Federal Reserve chairman Jerome Powell reminded everybody, if it was needed, that he is no Paul Volcker with his comments at the December FOMC meeting when he said that a rate cut “begins to come into view” and is “clearly a topic of discussion out in the world and also a discussion for us at our meeting today.”

As a result, stock markets celebrated the presumed pivot in the run up to year end.

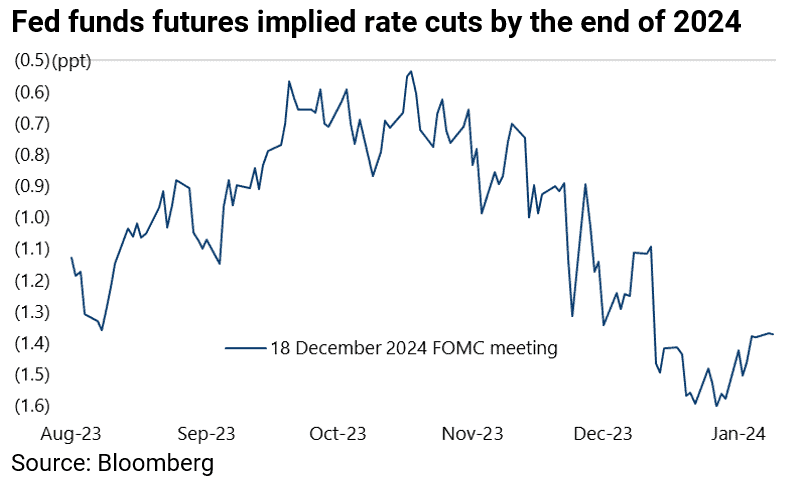

Money markets’ easing expectations rose from 75bp of rate cuts in 2024 in mid-November to 160bp in late December, though they have fallen back to 137bp following Friday’s employment data.

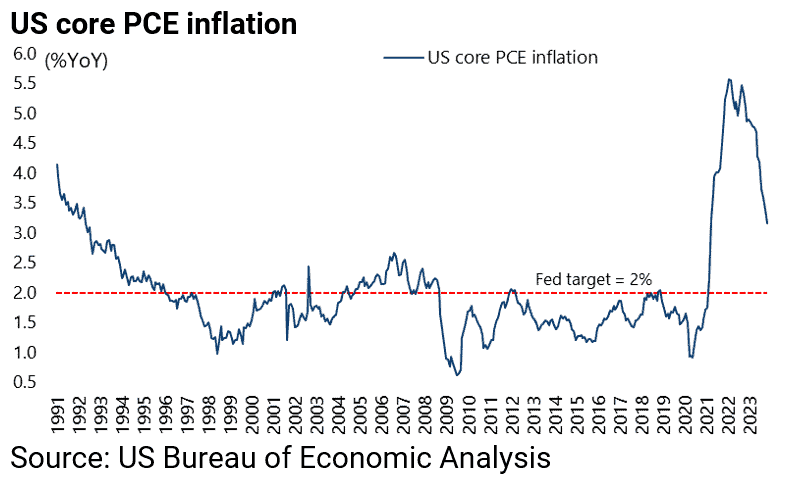

Meanwhile core PCE inflation, the Fed’s favourite inflation indicator, came in at 3.2% YoY in November, down from 3.4% YoY in October and 4.7% YoY in May 2023.

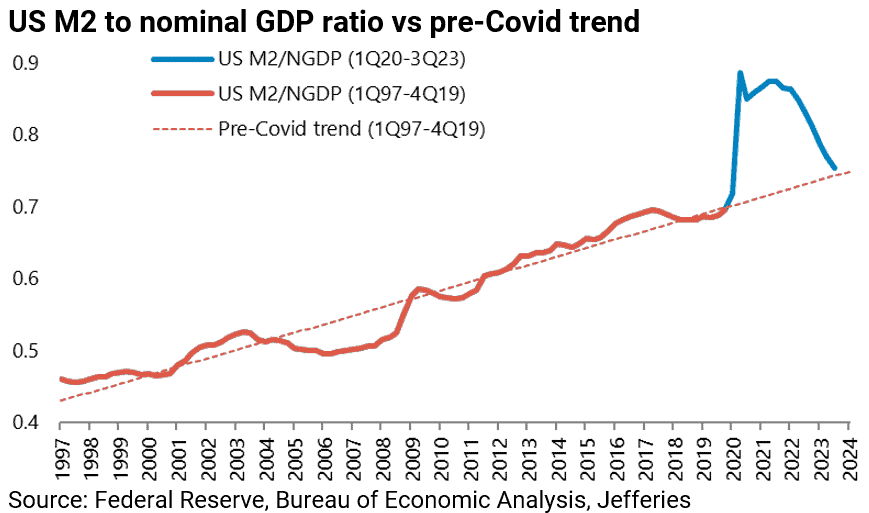

If this is the near-term backdrop with markets now pricing in a presumed soft landing in the US, the release of the revised third quarter US GDP data has also provided an opportunity to update the US M2 to nominal GDP ratio which this writer has been tracking.

The ratio is now back almost at the pre-pandemic trend.

The chart highlights the delayed impact of monetary tightening as a result of the base effect from the surge in M2 growth in the second quarter of 2020.

The ratio rose from 0.719 in 1Q20 to a peak of 0.887 in 2Q20 and has since declined to 0.754 in 3Q23. It is now only 1.5% above the pre-pandemic trend since the ratio bottomed in 1997, down from 3.8% in 2Q23 and a peak of 25.9% in 2Q20.

It is understandable that markets rallied into year-end on the Fed’s more doveish stance and resulting much greater confidence that the next move in the federal funds rate will be down.

But it is still the case that it is the delayed but ongoing impact of monetary tightening which represents the greatest threat to risk assets, with the greatest risks facing the formerly booming world of private equity and the still booming world of private credit since they were the biggest beneficiaries of the zero-rate era.

A Weak Yen Remains Bullish for Japanese Stocks

If a more dovish Fed is seen as a positive signal for stocks, so long as the perception is that a recession can be avoided, it should also mean a weaker US dollar.

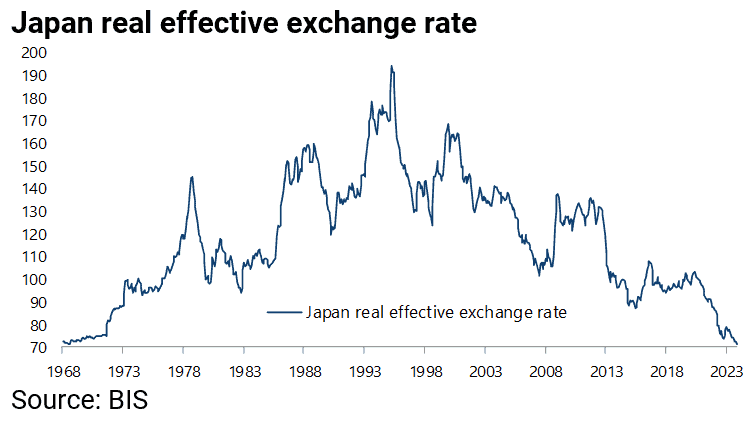

That in turn raises the issue of the Japanese yen which remains extremely cheap on a real effective exchange rate basis.

The yen’s real effective exchange rate has declined by 63% since peaking in 1995 to 71.62 in November, the lowest level since 1968.

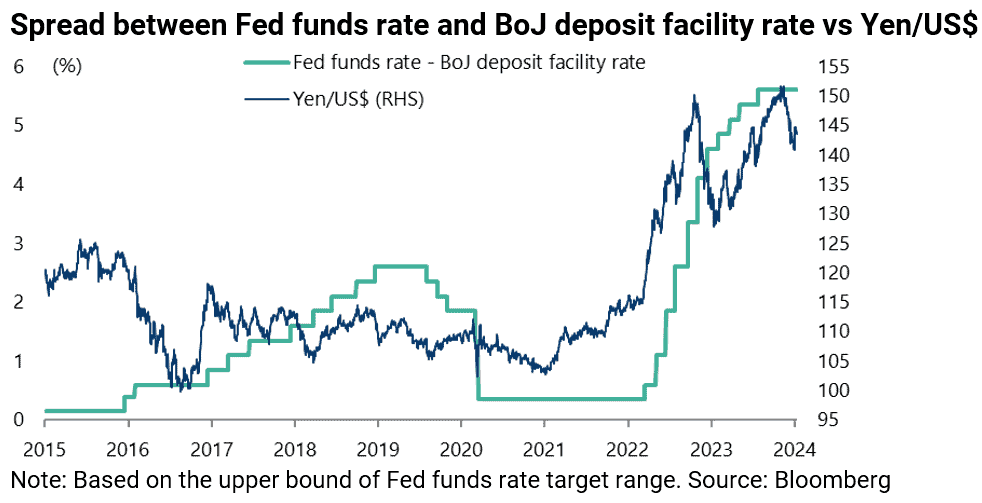

Still the yen has rallied by 5.8% against the US dollar from the low of Y151.9/US$ reached last year in mid-November.

This partly reflects growing confidence that the differential between the US and Japan have peaked in terms of short-term interest rates.

The spread between the Fed funds rate (upper bound) and the BoJ deposit facility rate has risen from 35bp in March 2022 to 560bp.

Japan Rates Expected to Normalize, Driving a Stronger Yen

Still BoJ Governor Kazuo Ueda also encouraged expectations that the central bank will finally end negative rates, and therefore finally normalise monetary policy, in comments made in a TV interview in Tokyo when the Anglo-Saxon world was celebrating Christmas.

Ueda said on 26 December in his first television interview with NHK since taking the job in April that ending negative rates could come sooner than originally anticipated.

This followed the release on 27 December of the “Summary of Opinions” of the Bank of Japan monetary policy meeting on 18-19 December which indicated a growing debate as regards the timing of a further tightening of monetary policy with one hawk arguing that the risk of an excessive rise in inflation was “not zero”.

Meanwhile the weak yen has meant a further loss of purchasing power for long-suffering Japanese households squeezed by rising prices.

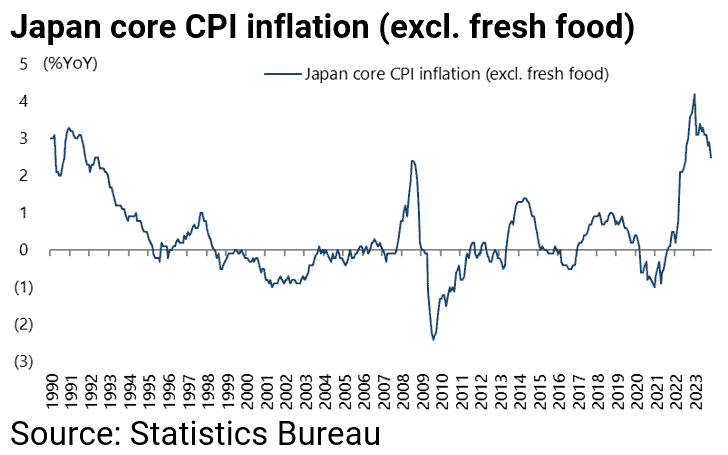

Japan core CPI inflation, which excludes fresh food, rose by 2.5% YoY in November though down from 2.9% YoY in October.

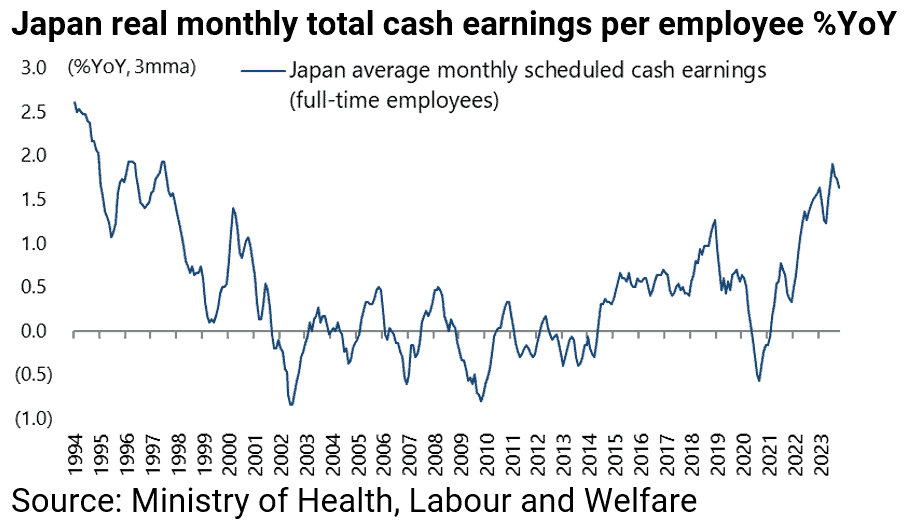

This is why, if nominal wages are rising more rapidly than at any time since 1997, the trend in real wages is showing a very different story.

Japan average monthly scheduled cash earnings for full-time employees rose by 1.9% YoY in the three months to July, the highest growth rate since 1997, and were up 1.6% YoY in the three months to October.

By contrast, real total cash earnings per employee declined by 2.7% YoY in the three months to October.

Future Wage Negotiations a Big Deal for Future Japanese Inflation

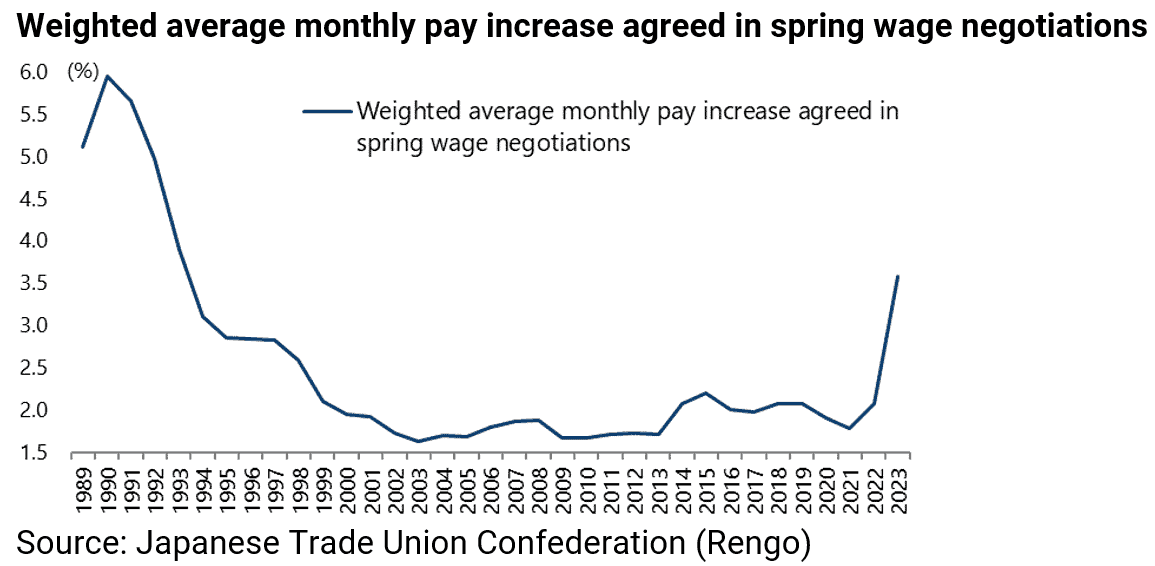

This is why markets will be watching closely the outcome of the forthcoming shunto spring wage negotiations in Japan.

As for the result of the negotiations last year, the Japanese Trade Union Confederation (Rengo) reported in July that companies concluded their annual wage talks with average wage hikes of 3.58%, the largest increase since 1993, including a 2.12% increase in base pay.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.