the Eurozone than other candidates currently discussed by pundits, be it a Donald Trump-triggered trade war, a much anticipated (by talking heads) Chinese currency collapse or overvalued Wall Street FANG stocks.

Still, they are all interconnected phenomena since, for example, a renewed focus on the existential risks in the Eurozone is likely to put renewed downward pressure on the euro which, if what happened in the second quarter is any guide, will then lead to broader US dollar strength against emerging market currencies. This will in turn make it more challenging for China to manage the capital outflow issue.

Burning the Bridge to Europe, Building a Bridge to the US

Returning to the Eurozone issue it is also important to remember what is easily forgotten in the financial markets. That is that the anti-euro, anti-immigration populists in Europe now have a supporter in the White House who is openly encouraging them to pursue their agendas. This is, of course, the exact opposite of what was the case under Barack Obama who, unfortunately, intervened in the Brexit debate in Britain with negative consequences for the ‘Remain’ cause he was supporting.

Donald Trump could not have made it clearer that he supports the cause of those in Italy wanting to leave the euro – just as he could not have made it clearer that he supports Brexit. This is not unimportant since a potential future decision by, say, Italy to walk out of the euro looks a lot less risky politically and economically if it has the support of the American president. This will be particularly the case if that particular American president’s political position has been strengthened by the outcome of the November mid-term elections. This is one reason, among many others, why those elections are becoming rather important. The base case here remains that the Republicans will maintain control of the Congress. But, clearly, that is not consensus.

It is also important to remember that Europe has its own upcoming election cycle. Grizzle refers again to the potentially hugely important May 2019 European parliamentary elections. While the focus of financial markets in the coming quarter will likely be on the Italian Government’s budget, and how Brussels and Berlin will respond, next May’s parliamentary elections are likely to be by far the most significant ever.

This is because the anti-euro populist parties are likely to run a far more coordinated campaign. The result could be the emergence of a populist alliance in the European parliament determined to attack from within many of the foundations of the Eurozone, be it the Maastricht Treaty in the economic sphere or ‘free movement’ in terms of the politically charged issue of immigration.

A reminder of this comes from reading a recent article on the growing activities in Europe of Steve Bannon, Trump’s former political strategist (see International New York Times article: “In Europe, a best friend for Bannon”, August 21, 2018 by Ivan Krastev). This article reported how Bannon announced in late July that he plans to establish in Europe a foundation, called The Movement, to create a formal alliance of populist right-wing parties ahead of next May’s European elections.

The mooted foundation will aim to provide polling and policy support. His main ally in Europe in this venture is, according to the same article, Hungarian Prime Minister Viktor Orban who was re-elected in April for his third consecutive four-year term.

Obviously, turning such an alliance into an effective political force is easier said than done, most particularly as there will be different views on specific policies. Still, there will be an easily achieved consensus among the populists on the related issues of immigration and Islam. On this point, the same article reports that Orban intends to make next May’s elections “a referendum on migration and Islam”.

The Shifting Tide of Immigration

This is where the renewed crisis in Turkey, with its focus on a collapsing currency and macro imbalances, meets the issue of European politics. This is, of course, because the main reason the flow of migrants into Europe, and in particular Germany, has declined significantly since late 2016 due to the EU-Turkey migration deal Angela Merkel negotiated with Turkish President Recep Tayyip Erdogan in March 2016.

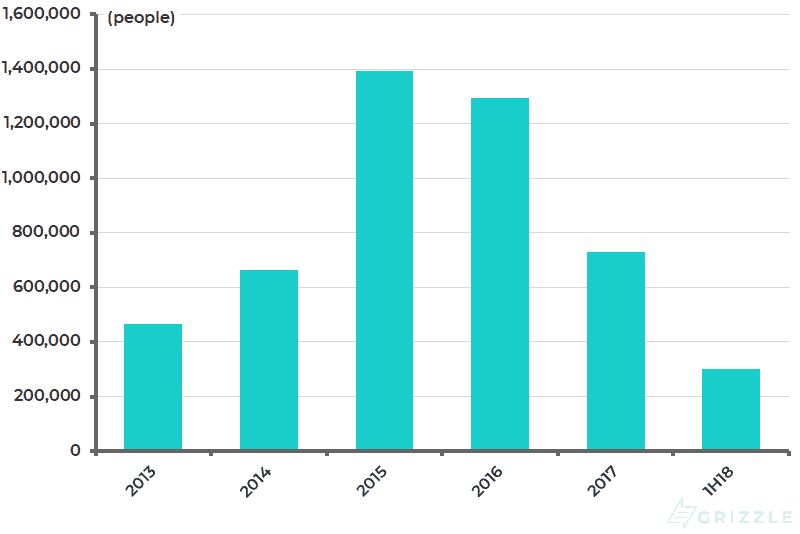

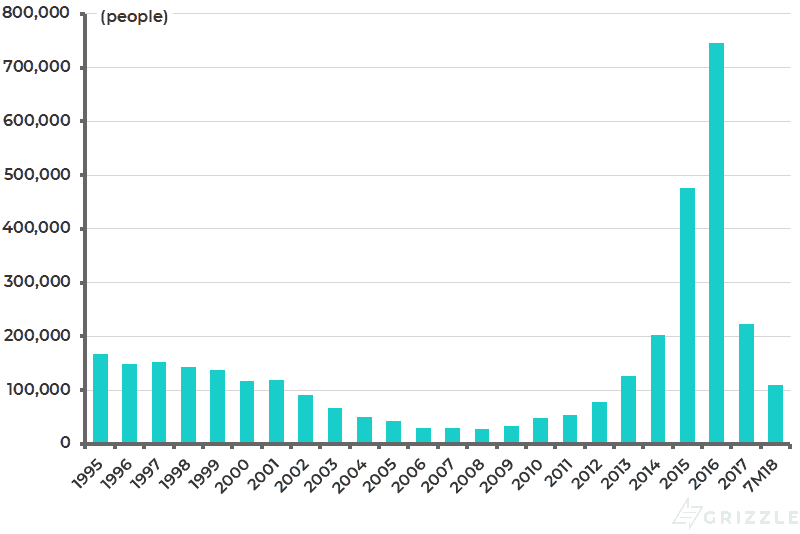

Under the deal, the EU agreed to pay Turkey €6 billion to halt the human flow with some 3.5 million Syrian refugees remaining in Turkey. As a result, the number of asylum applications lodged in Europe declined by 44% YoY to 728,470 people in 2017 and were down 15% YoY to 301,390 in 1H18, according to the European Asylum Support Office (see following chart). As for Germany, total asylum applications declined by 70% from a peak of 745,545 people in 2016 to 222,683 in 2017 and were down 15% YoY to 110,324 in the first seven months of 2018, according to the Federal Office for Migration and Refugees (see following chart).

Asylum Applications Lodged in Europe

Germany – Total Number of Asylum Applicants

The above creates obvious leverage for Erdogan to apply against Merkel and the Eurozone. This explains why Merkel in her public comments has taken a conciliatory tone in response to recent developments in Turkey in stark contrast to the provocative posture adopted by the Donald Trump.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.