The US cannabis industry is one of the most attractive growth sectors in the stock market for investors.

The industry offers big top-line growth and companies who are cracking open a completely new legal market.

However, investing in emerging growth industries is inherently risky.

Most stocks will fail to live up to their hyped growth expectations and many will go to zero.

Grizzle has been covering the cannabis sector since its infancy, in fact we launched our company in 2018 with a short report on the overvalued Canadian cannabis sector – the first in-depth analysis of the ills that would soon impact the frothy stocks.

We believe we’re at a very attractive juncture for the US cannabis market, sector-level valuations are reasonable relative to the significant growth runway ahead for the sector.

However, company-specific risks are still significant and we believe investors should take a laser-focused approach (fundamental stock selection) rather than a generic scattergun approach (ie. market weight cannabis ETF).

Enter the Grizzle cannabis portfolio.

To help investor’s we’ve created a fundamentally driven cannabis portfolio with a focus on avoiding companies headed to zero while at the same time maximizing upside through valuation and fundamental analysis.

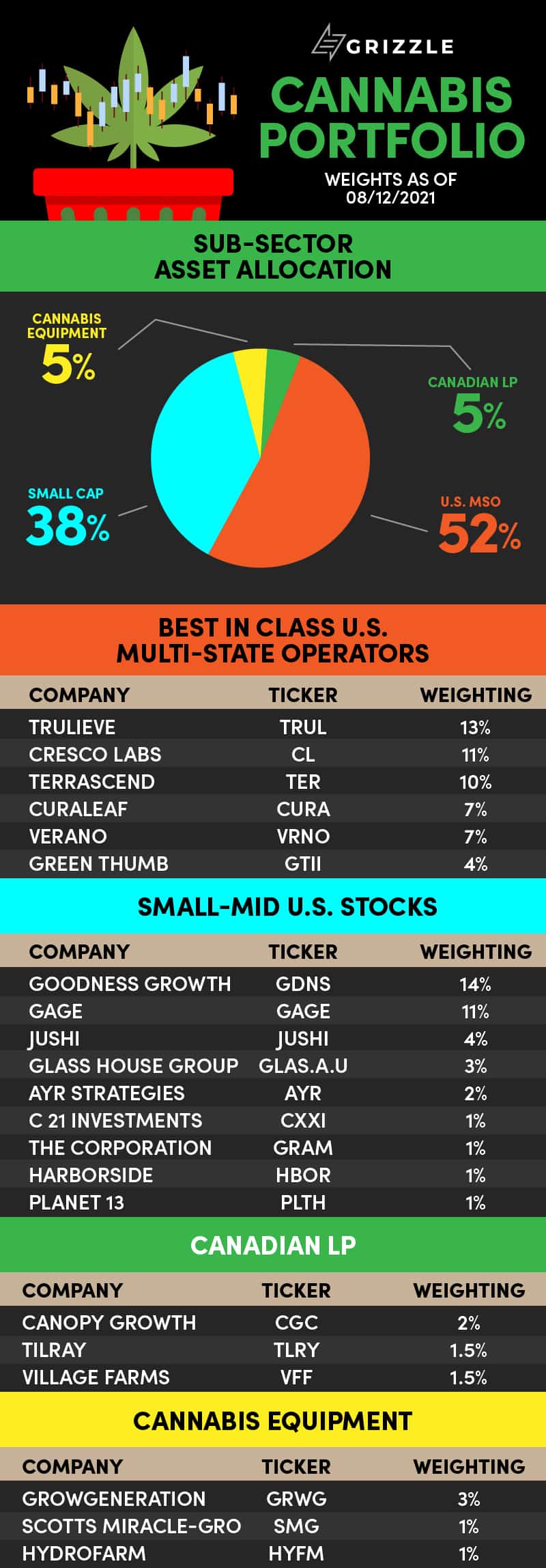

Below is our full portfolio asset allocation as well as explanations of how we assigned all of our individual company weights.

*Check back regularly as we will be posting all portfolio changes here when our industry and stock-specific outlook changes. Check this YouTube LINK for an in-depth conversation of all the most recent portfolio changes.

Our Current Thoughts on the Cannabis Industry

Cannabis stocks are a long way from the euphoric days of February 2021.

We think investors got a little too bulled up after the suprise democratic victories in November and January and then when legal change did not come, the air came out of market expectations.

Once it became clear that investors could be looking at a long wait until meaningful cannabis reform was passed, volumes declines and many investors sold locking in their quick gains made over a 4 month period.

We are now 4 months into a drawdown that has seen even the best stocks fall 35%.

% Off High for 4 Large US Cannabis Stocks

The Grizzle portfolio is positioned for the eventually passage of meaningful legislation, whever it will come.

We think Schumer’s comprehensive cannabis bill in the senate will ultimate die off and a simpler bill that really moves the needle like the SAFE banking act or STATES act will be passed.

Even if a bill that allows normal banking services and stock market uplisting takes longer than expected, we are heavy into stocks that will grow cashflow significantly faster than the market regardless.

We also own smaller US operators who will outperform their larger peers if a bill does eventually pass.

In our opinion the U.S. is a much more attractive growth opportunity than investing in Canada and the portfolio reflects that view.

U.S. MULTI-STATE OPERATORS

For the best in class US Multi-State operator group our weightings were driven by the level of net debt and the enterprise value to EBITDA multiple plus some qualitative factors.

Multi-state operators are the companies who own one of a limited number of states licenses.

Demand that exceeds supply in many of these markets means the companies have been given a license to print cash.

These companies win even if no new bills are passed and are a core holding in the Grizzle cannabis portfolio.

SMALL-MID CAP US STOCKS

Our weightings in this group were led by net debt, the price to sales ratio, and also the potential of a buyout.

Small-cap cannabis stocks provide a potentially attractive way for the bigger guys to enter new states quickly without the permitting hassles that can push off licenses for years.

These companies have room for faster growth and more rapid cashflow improvement than the big MSO’s and are how we are positioned for the eventually passing of a bill that will give these companies access to traditional bank loans and uplisting to big US exchanges.

They may lag the big guys at times but when the cannabis sector is outperforming the market, small and mid-cap stocks are the torque in our portfolio.

CANADIAN LICENSED PRODUCERS

The only thing Canadian investors want to hear from management teams is how they plan to enter the U.S. market and how soon it’ll happen.

Growth is hard to come by in Canada, making the US the far superior market.

For our Canadian weightings, cash was king, with valuation as a secondary factor.

If you want to enter the U.S. you need cash to buy your way in.

We own Tilray for its diversified global portfolio of assets, Canopy Growth for access to the US and Village Farms because it has the lowest growing costs in Canada and provides some of the best quality cannabis for the money.

Tilray and Canopy are plays on passage of the US STATES act or SAFE Banking, while Village Farms also has some US optionality but is more a Canadian best in class holding.

When cannabis comes back into favor the Canadian stocks will rip, and even though our weighting to Canada is much lower than to the states we wanted at least a bit of exposure.

CANNABIS EQUIPMENT

Cannabis equipment companies are the supplier to both professional and amateur growers.

As long as the industry grows more cannabis every year, equipment companies will grow as well.

They do not care if the retail or wholesale price of cannabis goes up or down, only that people are growing it.

Equipment stocks are “non plant touching” which makes them easier, from a compliance standpoint, for big institutional investors to own.

GrowGeneration was the best performing cannabis stock in 2021 and drove much of our returns in 2020, but the stock is now looking mucho expensive.

Even so it is the fastest growing equipment pure play in the space and remains a core holding in the equipment sector for us.

Full Disclosure: Employees of Grizzle own securities mentioned in this article.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.