If anybody was in any doubt that cyclical stocks would rally sharply on the re-opening trade, they got the evidence they needed with the parabolic market moves on 9 November on the original Pfizer news.

Pfizer announced that its Covid-19 vaccine was found to be more than 90% effective in preventing Covid-19 in the first so-called “interim efficacy” analysis.

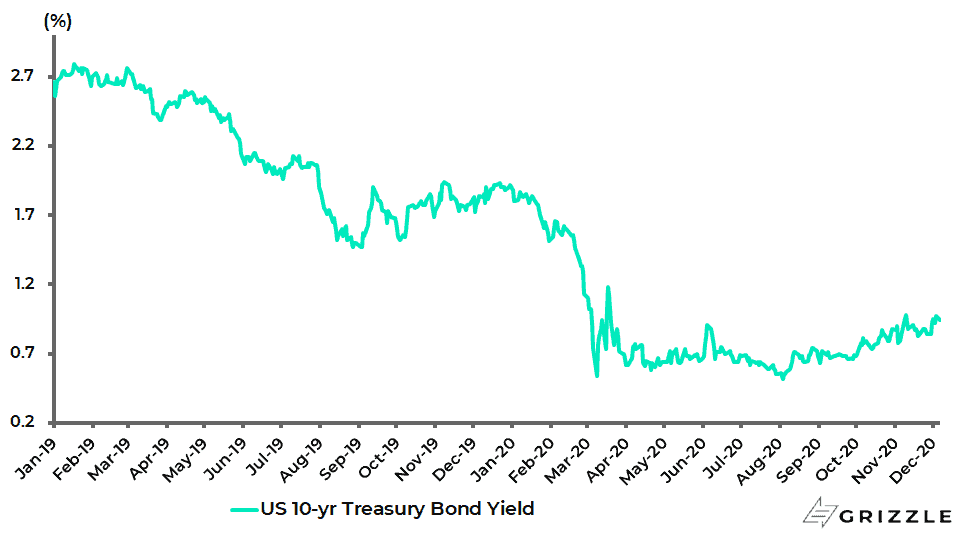

The action was not only in cyclical stocks but in the biggest sell-off in the 10-year Treasury since mid-March.

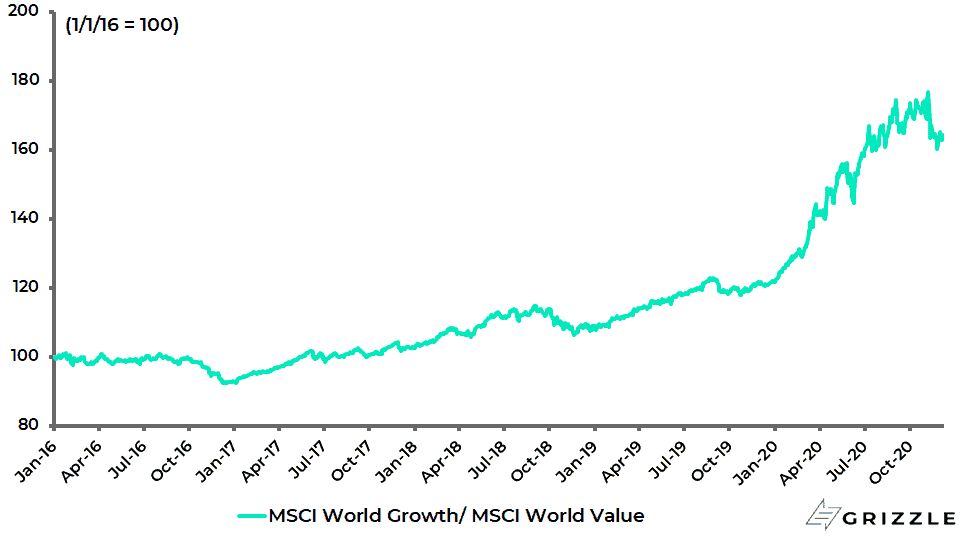

The MSCI World Value Index rose by 4.2% that day while the MSCI World Growth Index declined by 0.7%.

As for the 10-year Treasury bond yield, it rose by 10.5bps to 0.924%, the biggest increase since 18 March.

US 10-year Treasury Bond Yield

Since then, of course, the vaccine story has moved and cyclical stocks have continued to outperform.

Moderna announced last week that the final result of its phase-3 study shows that its vaccine is 94% effective.

Both Pfizer and Moderna are now seeking the US Food and Drug Administration (FDA) for emergency use authorization.

This market action indicates the merits of the long-advocated strategy here of pursuing a barbell approach of owning both growth stocks and cyclical stocks.

Clearly, how much an investor wants to bet on the “tangible” cyclicals against the “intangibles” depends on the time horizon of an investor since digitalia is an ongoing theme.

Still, the outperformance of cyclicals could be dramatic on a real re-opening since it is not an everyday occurrence when economies are locked down by government fiat.

It also remains the case that the policies undertaken in response to the pandemic have likely unleashed a regime change in the investment climate, in terms of the return of inflation as discussed here on several occasions. It is also the case that the dramatic outperformance of growth stocks over cyclicals in recent years means there is a lot of room for gaps in the chart to be filled even if it turns out, ultimately, to be only a countertrend move.

The continuing potential for mean reversion is highlighted in the chart below.

MSCI World Growth Index relative to MSCI World Value Index

What about the vaccine news itself?

This writer’s conversations with biotech experts in recent months has made clear that there is little doubt that there will be more than one vaccine readily available by the middle of next year since the technology has improved dramatically for “mapping” viruses since when AIDS first appeared in the 1980s.

The bottleneck is rather producing the vaccine on a mass scale.

Meanwhile, the political significance of the Pfizer and Moderna news is that it gives politicians cover to end renewed restrictions on mobility sooner rather than later.

On the controversial lockdown issue itself, this writer recommends reading an open letter by 200 French lawyers translated into English in the British weekly publication, The Spectator last month (“Liberté! An open letter by 200 French lawyers protesting against lockdown”, 7 November 2020).

The letter is about the implications of what the co-signees describe as the “zero-risk” society, in terms of the willingness to sacrifice everything to prevent the threat of infection.

In truth, this is just another manifestation of the nanny state or, in the context of the financial markets, the willingness to bail out everybody and anybody as a result of central banks’ growing willingness to underwrite credit risk.

Indeed the panicky response to the pandemic in the G7 world has been, in many respects, quite predictable in the context of the policy responses in the Western world to the global financial crisis.

What about America? President-elect Joe Biden is still worrying about a “dark winter”.

But the interesting issue is whether a Biden administration will be more focused on the economy and less on Covid now that the White House is seemingly secured.

The expectation here is that America will avoid renewed lockdowns.

That said, the view here remains that the Fed will remain doveish even in the context of the arrival of vaccines and the passing of the pandemic.

This writer also continues to believe that the Fed will react to rising long-term government bond yields on such a re-opening trade (i.e. the type of market action seen last week when the 10-year Treasury bond yield rose to 0.97%).

Meanwhile, the appointment of former Federal Reserve Chairwoman Janet Yellen as Treasury Secretary symbolises perfectly the growing convergence of fiscal and monetary policy in America.

On the same subject, a remarkably frank speech was made earlier this quarter on the inevitability of monetisation.

This writer refers to comments made by Randal Quarles, the Fed Vice Chair for Supervision, in a virtual event at the Hoover Institution. The central banker observed that the “sheer volume” (i.e. size) of the Treasury bond market may have outpaced “the ability of the private market infrastructure to support stress of any sort there”. Or in other words, the Fed will need to fill in the gap, which means more monetization and another reason to buy more gold and more Bitcoin. Remember the two are not mutually exclusive.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.