Bottom Line

Lyft (NASDAQ: LYFT) put out strong earnings this quarter, beating consensus on both the top and bottom line, but the news that the stock lockup will end a month early will largely overshadow these results.

Lyft decided to move up the share unlock date to Aug. 19, from Sept. 24. This decision means the lockup will be hanging over the head of every investor for the rest of the month.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]With 257 million shares, or more than 90% of shares outstanding coming off of lockup, the stock could see some selling pressure leading up to and through the lockup expiration. Employees and management have an average cost basis of $23.50 so are sitting on 170% gains on average.[/su_panel]Moving back to the fundamentals, we think a beat on revenue and EBITDA will now be overshadowed by losses that continue to grow and weak guidance for user growth over the next two quarters.

If you are day trading this stock, come back in September, but for those with a longer time horizon, we recommend stepping back a bit to take a hard look at what you own.

Lyft’s expenses grew 79% year over year, faster than revenue, up only 71%. On an absolute basis, revenue was up $360 million, but costs increased $550 million, widening the company’s losses to $1.5 billion on an annual basis.

Expenses have been outgrowing revenue consistently making it hard to see when or how the company will eventually turn a profit.

Call us haters if you want, but there is something wrong with the rider economics of this business that we just can’t get past, even if revenue growth is pretty darn impressive.

We went through the numbers in-depth in our Uber deep-dive, but in a nutshell, the costs to service the current rider base are not declining as they should in a rapidly growing business.

We’ve been told there are economies of scale in tech-heavy businesses, but at Lyft we just aren’t seeing this.

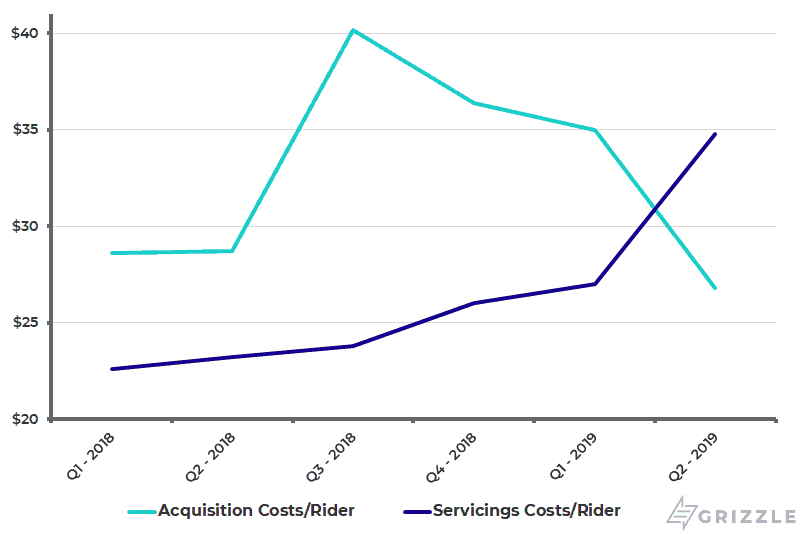

Lyft spent $35 to support each rider in the latest quarter, up from $23 a year ago even though six million new riders joined the platform.

Support costs include the driver’s cut of a ride, call centres and the cost to build and maintain driver centres among other expenses.

The company tells us they are investing in growth, which explains the higher support costs, but we aren’t touching this stock until management can show servicing costs are going lower on a long-term basis.

Even if management were to cut marketing to zero, which would introduce its own growth problems, they will continue to lose money unless they can fix what looks to be broken per rider economics.

Costs to Service a Rider are Still Going up Even as the Company Grows

At an ~$18 billion valuation, Lyft is going to flounder until the company can prove there is a clear path to profitability or they find a way to reaccelerate rider and revenue growth.

Our preferred way to play ride-hailing stocks is through a pair trade.

Buy Uber to take advantage of it’s better underlying economics, 12% lower multiple and lower per ride losses while shorting Lyft.

Uber’s CEO looks to be tightening his belt, which could show up in losses shrinking faster than at Lyft, which the market would love.

We think this is a low-risk way to play the ride-hailing opportunity without knowing if the business model is really and truly viable longer term.

Operational Review

After a less than stellar debut on public markets, this quarter’s earnings report is being well received by the market with the stock still up 5% as we are writing this. Lyft exceeded revenue expectations by 7% and increased revenue guidance for 2019 by 6%.

The company also decreased the expected EBITDA loss in 2019 by 25% to $860 million from $1.2 billion, which is solid, but still far from a positive number.

Forward guidance from the company was mixed. On the one hand Lyft upped revenue guidance for 2019 to an average of $3.48 billion from $3.28 billion, but guidance for rider growth through the rest of the year was 20% or so compared to 40% year-over-year growth in the first six months.

This slower rider growth is likely due to price increases that took effect in June. Revenue growth should benefit but at the expense of rider growth.

Despite the large losses, the company did continue to post impressive growth numbers, however. Quarterly revenues grew 70% year over year, active riders grew 41% year over year and revenue per active rider grew 22% year over year.

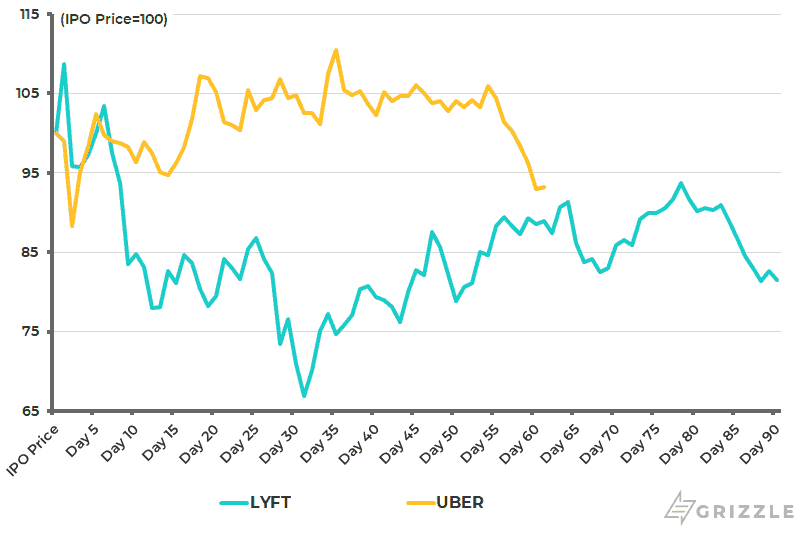

Since the Lyft IPO on March 29, the stock has not performed well, down over 16% from the IPO price of $72.

Compare this performance to Uber which is down about 6% from its IPO price.

Uber and Lyft have had the weakest debuts among the big tech IPOs this year with other companies like Pinterest (NYSE: PINS), Slack (NYSE: WORK) and Zoom (NASDAQ:ZM) up 15%-180%.

Share Performance Since IPO of Uber and Lyft

Overall this earnings release did nothing to reassure investors that Lyft will one day be a profitable ride-hailing juggernaut.

The stock could go higher if the company keeps beating on earnings and raising guidance, but with a premium multiple and a questionable cost structure, Lyft is not the growth stock you want to own for the long term, yet.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.