Italian Politics – A Perpetual State of Turmoil

The focus has returned to Italian politics in recent weeks and the potential for a renewed Eurozone crisis. The first development was an initial realization that there could be another general election in July, only four months after the previous election on March 4.

This occurred when the Five Star Movement and the League (formerly the Northern League) indicated they did not support the proposal, made on May 7 by Italian President Sergio Mattarella, for a ‘neutral’ caretaker government to hold power for the rest of this year.

Such an outcome would involve a replay of the initiative by the previous president Giorgio Napolitano, installing former EU Commissioner Mario Monti as Italian prime minister in 2011 in the midst of the Eurozone crisis.

Monti’s caretaker government lasted 17 months, though it never had democratic legitimacy. This is exactly why both Five Star and the League, both viewed as ‘populists’ by investors, oppose the latest proposal for a ‘neutral’ (i.e. pro EU) government.

The issue now in Italy is whether a new election will be held, or even worse for markets whether Five Star and the League can form a government, a prospect which has now become a real possibility, if not probability.

The two parties’ leaders announced on Friday morning that they have agreed on a governing contract to form a coalition government, though they still have to pick a prime minister candidate and get the president’s approval.

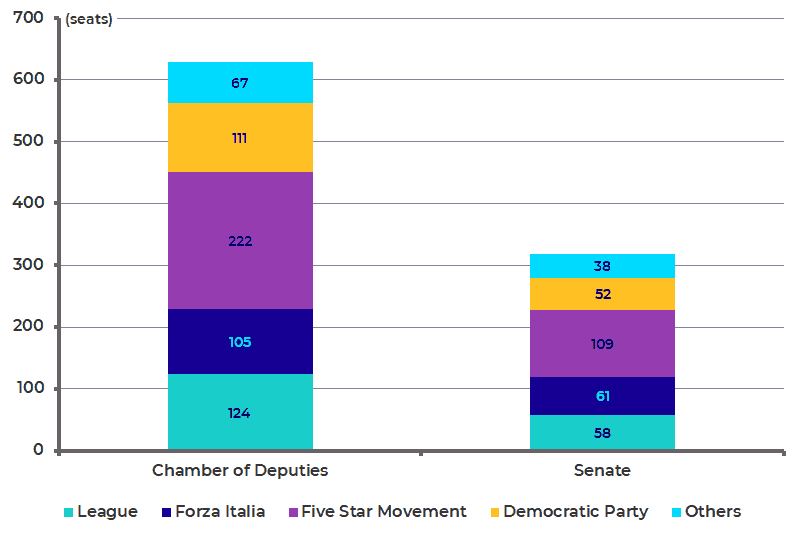

This scares investors because both parties have had a euroskeptical agenda. They certainly have the technical ability to form such a government since together they have a majority of seats in both houses of the Legislature. Five Star and the League together have 346 or 55% of the seats in the Chamber of Deputies (Lower House) and 167 or 53% of the seats in the Senate (see following chart).

If they want to achieve constitutional changes, such as exiting the Eurozone, they need a two-thirds majority in the legislature. This becomes possible, if the Forza Italia (aligned with former Italian Prime Minister Silvio Berlusconi) votes with them.

Italian Parliament Current Composition

Bond Investors have been Sanguine to the Risks

All of the above has only now started to be appreciated by investors given the remarkably low level of Italian government bond yields that have prevailed until recently in spite of the populist surge in the last general election and the continuing failure to form a new government since then.

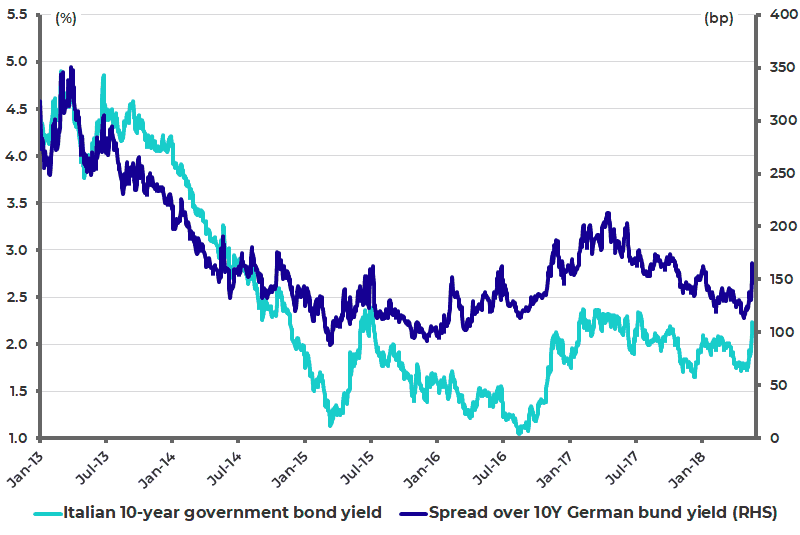

Indeed, the yield on the 10-year BTP, the acronym used for Italian government bonds, declined to a low of 1.71% this year on May 4 though it has since risen by 52bp to 2.23%, while the spread against Germany’s 10-year bund yield has begun to widen again after reaching remarkably compressed levels.

Thus, the spread between the 10-year BTP yield and the 10-year bund yield declined from 213bp in April 2017 to a low of 114bp in late April and has since risen to 165bp (see following chart).

Italian 10-year Government Bond Yield Spread Over 10-year German Bund Yield

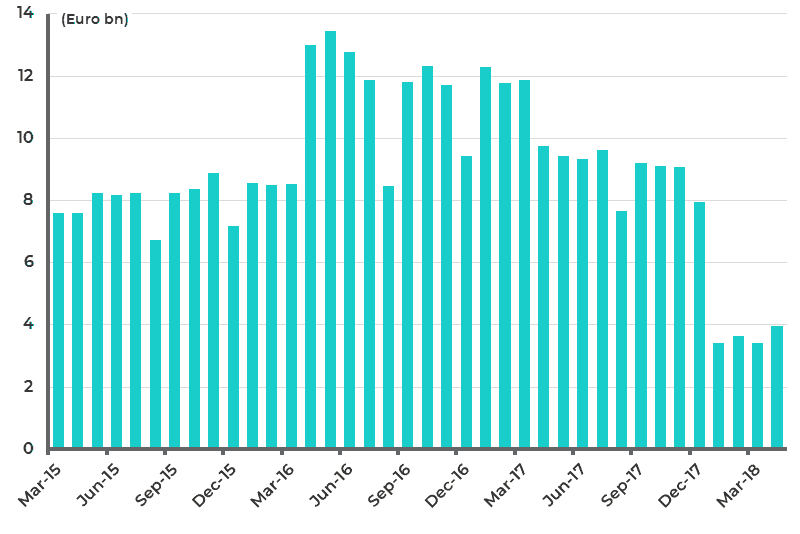

The reasons for investors’ delayed reaction are probably twofold. First, Italian politics are bewilderingly complex to outsiders. Second, there has been the anaesthetizing effect of the European Central Bank’s bond buying. The ECB is buying BTPs at an estimated rate of around €200m daily (see following chart).

ECB Monthly Net Purchases of Italian Government Bonds

Still it is clear that markets were far too sanguine given that the formation of a Five Star/League government could precipitate again an existential crisis in the Eurozone.

This is also the reason why it is not surprising that Frau Merkel has not wanted to embrace openly French President Emmanuel Macron’s agenda for a move towards greater fiscal integration until the issue of the formation of a new Italian government is resolved.

Germany: Running Surpluses and Resisting Eurozone Fiscal Integration

If fiscal integration in the Eurozone makes theoretical sense, given there is already monetary union, German resistance remains an issue. Yet, it is raining taxes in Germany with projected tax revenues over the next five years €63 billion higher than was estimated by the government last November.

Despite this the German government remains focused on achieving a fiscal surplus and cutting the government debt to GDP ratio below the 60% threshold set out in the Maastricht Treaty of 1992.

A Keynesian critique of this policy by German author Wolfgang Münchau was set out in the London Financial Times article, “Germany’s budget is an accident waiting to happen,” earlier this month.

The article notes correctly that Germany’s new SPD finance minister, Olaf Scholz, is proving about as conservative as his CDU predecessor, Wolfgang Schäuble.

The stated goal is to push the budget into a surplus of 1% of GDP or higher during 2019-2022, and for the government debt to fall below the 60% threshold in 2019. But the way these fiscal targets are met is by cutting investment rather than retrenching welfare, which is perhaps what should be expected from an SPD finance minister.

There is a nominal cut in investment and a reduced ratio of defence spending, according to Sholz’s fiscal plan announced in early May. But the welfare budget is not cut. Investment spending will decline from an expected €37 billion this year and €37.9 billion in 2019 to €33.5 billion in 2022. While defence spending will be 1.3% of GDP in 2019 and then decline to 1.23% of GDP by 2022.

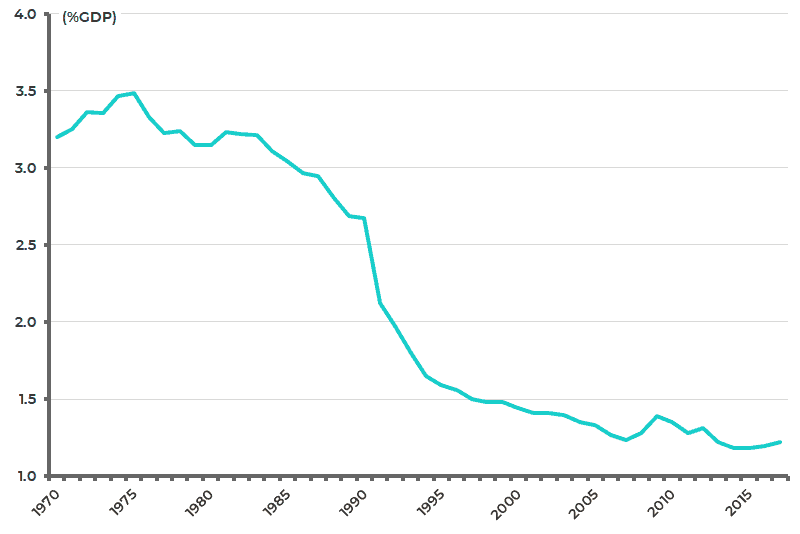

The above is a continuation of a policy trend already in place. Despite Germany’s commitment to the NATO defence spending target of 2% of GDP by 2024, Germany’s military spending as a percentage of GDP has declined from 3.5% in 1975 to 1.2% in 2017 (see following chart).

Germany Military Expenditure as % of GDP

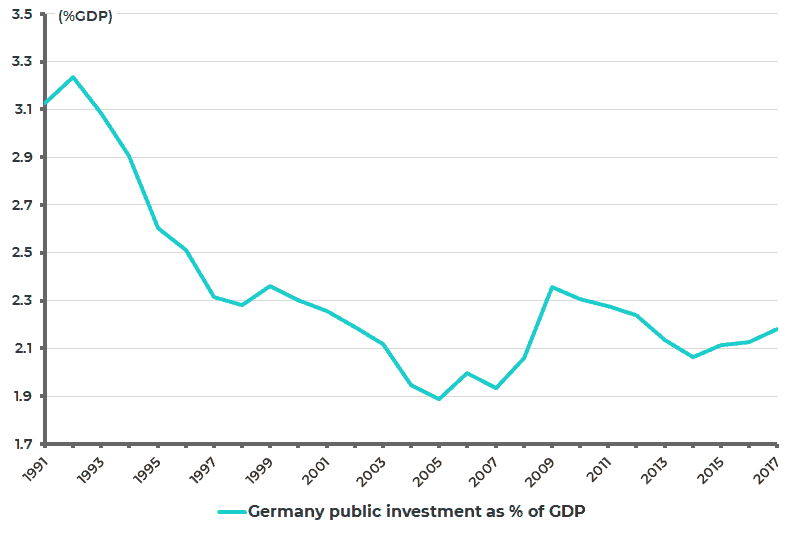

The public investment to GDP ratio has also declined from 3.2% in 1992 to 2.2% in 2017 (see following chart). Meanwhile, the welfare budget keeps soaring, much of which according to the growing number of right-wing populists goes to ‘asylum seekers’ and other immigrants.

Germany Government Gross Fixed Capital Formation as % of GDP

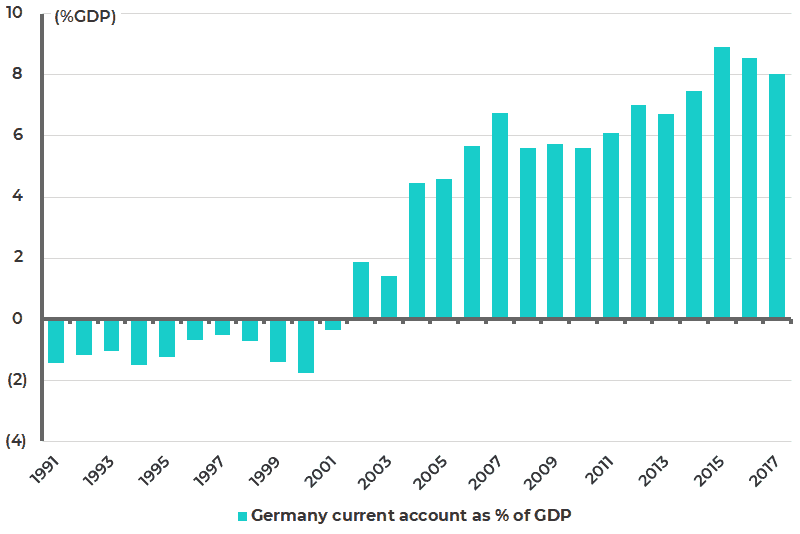

If the German political right focuses on immigration, the critical focus of the neo-Keynesian policymaking establishment globally is the negative consequences on demand globally, and for the Eurozone in particular, of Germany continuing to run a current account surplus of around 8% of GDP (see following chart).

Still, as noted, the latest budget shows no sign of a change in policies. Indeed, there is even talk that Germany will not increase its contribution to the next post-Brexit EU budget for 2021-2027.

Germany Current Account as % of GDP

‘Bailout Union’ — An Unpopular Idea for Germans

All of this raises the question whether Frau Merkel will really be able to support the Macron push for greater fiscal integration in the Eurozone. For there is no doubt that such a move towards what the German people view as a ‘bailout union’ is very unpopular with the German electorate at large.

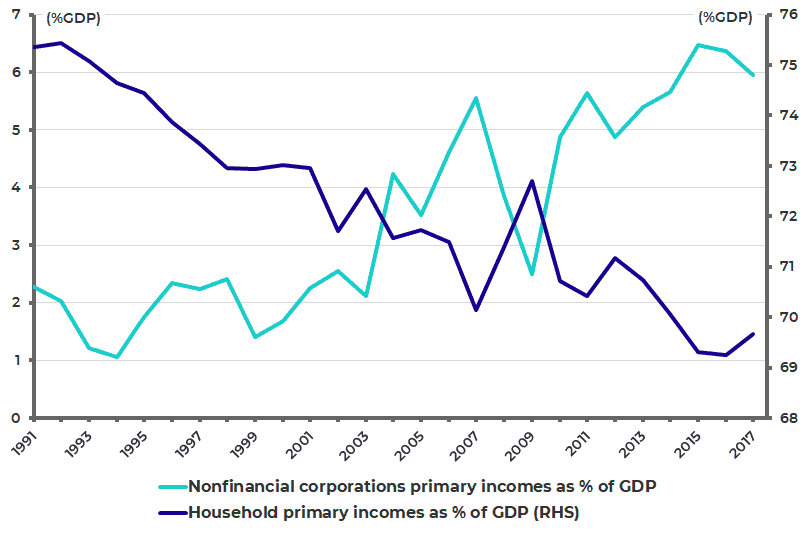

This reflects in large part the fact that the household sector has not been benefiting from the German boom in recent years even as the corporate sector clearly has.

This can be seen in the Japanese-like contrasting trend in corporate and household income trends. Thus, non-financial corporations’ primary income rose from 2.5% of GDP in 2009 to 6.4% in 2016 and 5.9% in 2017, while household primary income as a percentage of GDP has declined from 72.7% in 2009 to 69.7% in 2017 (see following chart).

Germany Household and Corporate Primary Incomes as % of GDP

Merkel Supporting Macron a Risky Move

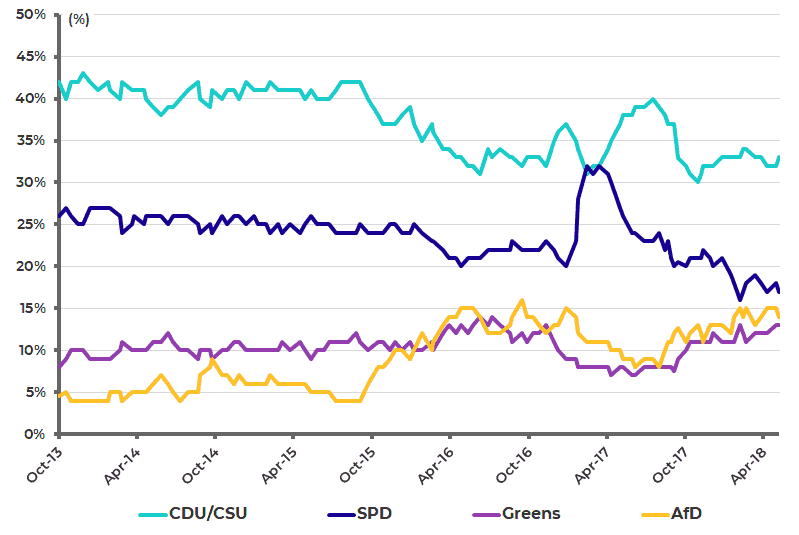

The above means that any move to support Emmanuel Macron overtly is risky for Merkel because it threatens a loss of voter support to the euroskeptical anti-immigration AfD which already has 13% of the seats in the parliament and is polling at a 14% support rate, compared with the CDU’s 33% (see following chart).

But it is even more risky for the SPD, which has lost its traditional blue-collar working-class voters over its unpopular policies regarding immigration and Eurozone fiscal integration. The SPD support rating is now only 17%, having plunged from 32% in March 2017.

German Political Parties’ Support Ratings

All this means that if Merkel does move to support Macron’s agenda more overtly, it will primarily be because the political calculation will be that the German electorate does not have to be consulted on its view for three years given the next federal election is not due to be held until October 2021.

The other reason is that Merkel has been reluctant so far to openly embrace Macron’s agenda due to the sheer unpredictability of events in Italy. But if the formation of a Five Star/League Italian Government raises the threat of an Italian exit from the Eurozone, the threat just might be the catalyst to force Germany to move in Macron’s direction.

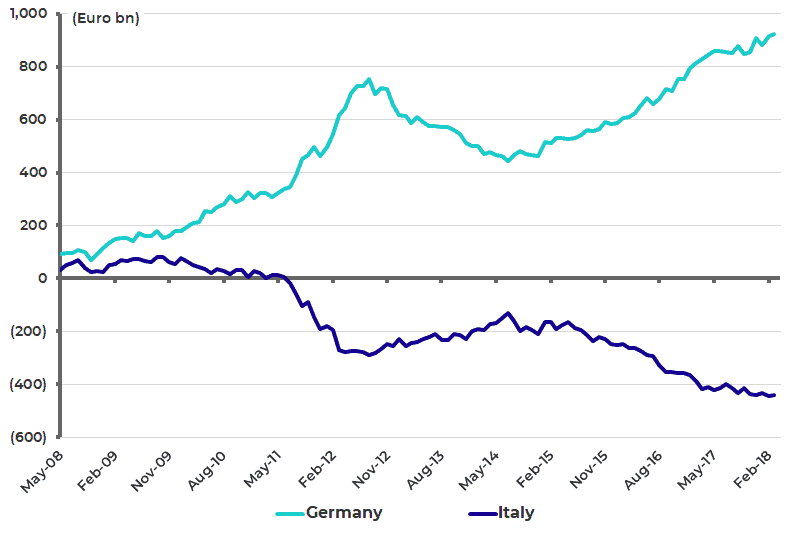

For an Italian exit would cost Germany a lot of money. Thus, Germany’s so-called Target-2 claims, defined as its central bank’s claims on other national Eurozone central banks, rose by 11% YoY to a record €923.5 billion at the end of March, while Italy’s Target-2 liabilities rose by YoY to €442.5 billion (see following chart).

German and Italian Target-2 balance

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.