Moving away from the financial markets, this writer attended, of late, two starkly different conferences in Europe in an unofficial capacity.

These were not narrowly focused investment conferences.

Both were interesting but of very different political persuasions.

The first was the Delphi Economic Forum in late April which is a kind of mini-Davos focused on Southeastern Europe.

There were an enormous number of panels on Ukraine and much debate on Turkish-Greek relations with both countries having general elections last month.

On Ukraine, the Western media narrative prevailed with much talk of a united Europe against a “common enemy” with many speakers making the point that they had never seen Europe more united.

Still there was a grudging acknowledgement that the “Global South is not responding to this narrative” as one speaker observed.

Another speaker noted that two-thirds of the world are not supporting sanctions against Russia and warned against the consequences of implementing so-called secondary sanctions as some have been pushing for.

South Korea’s exports to Kyrgyzstan are up 415% YoY over the past year, for example, compared with a 24% YoY decline in its exports to Russia.

The same speaker also warned that the track record on the International Criminal Court is controversial in the Global South.

This is of a certain relevance given the 70,000 registered war crimes already alleged against Russia.

But perhaps most interesting was a former Polish foreign minister who advocated “strategic patience” on Ukraine warning that the much-anticipated spring offensive would be “unwise” needlessly risking many Ukrainian lives.

He advised using the much of US$587bn of Russia’s frozen foreign exchange reserves as a bargaining chip in negotiations with Moscow.

Clearly, many in Ukraine are hoping that this money can be deployed in the post-war reconstruction of the country, the cost of which speakers at the conference put at more than US$400bn.

Still the legality of such a move, or rather the lack of it, could create a dangerous precedent, as was acknowledged by one speaker.

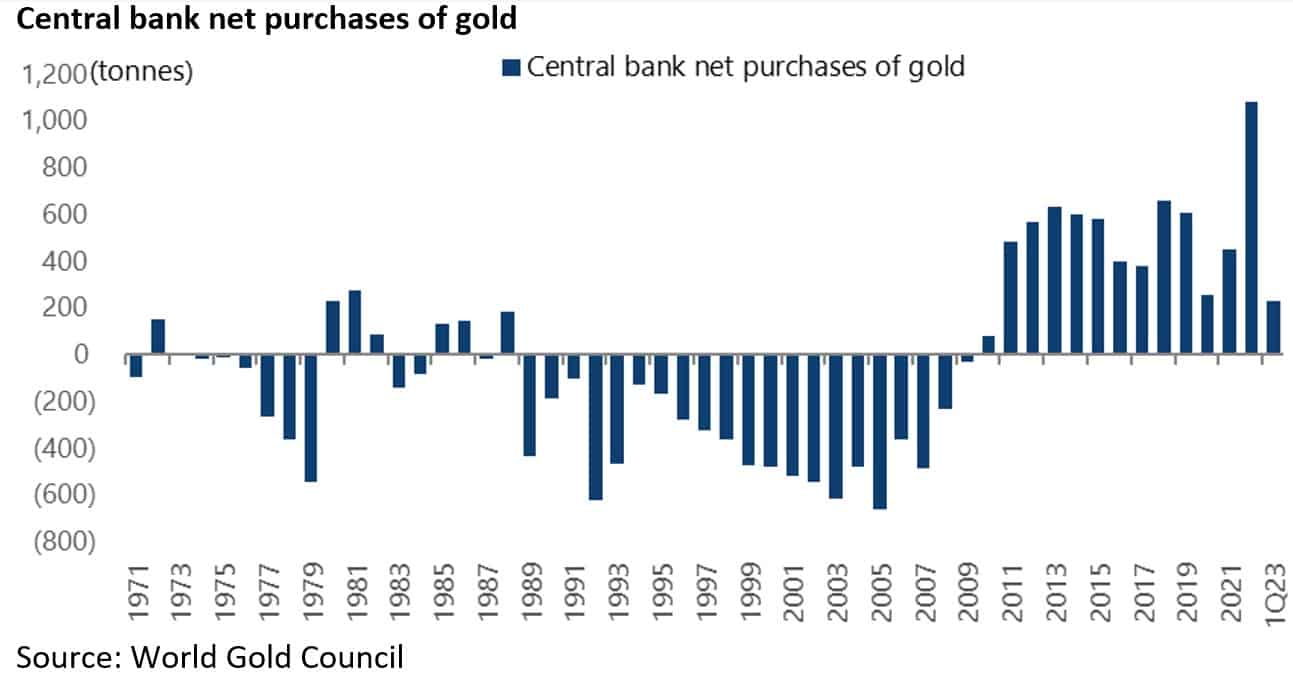

The long-term consequences of that decision could prove profound consequences, as hinted at by the record central bank buying of gold last year which has continued into the first quarter of this year.

Central banks’ net purchases of gold rose from 450 tonnes in 2021 to 1,078 tonnes in 2022 and a further 228 tonnes in 1Q23.

Handicapping the Chances of a Settlement in Ukraine

Meanwhile the hopes of a negotiated settlement on Ukraine are not zero since China has an interest in acting as a peacemaker, just as Beijing won plaudits for brokering the detente between Iran and Saudi Arabia.

It also, arguably, has some leverage on Moscow.

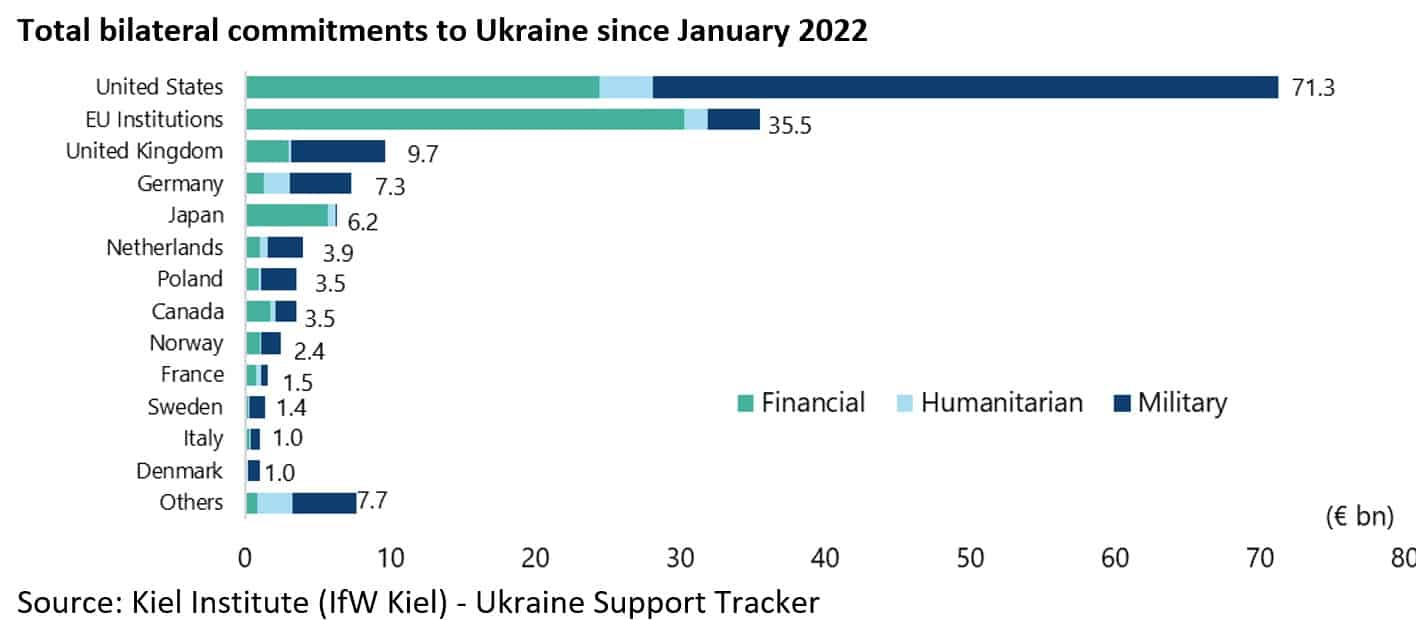

Still it is also the case, from a Ukraine perspective, that the longer the Ukraine conflict continues, and the more costly it becomes with €71bn so far spent by America and €74bn by Europe, the more opposition could build in the forthcoming US presidential campaign with some of the likely Republican presidential candidates opposed to the current policies.

The two Republican candidates currently leading in the polls, namely former president Donald Trump and Florida Governor Ron DeSantis, both appear to oppose the present policy on Ukraine.

Takeaways from the CPAC Hungry Conference

If Ukraine was the subject of much discussion in Greece, that country was much less focused on in the second conference in early May that this writer paid a visit to in Budapest, namely CPAC Hungary, even though Hungary is geographically nearer to Ukraine.

The political complexion of the conference can be construed from the banner at the entrance to the event which proclaimed proudly “No Woke Zone”.

Hungary is clearly a controversial country in the EU context with Brussels still holding up funding from the NextGenerationEU Recovery Fund as reported last month (see Financial Times article: “EU funding to Hungary still frozen despite concession on rule of law”, 5 May 2023).

This writer does not want to get into the details of the above dispute save to note that Hungarian Prime Minister Viktor Orban has been elected to power in four consecutive elections since 2010.

But what this writer was not previously aware of was the powerful tax-incentive policies Hungary has implemented to encourage births within families since 2019.

These are worth spelling out in some detail.

It should be noted that the policies are in the context of a flat rate of income tax of 15% and a corporate tax rate of 9%.

Hungary grants women who give birth to and raise at least four children a lifetime exemption from personal income tax on income derived from work.

Families with three children or more can also apply for a HUF2.5m non-repayable grant (€6,760 based on the current exchange rate) towards the purchase of a seven-seater vehicle.

A woman aged between 18 and 40 in her first marriage, and in employment for at least three years, is eligible for an interest-free loan up to HUF10m (€27,000).

A third of such a loan is cancelled when a second child is born, and the entire debt is forgiven following the birth of a third child.

The government will also deduct HUF1m (€2,700) from the mortgages of young, married couples after the birth of a second child and HUF4m (€10,800) for the third child and HUF1m for each additional birth.

Meanwhile, from January young mothers under the age of 30 will also be exempted from paying personal income tax until they reach the age of 30.

These are dramatic measures to incentivise bearing children within families, the most selfless act humans can undertake.

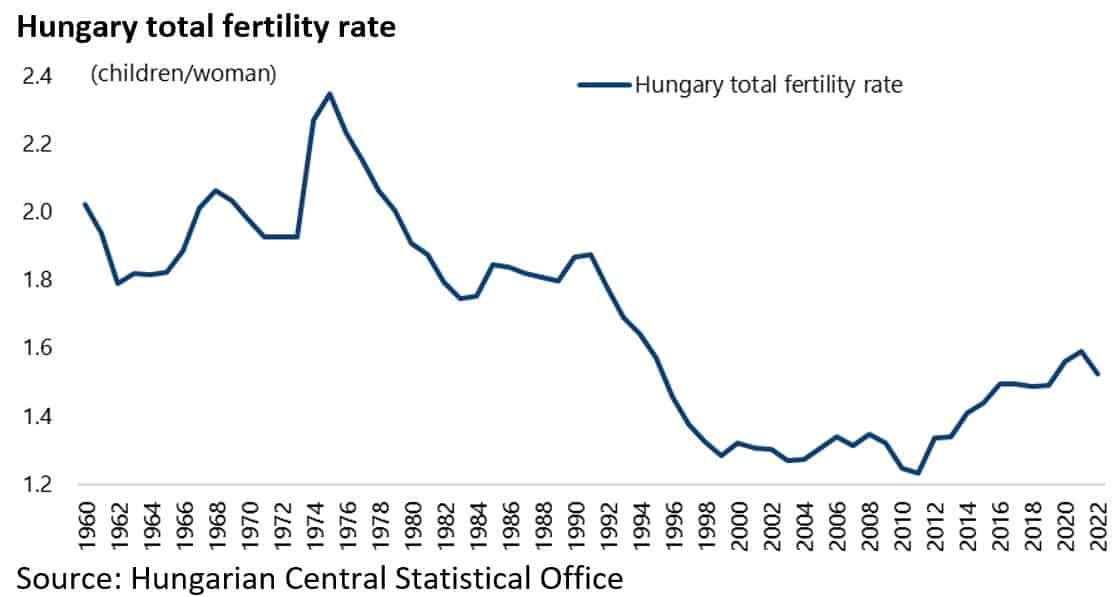

The interesting point is that the fertility rate has improved since Orban’s election in 2010 though, admittedly, from a low base.

The fertility rate has risen from a low of 1.23 children per woman in 2011 to 1.52 in 2022

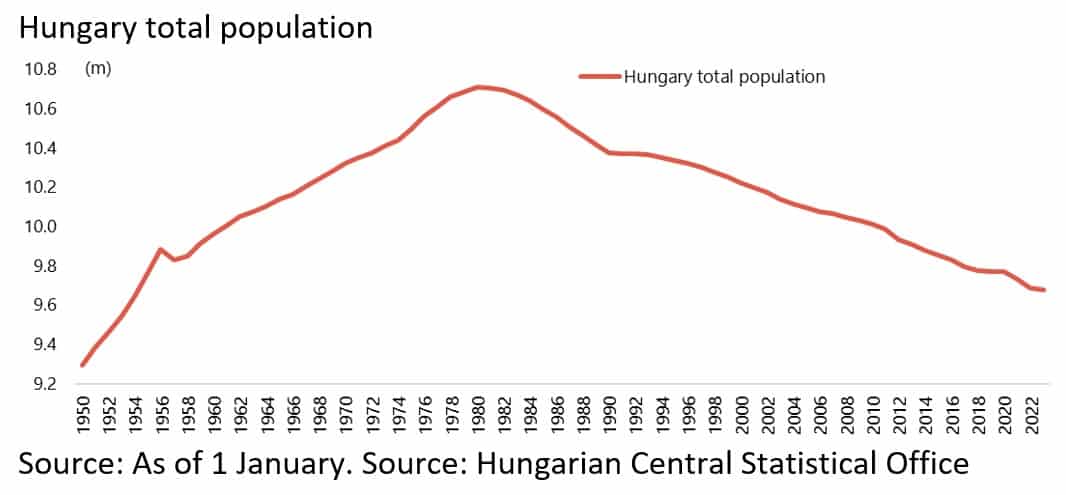

The stated aim is to reach 2.1 by 2030 at which point the population stops declining.

Such dramatic tax incentives are certainly what is needed in Asia where fertility rates in Hong Kong, Korea, Taiwan, Singapore, China and Japan are currently 0.70, 0.78, 0.89, 1.05, 1.18 and 1.27, respectively.

Still there is one problem in Asia, not shared by Hungary.

That is the cost of buying properties as a result of the reality of expensive residential properties in densely packed cities.

But that should not stop governments from trying.

Greece’s Macro Story is Rapidly Improving

Returning to Europe, it is worth noting the dramatically improved macro story for Greece, which was the big victim of the Eurozone crisis ten years ago.

Growth is well above the European average while the country is now running a primary surplus of €2.29bn in the first five months of 2023.

This measure excludes net interest payments on the government debt.

Greek real GDP rose by 2.1% YoY in 1Q23 and 5.9% YoY in 2022, compared with 1.0% YoY and 3.4% YoY, respectively, in the Eurozone.

One following wind for Greece, and other Southern European countries, is the continuing financial flows from the EU recovery fund.

And in Greece’s case, unlike Hungary’s, there is no risk of Brussels withholding funds since, as The Economist recently noted, Prime Minister Kyriakos Mitsotakis is “one of Brussels’ darlings”.

With the ECB continuing to raise rates and credit tightening accordingly, there will likely be rising recession concerns in Europe in coming months.

But it is clear that the Southern countries receiving these funds are better positioned than the North of Europe which is supplying the money.

Growing Economic Pressures in Germany

Meanwhile if the Southern part of the Eurozone looks more resilient, a reminder of the growing pressures facing the German economy has come with the latest macro data.

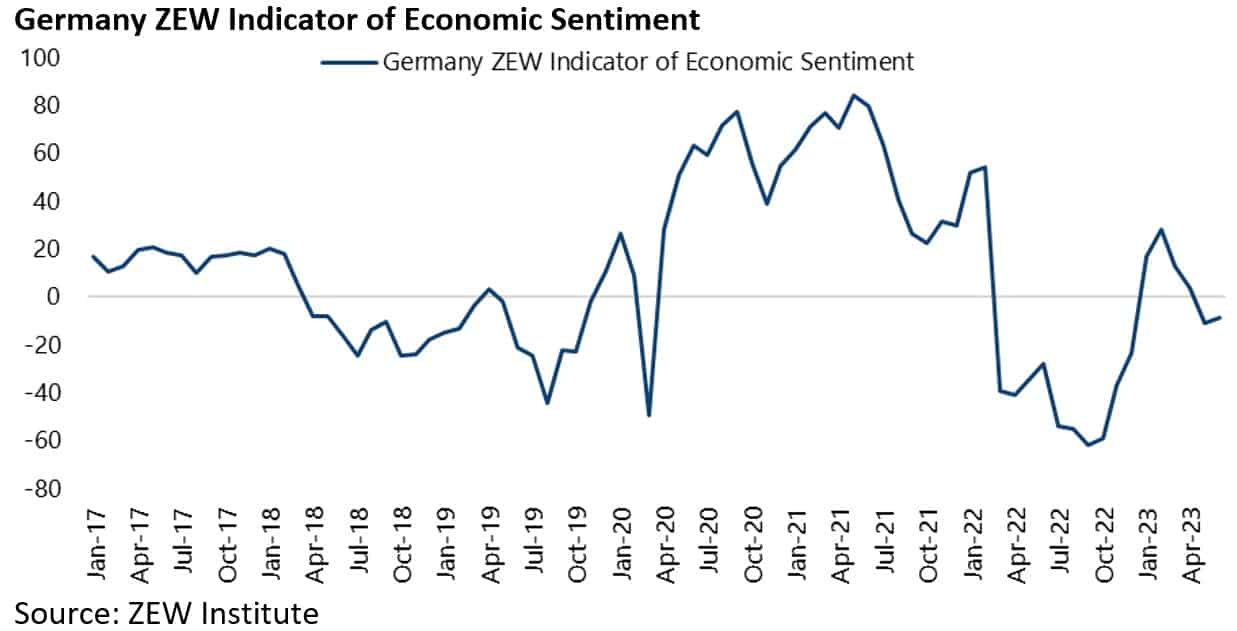

Thus, the ZEW Institute’s Economic Sentiment Indicator for Germany fell to a negative 10.7 in May and a negative 8.5 in June, down from 28.1 in February.

German real GDP declined by 0.5% YoY in 1Q23.

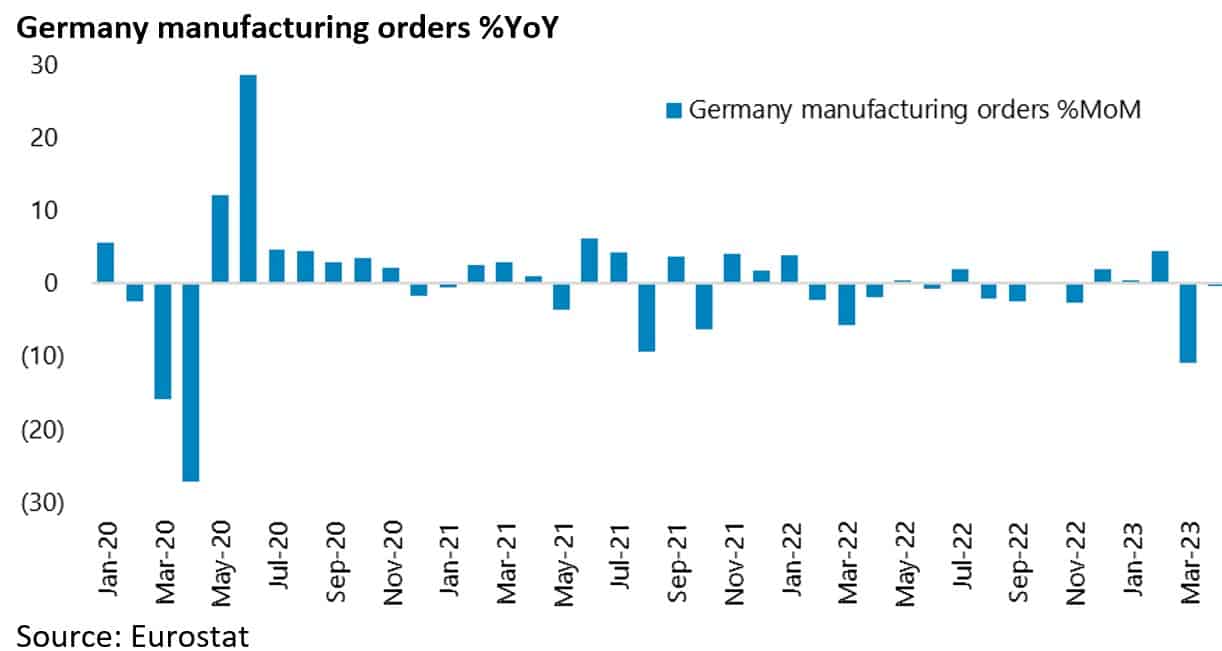

While manufacturing orders declined by 10.7% MoM in March, the biggest decline since April 2020, and were down 0.4% MoM in April.

The German economy is coping not only with the loss of cheap Russian energy but the costs of funding both de facto Eurozone fiscal integration and re-armament.

This is not to mention the existential challenged facing the German auto sector, the country’s largest, in terms of the transition to EVs.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.