The inflation debate continues to percolate as the Federal Reserve has finally dropped the word “transitory”.

This writer continues to advise investors to keep a close eye on inflation expectations as the best gauge to the timing of any tightening scare hitting stock markets.

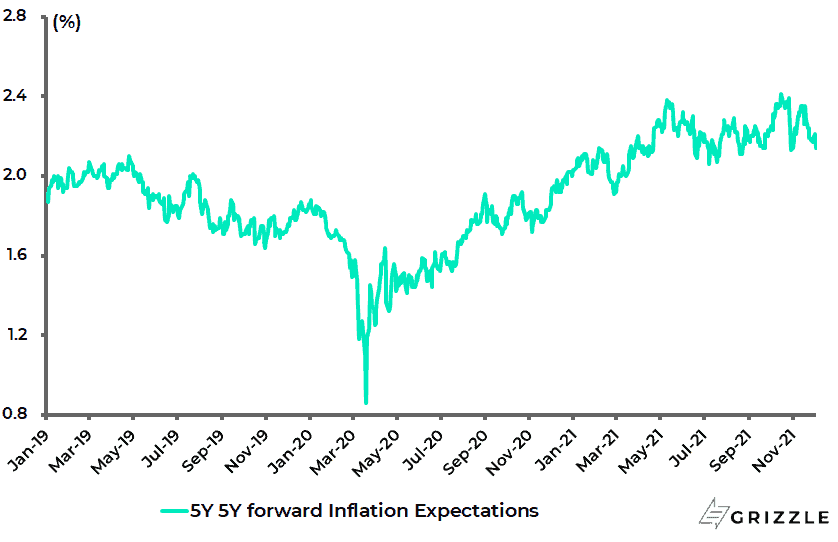

The US five-year five-year forward inflation expectation rate, the key one to watch in terms of what the Fed has signaled, has still not broken above the 2.5% level and indeed has fallen of late on concerns about the new Covid Omicron variant.

It has declined from 2.35% in mid-November to 2.14%.

US five-year five-year forward inflation expectation rate

A break of that level would likely cause markets to focus on the growing risk of real tightening as opposed to just “tapering”.

It should be noted that the abovementioned five-year five-year forward inflation expectation rate measures the expected inflation over the five-year period that begins five years from now.

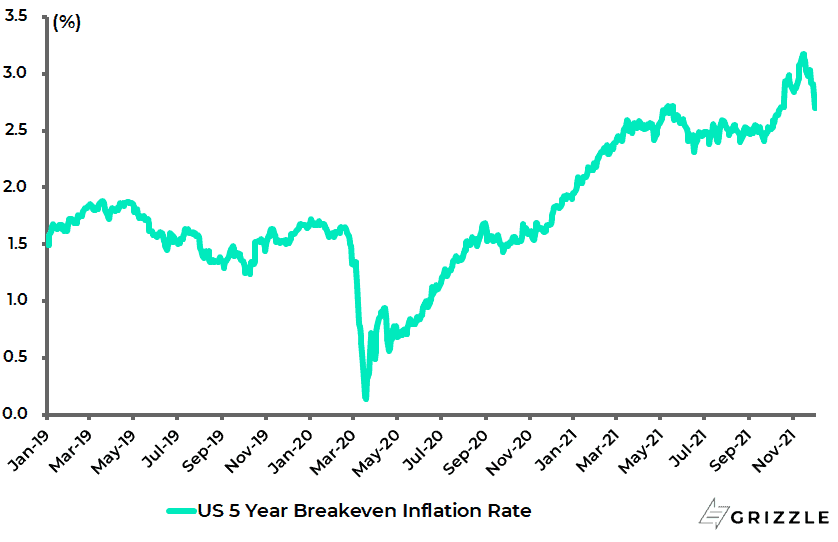

As for the shorter term so called five-year breakeven rate, it measures the expected average inflation for the coming five years.

US five-year breakeven inflation rate

Japan Would Love Some Inflation Right About Now

Meanwhile, Japan should be as big a beneficiary as any stock market globally if inflation really returns.

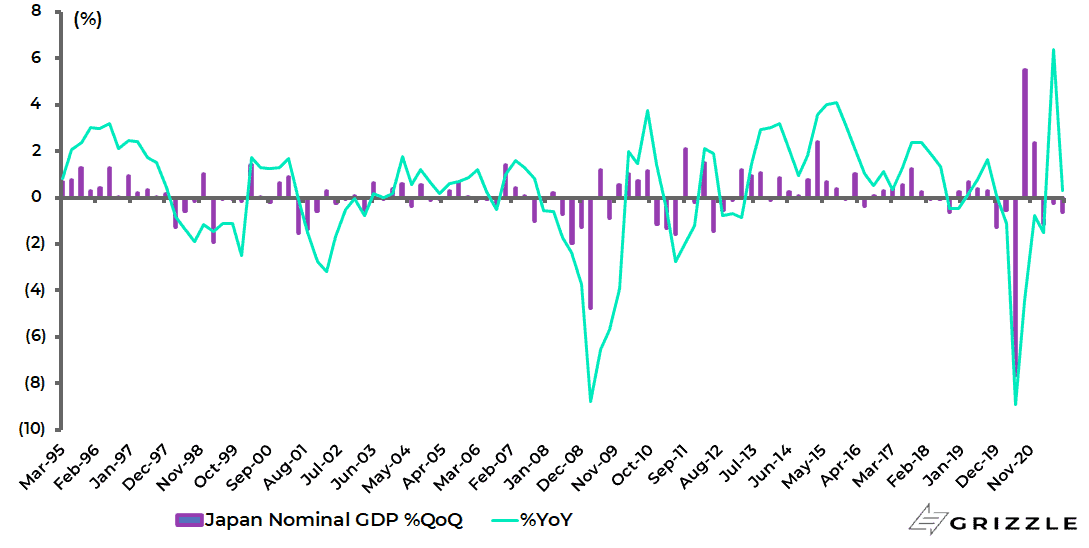

Still, the third-quarter GDP data highlighted the impact of the Delta-driven Covid surge with Japan reporting its third consecutive quarter of a quarter-on-quarter decline in nominal GDP growth.

Japan’s nominal GDP declined by 0.6% QoQ in 3Q21 and is now down 2.0% over the past three quarters.

As a result, Japanese nominal GDP rose by only 0.3% YoY in 3Q01.

Japan nominal GDP growth

Still, the Delta wave has peaked in Japan and restrictions on activity have begun to be relaxed.

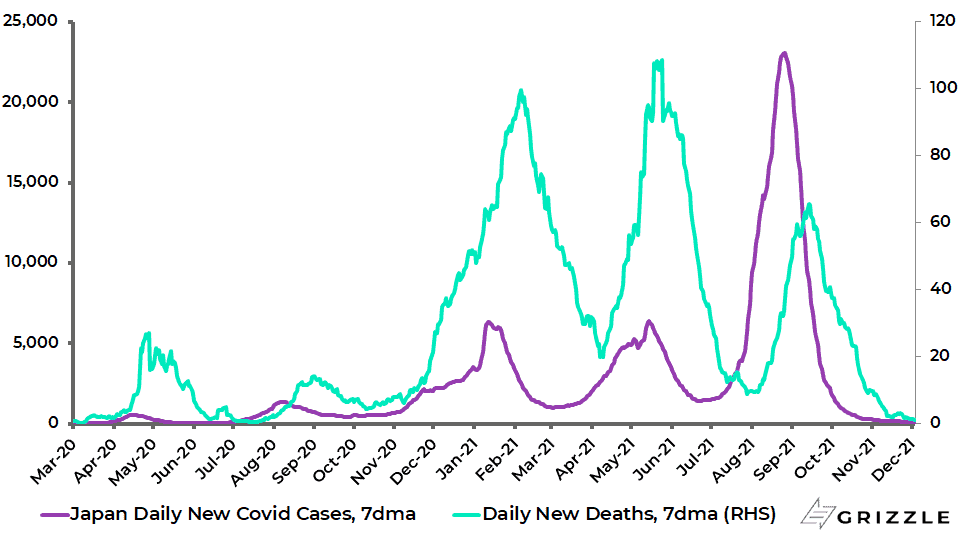

The 7-day average daily new Covid case count has declined from a peak of 23,080 in late August to 115, while the average daily death count is down from a recent high of 66 in mid-September to 1.0.

A total of 77% of the Japan population has now been fully vaccinated.

Japan 7-day average daily Covid cases and deaths

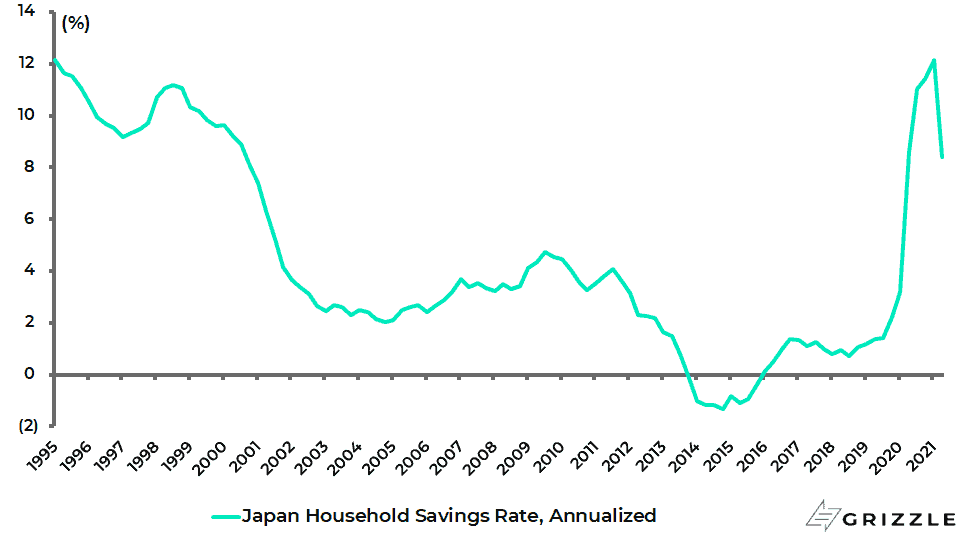

Meanwhile, Japanese household savings have risen not because households have received big handouts, as in the case of, say, America, Britain or Australia, but rather because consumers have reverted to save amidst the prevailing uncertainty.

The annualised household savings ratio increased from 2.2% of disposable income in 2019 to 12.1% in the four quarters to 1Q21 and was 8.4% in the four quarters to 2Q21, according to the latest national accounts data (see following chart).

Japan household savings rate

Source: Japan Cabinet Office

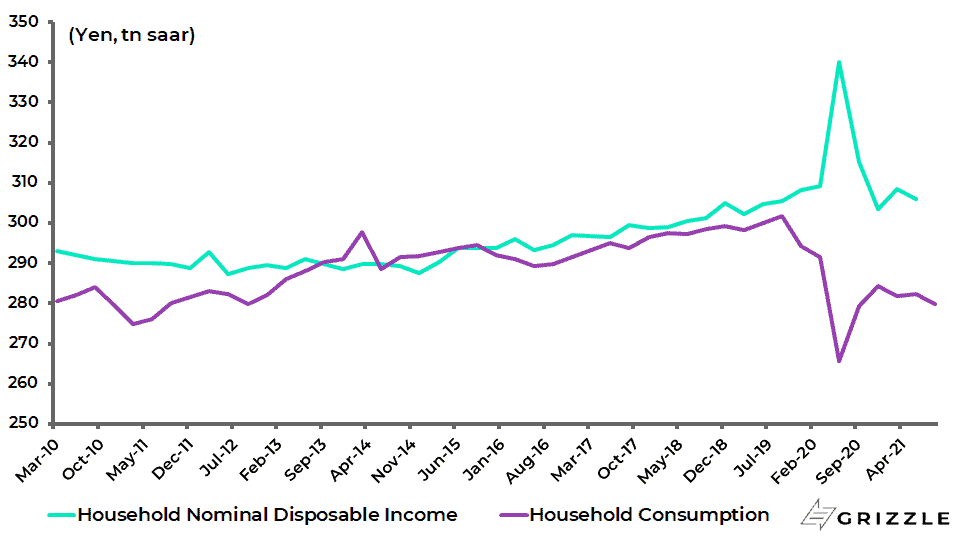

Household consumption is still 7.2% below the pre-Covid high reached in 3Q19.

While household disposable income was an annualised Y306tn in 2Q21, or 1% below the pre-Covid high in 1Q20; though it rose to an annualised Y340tn in 2Q20 and Y315tn in 3Q20 as a result of a Covid-related increases in transfer payments.

Japan household disposable income and consumption

Net current transfers rose to an annualised Y38.6tn in 2Q20 and Y11.7tn in 3Q20, though have since declined to only Y1tn in 2Q21.

Japan household income and savings breakdown

| Yen tn, saar | Pre-Covid 1Q20 | 2Q20 | 3Q20 | 4Q20 | 1Q21 | 2Q21 | 2Q20-2Q21 Average | Diff from 1Q20 |

| Household income excl. transfers | 346.1 | 334.1 | 335.8 | 336.1 | 344.6 | 339.9 | 338.1 | -10.0 |

| Operating surplus and mixed income | 32.0 | 31.1 | 30.9 | 30.4 | 31.5 | 31.5 | 31.1 | -1.2 |

| Compensation of employees | 289.8 | 278.9 | 280.7 | 281.7 | 289.0 | 284.2 | 282.9 | -8.6 |

| Property income, net (interest/dividends, etc.) | 24.3 | 24.1 | 24.1 | 23.9 | 24.1 | 24.2 | 24.1 | -0.2 |

| Less: Current taxes on income, wealth, etc. | 30.3 | 30.1 | 30.0 | 30.4 | 31.2 | 31.5 | 30.7 | 0.4 |

| Less: Net social contributions, payable | 84.3 | 81.9 | 82.0 | 82.8 | 83.9 | 83.4 | 82.8 | -1.9 |

| Social benefits other than social transfers in kind | 79.0 | 79.4 | 79.8 | 79.8 | 80.0 | 80.0 | 79.8 | 1.0 |

| Other current transfers, net | -1.3 | 38.6 | 11.7 | 0.8 | -1.1 | 1.0 | 10.2 | 14.4 |

| Nominal disposable income | 309.2 | 340.1 | 315.2 | 303.4 | 308.5 | 306.0 | 314.6 | 6.9 |

| Adjustment for the change in pension entitlements | 0.0 | 0.1 | 0.1 | 0.1 | 0.1 | 0.2 | 0.1 | 0.2 |

| Consumption of households | 291.5 | 265.7 | 279.4 | 284.4 | 281.8 | 282.2 | 278.7 | -16.0 |

| Household savings | 17.6 | 74.5 | 35.9 | 19.1 | 26.8 | 24.0 | 36.1 | 23.0 |

| Saving ratio (%) | 5.7 | 21.9 | 11.4 | 6.3 | 8.7 | 7.8 | 11.5 | 5.8 |

| Saving ratio (%), annualised | 3.2 | 8.6 | 11.0 | 11.4 | 12.1 | 8.4 |

Source: Japan Cabinet Office

As a consequence, Japanese households’ total income, excluding social benefits and current transfers, in the period between 2Q20-2Q21 has been Y10tn less than the pre-Covid level in 1Q20.

While including social benefits and transfers, nominal disposable income and household savings during that period were Y7tn and Y23tn higher than the pre-Covid levels, with households spending Y16tn less than what they spent prior to the pandemic (see previous table).

By contrast, Americans have received US$2.3tn more in transfer payments since March 2020 compared with the pre-Covid levels, with personal savings increasing by US$2.4tn over the same period.

US personal income and savings breakdown

| US$bn, saar | Feb-20 (Pre-Covid) |

Oct-21 | Mar20-Oct21 (Average) |

Mar20-Oct21 Chg vs Feb-20 |

| Personal income (excl. transfers) | 17,287 | 18,470 | 17,349 | 103 |

| Personal current transfer receipts | 3,208 | 3,943 | 4,590 | 2,303 |

| Disposable personal income | 16,735 | 18,108 | 18,063 | 2,214 |

| Personal outlays | 15,342 | 16,787 | 15,245 | (162) |

| Personal saving | 1,392 | 1,322 | 2,818 | 2,376 |

| Personal saving/disposable income (%) | 8.3 | 7.3 | 15.6 | 7.3 |

Note: Personal income includes compensation of employees, proprietors’ income, rental income, interest and dividend incomes. Source: US Bureau of Economic Analysis

As a result, there is significant potential for Japanese consumers to increase spending should they so wish.

Households’ cash and deposits rose by 4% YoY to a record Y1,072tn at the end of 2Q21.

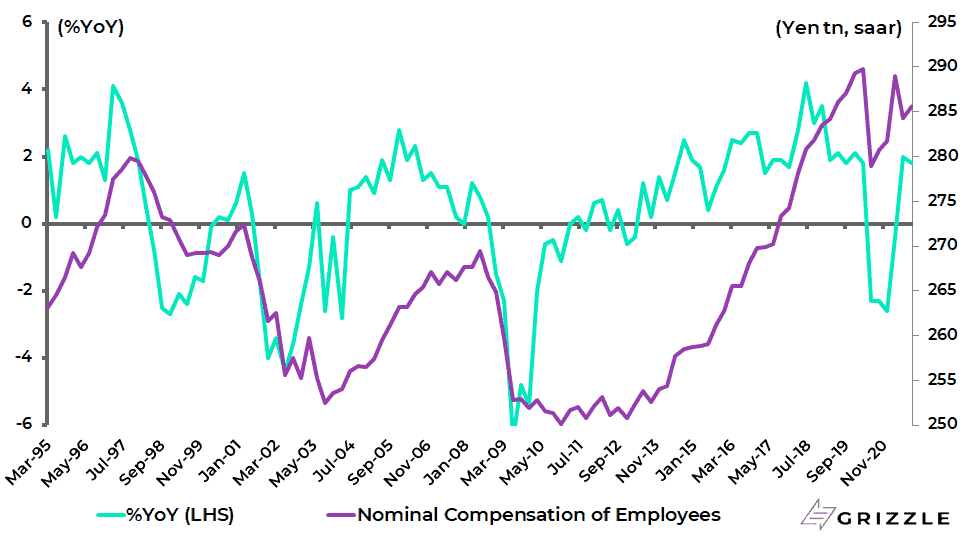

It is also the case that total compensation for employees grew by 1.8% YoY in 3Q21 and is up 13.9% since 2013.

Japan compensation of employees

Source: Japan Cabinet Office

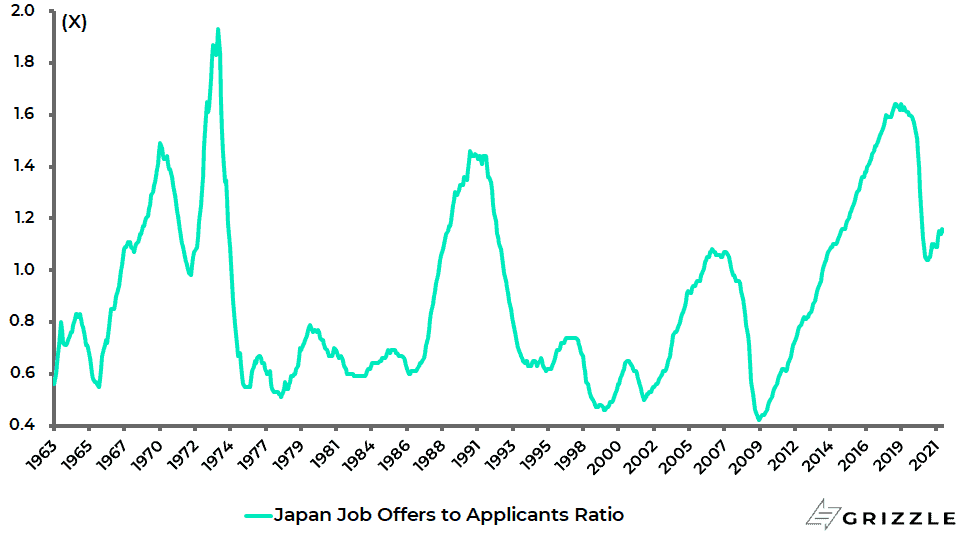

Japanese Labor Market is Definitely Tight

The labour market also remains comparatively tight.

The job offers to applicants ratio has risen from 1.04 in October 2020 to 1.15 in October 2021, though it remains well below the recent high of 1.64 reached in January 2019.

This compares with the long-term average of 0.90 since 1963.

Japan job offers to applicants ratio

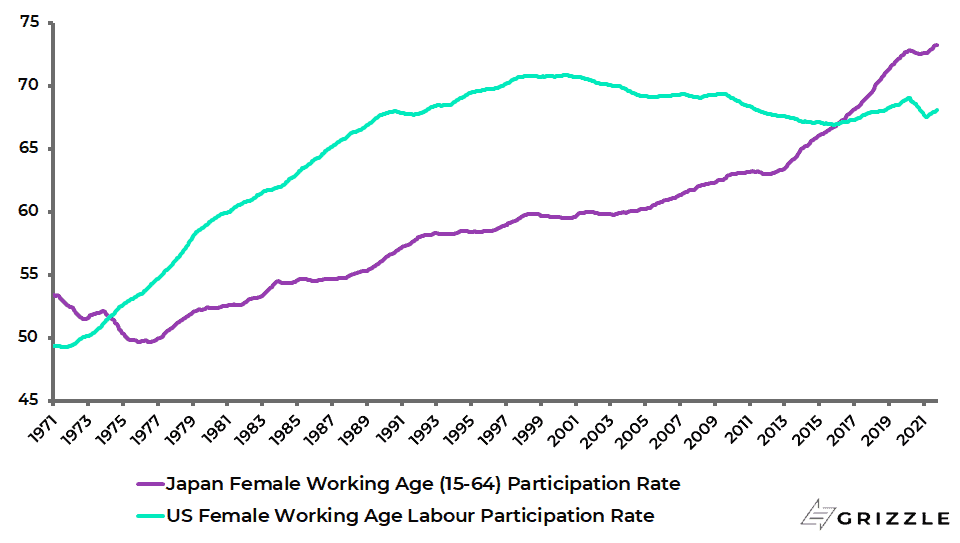

The tight labour market is also reflected in Japan’s record high female working-age participation rate.

The annualised female working-age (15-64) labour participation rate has risen from 72.5% in the 12 months to October 2020 to a new high of 73.2% in the 12 months to October.

Interestingly, it has been higher than the prevailing American level since 2016.

Japan and US female working-age labour participation rates

Japan Back to Releasing Godzilla Sized Stimulus Packages

Meanwhile, the new Japanese Government of Fumio Kishida, who replaced Yoshihide Suga as prime minister on 4 October, has reverted to type by unveiling recently yet another monster fiscal stimulus package.

This, approved by the cabinet on 19 November, includes Y55.7tn in fiscal spending, reaching a new record level exceeding the Covid-triggered Y48.4tn emergency stimulus announced in April 2020 at the start of the pandemic.

The stimulus package will also be much bigger than the Y15.4tn stimulus package in April 2009 following the global financial crisis.

The main distinguishing feature of this latest package is the reported decision to provide Y100,000 in cash and vouchers only to those under 18 years old, with the payments expected to be made by spring 2022.

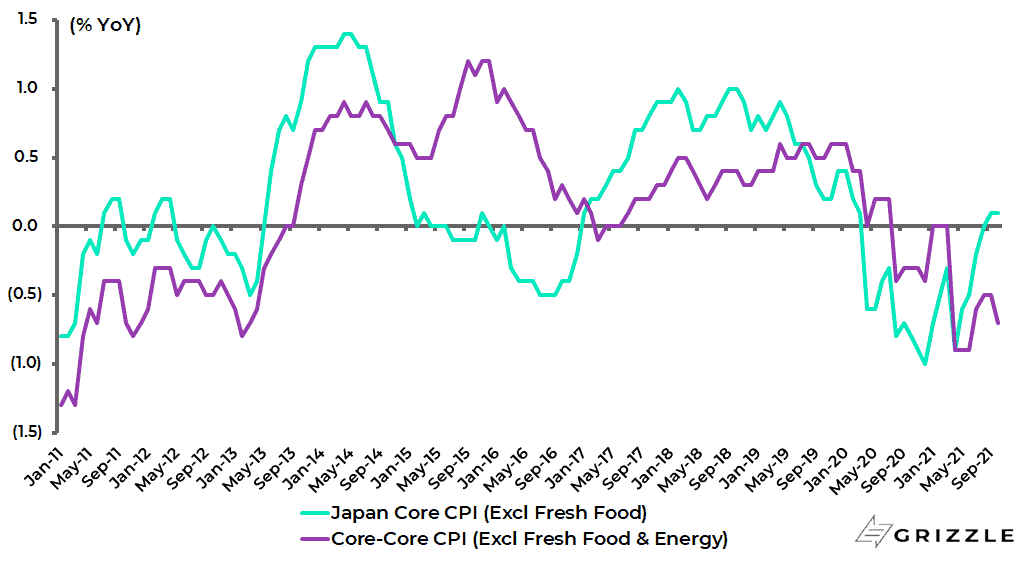

If Kishida’s premiership offers little prospect of an innovative approach, in stark contrast to the expectations created by the launch of so-called Abenomics back in late 2012, it is worth highlighting that the Covid triggered downturn has not led to a self-feeding collapse in prices as with previously post Bubble downturns in Japan.

Japan core CPI, excluding fresh food, rose by 0.1% YoY in October while CPI excluding fresh food and energy was down 0.7% YoY.

Japan core CPI inflation

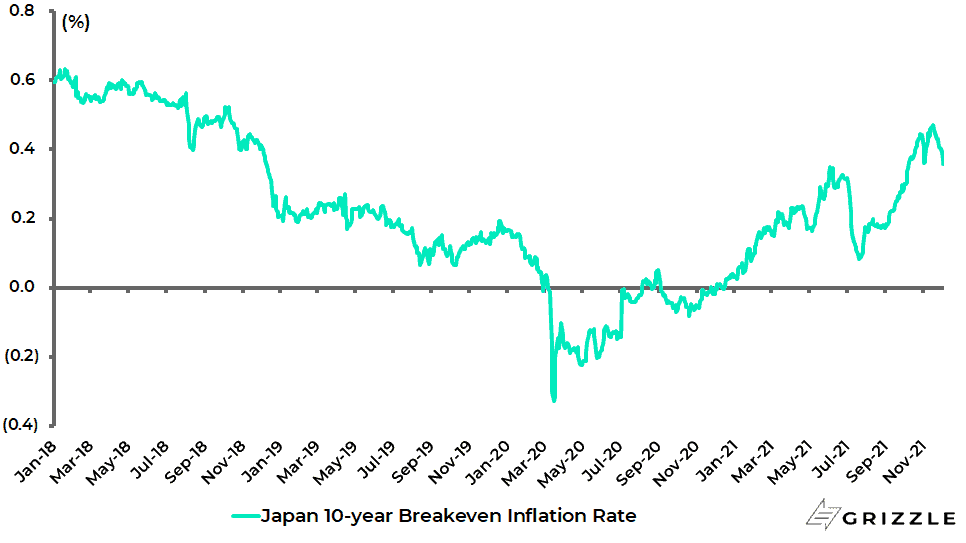

It is also the case that inflation expectations never fell into deflation and have actually moved up in recent months.

The Japan 10-year breakeven inflation rate has risen from a recent low of 0.07% in July to 0.49% in mid-November, the highest level since October 2018, and is now 0.36%.

Japan 10-year breakeven inflation rate

The Return of Inflation Would be Very Good for Japanese Stocks

The growing evidence of the waning deflationary pressures should at some point prompt Japanese domestic institutions to allocate out of Japanese government bonds into Japanese equities.

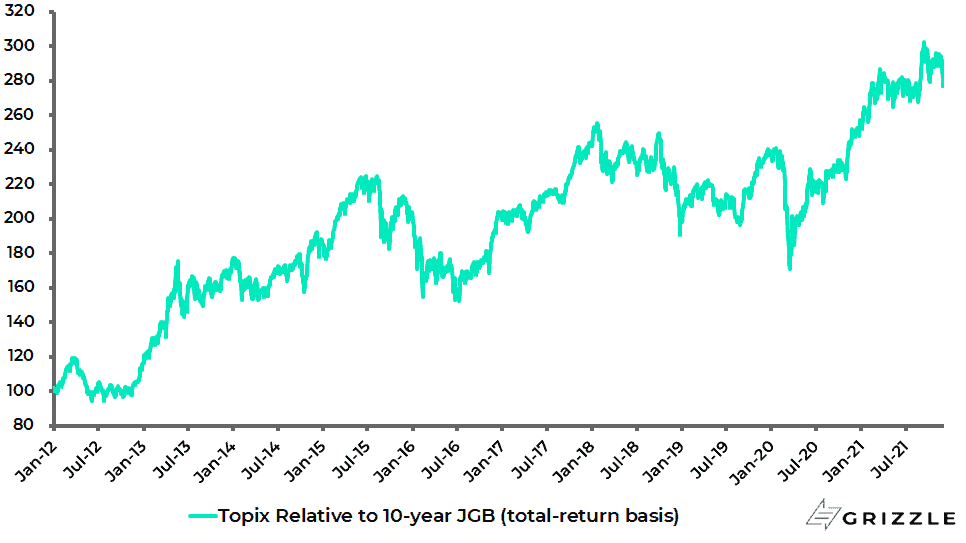

On this point, the Topix has now outperformed the 10-year JGB on a total return basis by 188% since mid-November 2012 shortly before the launch of Abenomics in December 2012.

But despite this dramatic outperformance domestic institutions remain missing in action because of a mistaken, albeit entrenched, obsession with volatility-adjusted returns.

Topix relative to 10-year JGB (total-return basis)

It is clearly going to take conviction that inflation has returned, or rather that deflation has ended, to trigger a change in mass psychology.

In this respect, the Japanese stock market has, as already noted, the potential to be one of the biggest long-term beneficiaries if the transitory view of inflation proves to be wrong.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.