Who is Palantir?

To put it simply, Palantir is one of the oldest private big data software companies.

Palantir sells software to businesses and government agencies to help them manage their data and make better connections.

For example, Palantir can find connections from thousands of unstructured data points (credit card purchases, phone calls, web browsing) to identify a potential terrorist for government agencies.

The company was built on goverment contracts and only recently has begun making a big push to diversify into corporate contracts.

Palantir’s product is most definitely valuable and in demand, but there are three major risks we see to continued growth and profitability that are keeping us on the sidelines for now.

Three Major Risks to Growth

#1: Reliance on Big Government Clients

Palantir is trying to diversify away from a dependence on government contracts but so far has not been successful.

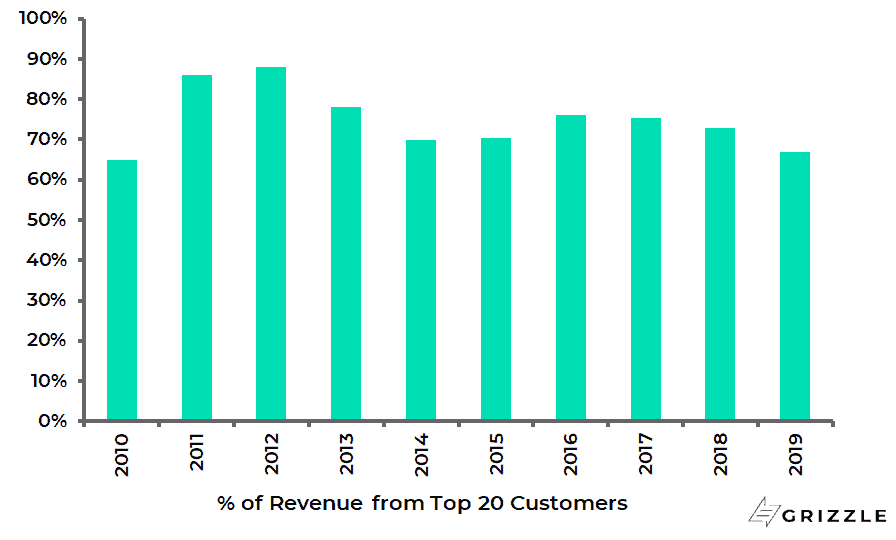

Looking at the % of revenue coming from the largest 20 clients (read governments) we don’t see a meaningful decrease in the weighting over the last few years.

A high concentration of customers means a loss of one can have a big impact on revenue growth and the stock price.

Investors don’t like surprises and Palantir’s customer concentration is currently an unwelcome feature of the company.

% of Revenue Coming from Largest 25 Customers

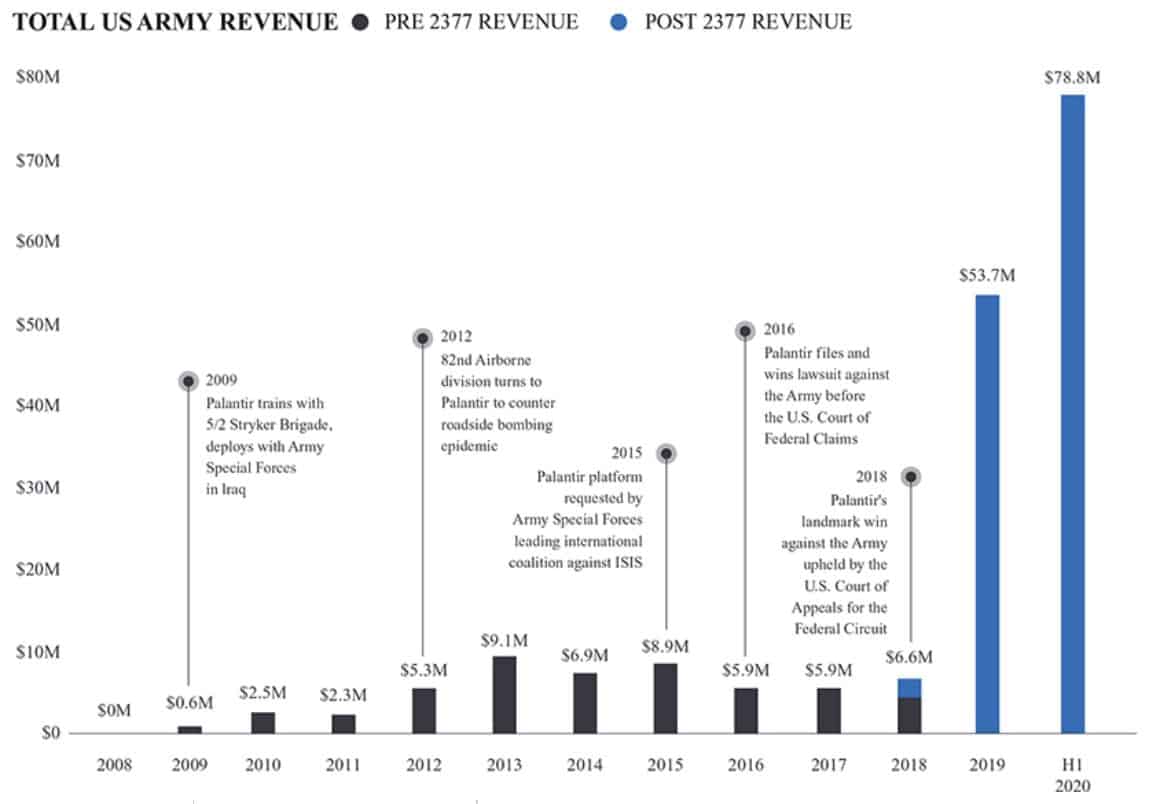

A contract with the U.S. Army made up a big part of that jump in government revenue.

The U.S Army alone went from 1% of revenue in 2018 to 16% today and was 30% of all revenue growth in 2019.

Big Jump in Government Revenue in 2020

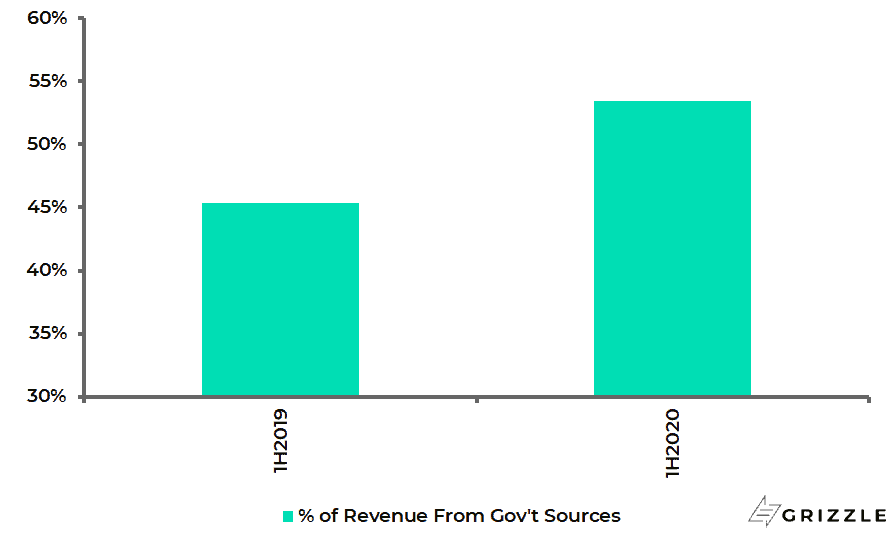

To drive our point home, government revenue increased from 45% of sales in 1H2019 to 53% in 1H2020.

COVID Has Actually Increased Gov’t Concentration

Corporate diversification is only in the early stages which could keep growth from showing the slow and steady results investors expect from SaaS companies.

#2: The Recent Improvement in Margins Likely Won’t Last

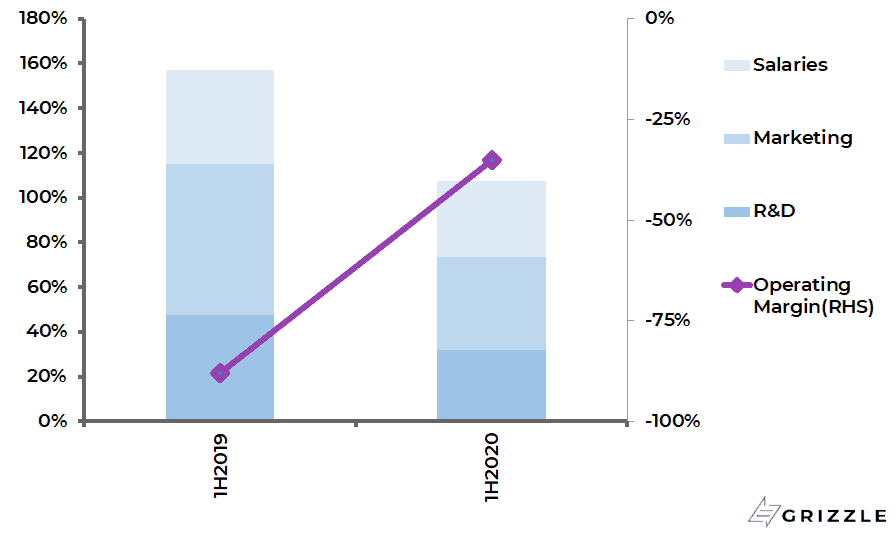

Palantir has seen a big increase in profit margins in the last six months compared to last year.

Investors new to the story may be tempted to pay a higher price for the stock to give the company credit for a new, higher-margin profile.

We think this would be a costly mistake.

If you dig a bit deeper you will see the margin increase was due to unsustainable cuts to operating expenses, not a change in the long-term profit potential.

The chart below shows that marketing spend as a % of revenue fell 25%, R&D spend fell 16% and salary expense fell 8%.

Palantir specifically called out the Coronavirus in their S-1 for keeping employees at home which has saved them lots of money on travel and marketing expenses.

In our opinion, these cost savings will largely reverse once the pandemic is over and sales and marketing ramps back up.

We are already seeing this with Marketing, R&D and G&A as a % of revenue up in the June quarter reversing some of the big fall in the quarter ending March.

The chart below shows that the improvement in the operating losses was almost exclusively due to lower spending on R&D and marketing, not a change in the underlying profitability of the business.

Cuts in Marketing and Personel Spending Drove Margin Gains in 1H2020

If costs rebound as the Coronavirus recedes it will slow or even reverse the recent profit improvements, denting the multiple investors are willing to pay and the stock price.

#3: To Grow You Need Clients, But Client Attrition is Concerning

Palantir’s average customer has been with the company for over six years, which is impressive and is typical among large government clients.

But to win these huge accounts, the company spends a lot more time selling the product before the customer will bite, six to nine months on average.

Also, the initial revenue from the contracts are tiny as Palantir proves the value of its software to customers who over time ramp up their usage and spending.

The initial losses are all fine if Palantir can hang onto clients for a long enough time, but recent data points to some lost customers as the Pandemic raged.

According to back of the envelope calculations below, Palantir went from 133 customers in 2019 to 125 today.

Palantir is not immune from the Coronavirus.

Based on my math they've lost around 8 customers in H1 2020 (comparing end of period 2020 customers with 2019 average) pic.twitter.com/RgXbz74y7Y

— Bread Crumbs Research (@breadcrumbsre) September 19, 2020

An article on Palantir’s push into Europe makes a concerning claim that of the 48 entities to have tried the service, 27 had already quit with the status of 8 others unknown.

Potentially losing 70% of your clients even if it is over a number of years doesn’t give us confidence in Palantir’s ability to hold onto clients long enough to generate solid profits from them.

Palantir’s business model gives up profits in the short term for cashflow on the backend, but it only works if customers don’t leave.

Palantir Chose a Direct Listing Instead of an IPO: What’s the Difference?

Palantir management chose a different route to take the shares public than the traditional initial public offering (IPO) process.

The decision to pursue a direct listing over an IPO could have potentially huge implications for the future price of the stock.

The biggest practical difference between an IPO and a direct listing is that Palantir will not set an official price for the shares before trading begins.

In an IPO process, the management team travels all over the world meeting investors, explaining the story and drumming up buying interest.

Based on these meetings and conversations between the banks on the deal and their own clients, a price is decided on that balances supply, demand and the desire to see the stock price perform well, ie. go up, on the first day of trading.

A direct listing avoids all of this price discovery in favor of letting investor’s sort out the price for themselves through actual trades on the first day.

Now don’t think this means investors can just name any price they want for the stock until the equilibrium price is found.

Day 1 trades are still anchored to where the stock has been trading recently on the private markets.

Investors set their opening bids based on the private price of the stock, so these prior sales do have a big impact on early trading prices in a direct listing.

The market maker, the one who makes sure shares are trading hands in an orderly fashion, also sets a “reference price” on the first day based on buy and sell prices they are seeing.

This reference price also guides investors in what prices they offer on day 1.

Now the big difference between an IPO and a direct listing comes after the first public trade is done.

In a direct listing, all shareholders are free to sell their stock whenever they want at the prevailing market price.

This differs in a big way from an IPO where a majority of shares are restricted from trading for 180 days.

Direct listings can lead to more selling pressure than a typical IPO which means the stock price falls more in the month or two after going public than it would under an IPO process.

However, the market finds the stock price that balances supply and demand quicker than in an IPO where the share restrictions keep supply artificially low.

Looking at past direct listings will give us a flavor for how the Palantir stock price could perform in the days and months after it goes public.

How Have Other Direct Listings Performed?

There are two large direct listings we can use for reference here, Spotify and Slack.

Spotify went public in April 2018 while Slack’s direct listing was in April 2019.

Both companies did not put any restrictions on stock sales by employees and insiders, which is a big difference from the 180-day lockup Palantir is imposing on 80% of shares outstanding.

So how did buyers of the stocks on day 1 make out?

For Slack, the company gave investors a “reference price” before the direct listing of $26.

The stock opened at $42/sh, a 62% pop on day 1.

Spotify listed a reference price of $132/sh and also opened higher, up 25% to $165/sh.

So insiders were certainly happy but what happened to investor’s who bought at those prices?

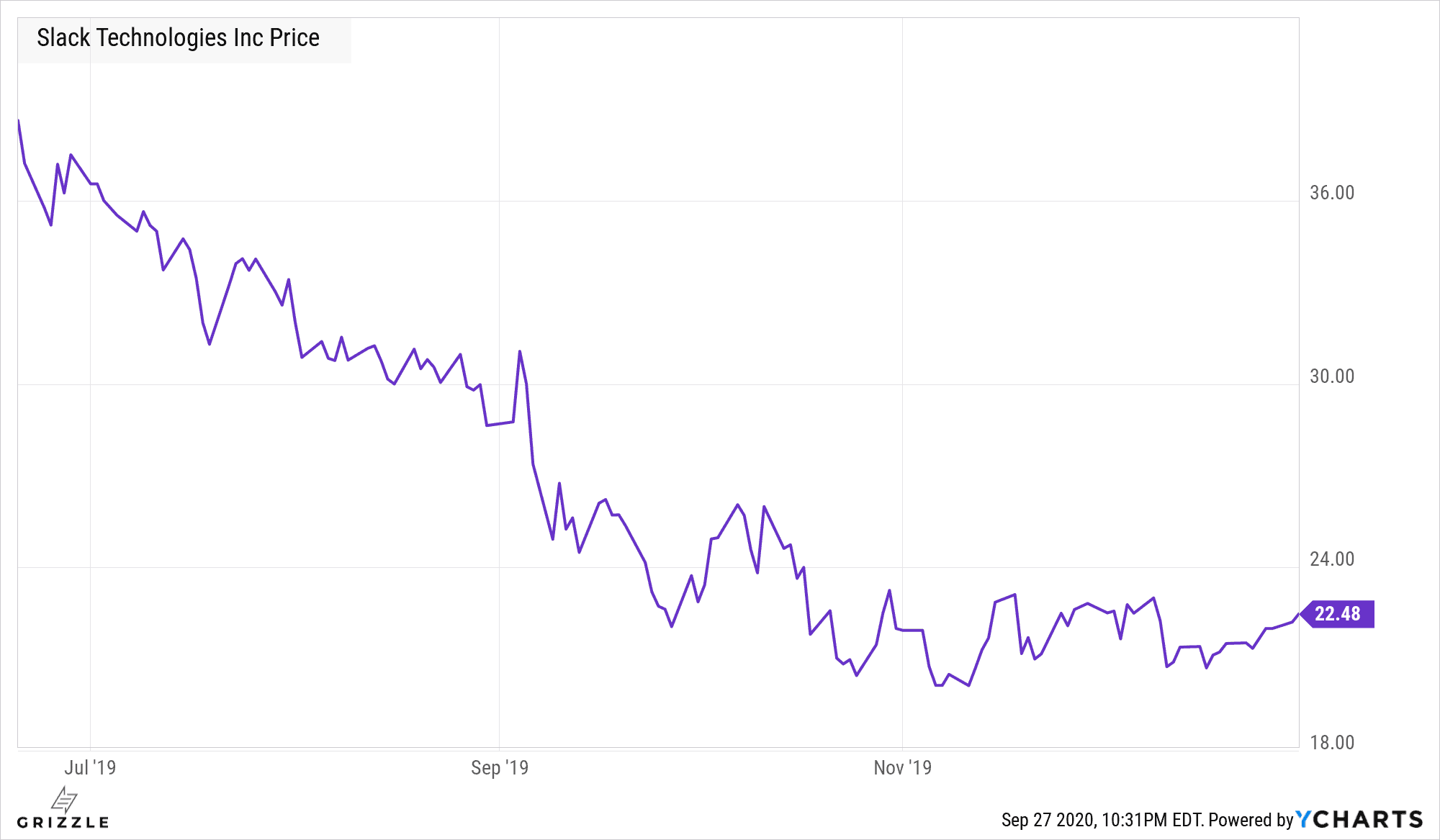

In Slack’s case, the stock closed day 1 at $38.62/sh before eventually falling to $25 3 months later and bottoming at $22 in October, handing early investors a 40% loss.

Slack’s first 9 Months Public

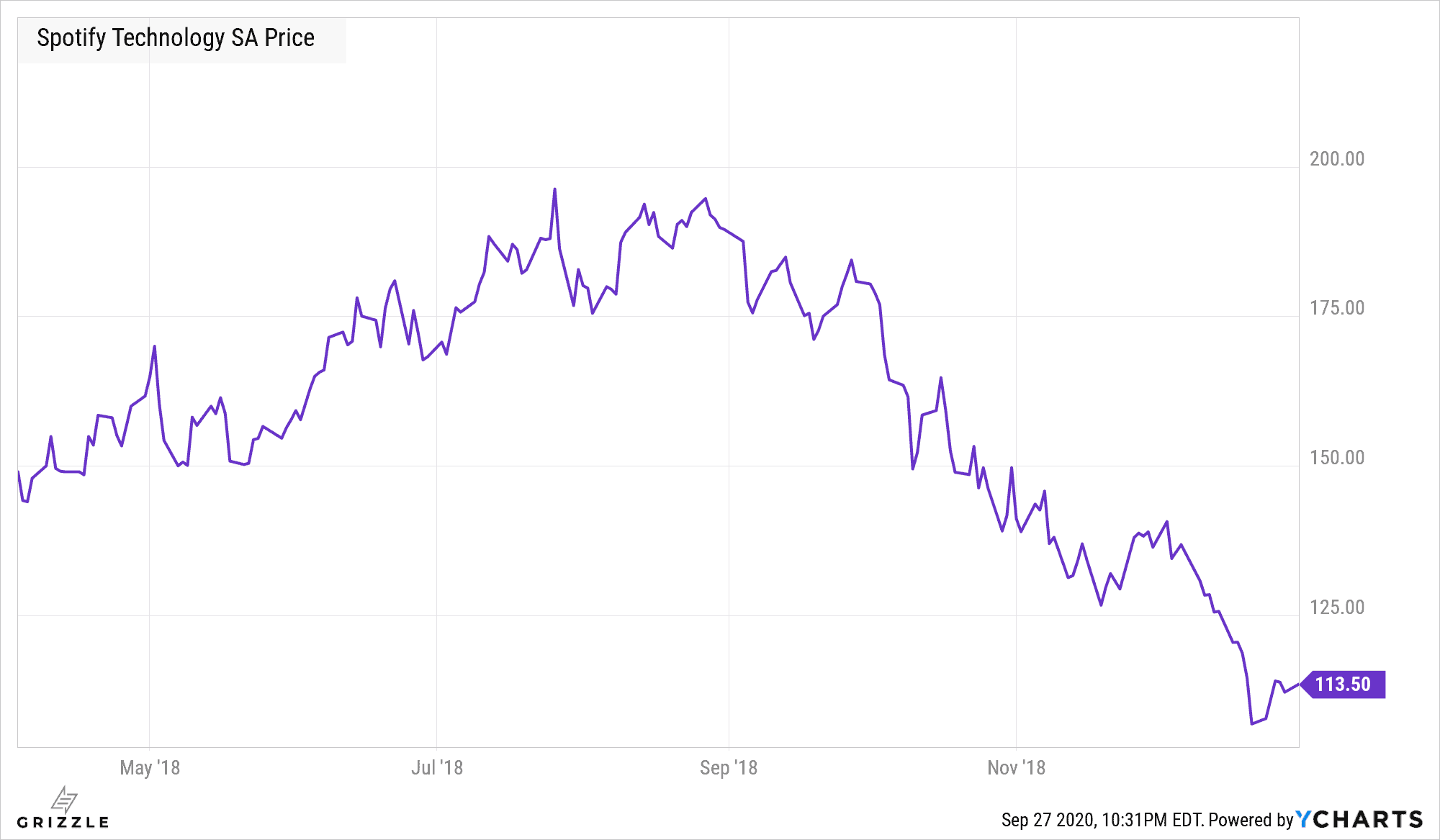

Spotify closed the first day at $149.01/sh and was at $169/sh 3 months later, however, the stock bottomed at $109/sh in December handing investors early losses just like Slack.

Spotify’s first 9 Months Public

How Does Growth and Profitability Stack Up?

High growth software companies are valued by the market for their growth above all.

The faster you can grow the more the market likes you and the higher multiple of revenue they are willing to pay.

Cashflow, profits, free cashflow, whatever your name for profitability, they all come in a distant second.

The most important steps you can take to figure out where Palantir should trade on day 1 and 10 years from now is to figure out how revenue growth stacks up against other software competitors.

Best growth = best multiple, its really that simple.

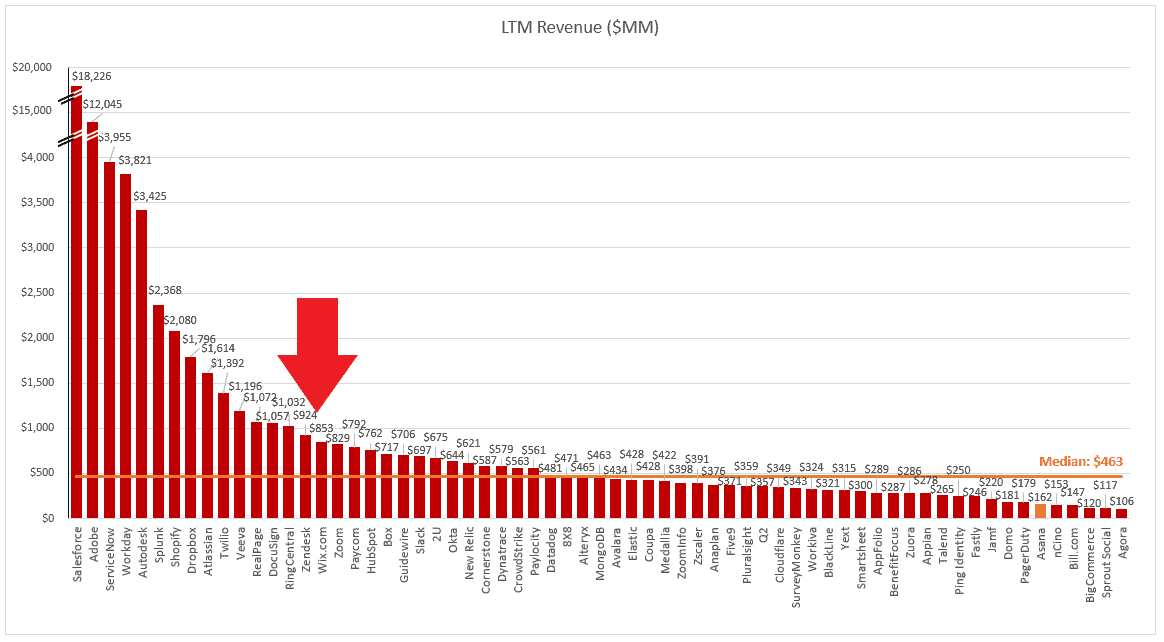

First, looking at the absolute size of Palantir, the company is on the larger side for a cloud software business.

The company has been in business for almost 20 years which explains its larger size.

Palantir Revenue vs Peers

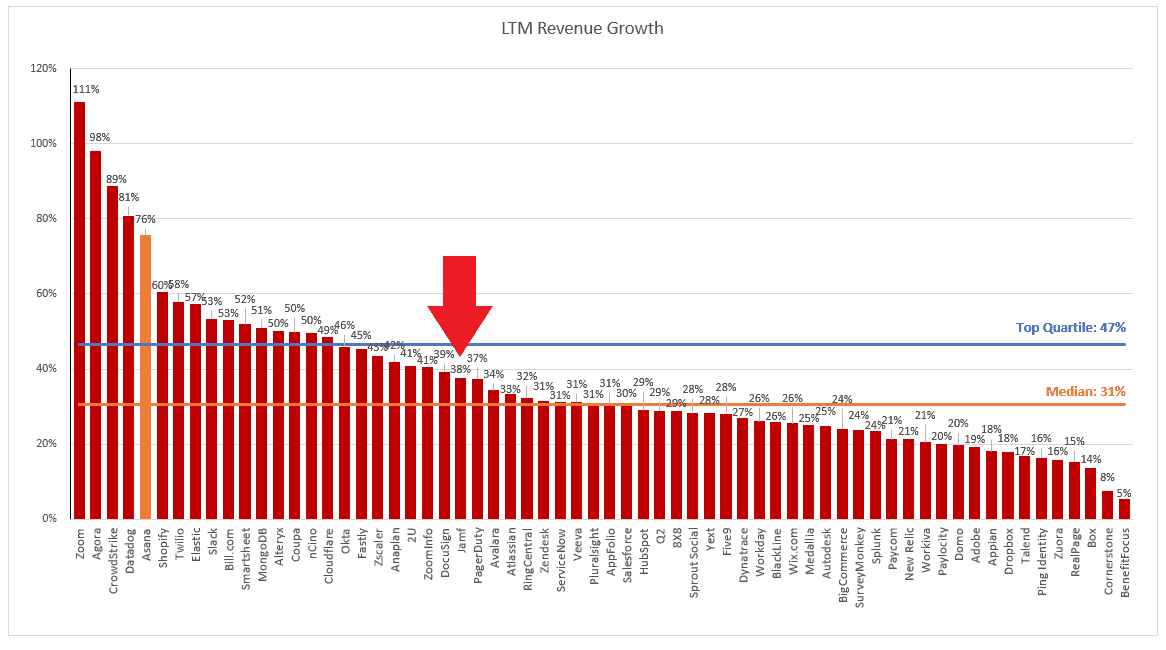

Growth is more important than the absolute level of revenue however and here Palantir puts up a decent showing based on the last 12 months of revenue growth.

Growth is above average but out of the top quartile and forecast to slow to 35% in the next 12 months, from 38% in the last 12.

Palantir LTM Revenue Growth Better than Average

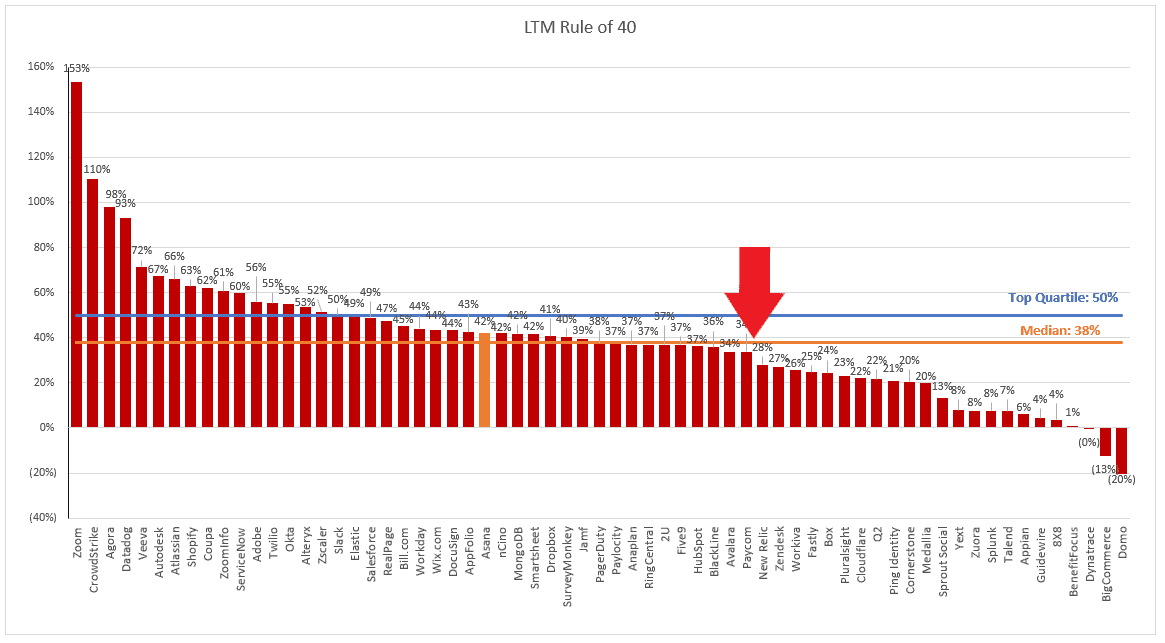

Looking at Palantir’s profitability through the “rule of 40” metric is a better way to compare the company’s growth vs profitability.

The rule of 40 takes the LTM revenue growth rate and adds the free cashflow margin (CFO – CFI).

Palantir’s rule of 40 of 30% is again below the median of 38%.

Palantir “Rule of 40” vs the SaaS Group

The company is still losing money while also growing slower than a majority of software peers which is concerning.

We need to see a pickup in growth or a big increase in the cashflow margin for this stock to be worth a purchase when there are already so many attractive SaaS stocks growing faster for not much more money.

24% of Shares Can be Sold on Day 1

The performance of Palantir in the first few weeks after going public will depend on how many shares can be freely sold by insiders.

In the direct listings for Slack and Spotify, more than 80% of shares could be freely sold as soon as the stocks started trading.

Palantir management no doubt saw the weak stock performance of both companies in the months after listing and is trying to avoid the same outcome.

To do this they’ve gotten shareholders of 75% of the stock to agree not to sell their stock until 3 business days after financial results for the year ending 2020 are released.

This means Palantir’s “share unlock” date will fall sometime in late January 2021.

With only 25% of shares free to be sold immediately, we think Palatir’s stock will behave more like it would in a typical IPO.

The scarcity of shares due to the lockup will prevent the stock from falling as much as we saw in the Slack example (40% fall), until the share unlock in January when the stock price will likely take another leg down until the equilibrium price is reached.

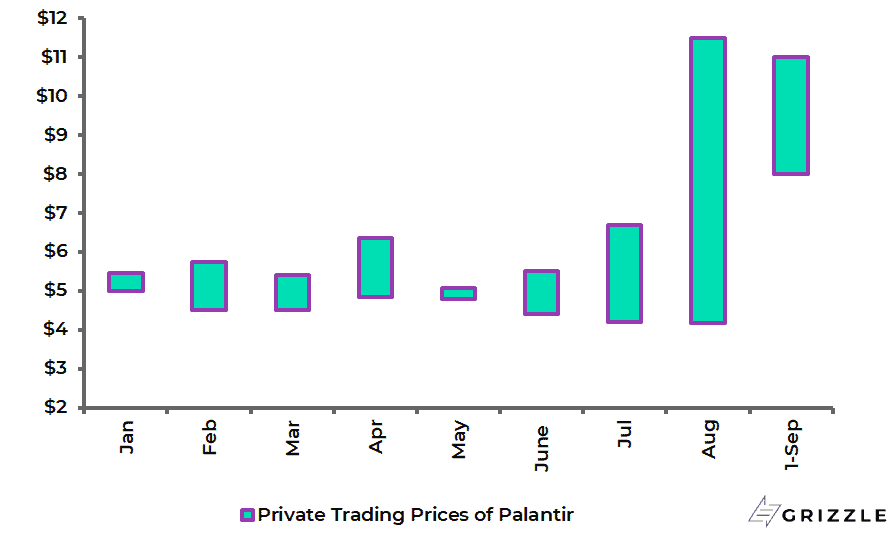

Palantir Worth $9-$12/sh Based on Private Trades but Will Open 50%-75% Higher.

Palantir’s recent private transactions will set the tone for how high the stock trades on its first day.

Looking at private transactions over the past nine months we see a big increase in the value investors are willing to pay leading up to the direct listing.

Palantir stock traded for as much as $11.50/sh in late August and this will likely serve at the “reference price” for the stock on day 1.

Recent Private Trading Price of Palantir Stock

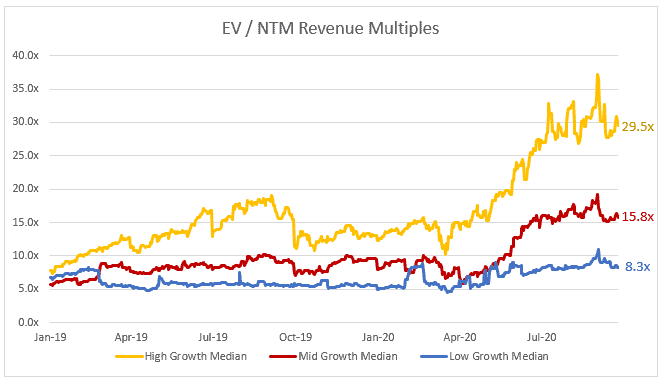

Palantir’s revenue growth is above average but not best in class and is expected to slow to slightly above 30% next year according to management.

Looking at group multiples, Palantir shouldn’t trade higher than 25x revenue which would still put it firmly in the high-growth valuation bucket even though growth is closer to the Mid-growth bucket.

SaaS Revenue Multiples Compared to Revenue Growth

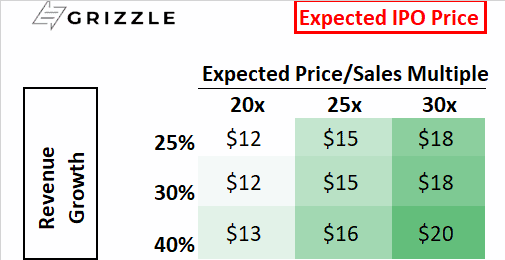

With expected revenue growth of 35% over the next twelve months and our expected revenue multiple of 25x, we think the best case price for Palantir on the first day of trading will be $16-$20/sh.

Where in that range will all depend on how investors are feeling that day, if markets are down, the stock could be on the low end, if markets are green the stock could hit $20.

Expected Price Range on Day 1

The range of $16-$20 is merely a trading price in the middle of a software bubble and during a period when demand for the stock likely exceeds artificially low supply.

What matters longer-term for investors is what the stock is worth based on the fundamental cashflows of the business.

Here the stock is less compelling if it trades at $16/sh or above.

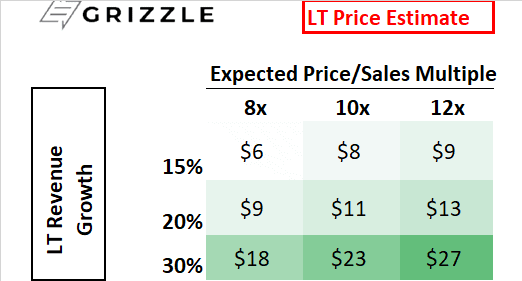

In the example below, we assume Palantir can keep growth steady at an average of 20% a year, which would put it in an elite league with the likes of Amazon, Microsoft, Salesforce, Adobe and other tech juggernauts.

This is a bullish forecast for a stock that was growing below 20% in 2017 and 2018.

Assuming a price to sales multiple of 8x-12x, in line with the long-term industry average and taking into account slower growth, Palantir isn’t worth more than $16.

What has changed to justify a doubling in the value of this company?

Honesty we can’t find anything.

A $16 stock implies good growth, but most importantly significant profits over the next decade, compared to deep losses right now.

For Palantir to offer long term upside for investors who buy above $13/sh, the company will have to grow revenue at a 30% annual rate, or better, for the next 9 years, a heroic outcome based on how the business operates today.

The Fundamental Value of Palantir

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.