https://youtu.be/QRuB-zar7A8

The potential of ride-hailing platforms like Lyft, Uber, and Didi cannot be denied. Lyft, in particular, is attempting to set a stock market milestone by being the first ride-hailing company to go public. Until Uber hits the market in a month or two Lyft will also be the largest publicly traded stock in the “gig” economy. The investor reception and valuation the Lyft IPO receives will set the tone for all the ride-hailing competitors who follow.

This one of a kind guide ahead of Lyft’s IPO answers all of your most pressing questions:

- How does the ride-hailing business model work?

- Can Lyft make money outside of ride-hailing?

- Is Lyft holding its own against Uber?

- What do drivers think of Lyft?

- When will self-driving cars arrive?

- When will the company break even?

- Will Lyft run out of money if they don’t turn a profit soon?

- Who owns the shares and is there a lockup?

- Should I buy the stock on the Lyft IPO date?

and much more….

Lyft on the Bleeding Edge of Shift Towards Transportation as a Service (TaaS)

In the past there was a tangible value associated with ownership of a car. Owning your own car meant freedom to travel when and where you wanted. Car ownership was a status symbol and a statement of individual style based on the make or model of the car. But then came the sharing economy. Society is starting to get used to sharing assets like cars with others for the sake of convenience and reduced upfront costs. Why pay a down payment and regular monthly payments to own a car that will be parked 95% of the time?

Along came ride sharing. The 21st century equivalent of carpooling, with a twist. Forget coordinating with friends and co-workers to arrange a ride or figuring out parking or paying for gas; there’s an app for that!

Companies like Lyft and Uber in North America and Didi, Ola, and Grab in Asia got in on the ground floor of ridesharing and created a new category for transportation, transportation as a service (TaaS).

The endgame for TaaS operators like Lyft, is a complete rethink of how people move from A to B. The addressable market is equivalent to the entire transportation expenditure for a household. In the United States alone that market is over $1.2 trillion.

The shift towards TaaS has the potential to disrupt huge long-established markets like automotive manufacturing, public transit, and even real estate.

Lyft’s Tech & IP – Tech Company or Marketing Platform?

Enabled by the digital revolution, consumers in the modern world expect everything on-demand. Ride sharing companies provide their customers with the instant gratification of knowing the moment you click that button in the app, a car will be on its way to take you wherever you need to go.

Matching rider to driver is at the heart of Lyft’s technology. Figuring out how to get a person from A to B is easy, however, ensuring that there is a driver who can reach a person quickly enough to satisfy those on-demand expectations and get them to where they need to go for a reasonable cost is more complicated.

You need a critical mass of drivers in a particular area and incentives for both the riders and drivers to use your platform. That’s why Lyft spends more than twice as much on Sales and Marketing as it does on Research and Development to retain drivers and riders on the platform (37% compared to 14% of revenues in 2018). Not what you’d expect to see from an emerging ‘tech company’.

The focus of Lyft’s technology is in utilizing the massive amounts of data they are gathering from the over 1 billion rides they’ve facilitated thus far. That means finding ways to optimize pricing for both riders and drivers to improve user retention and revenue per ride.

Convenience is one of the main draws for riders using Lyft so the company also needs to leverage its treasure trove of data to predict rider destinations, position drivers to maximize efficiency and balance out supply and demand.

The last area of technology-driven focus at Lyft is the prize at the end of the Transportation as a Service rainbow, autonomous vehicles (i.e. driverless cars) — more on this later.

Leading up to the Lyft IPO: An Operational History

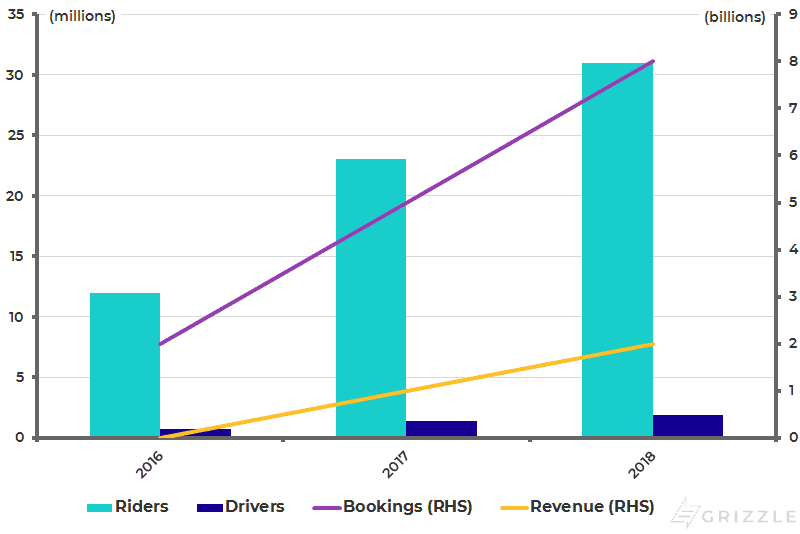

Lyft is seeing rapid growth in riders and drivers. The company boasted 31 million riders in 2018, up from only 12 million in 2016. The company facilitated 620 million rides in 2018, up 65% from the year before and up from 160 million rides in 2016. Total rides are growing even faster than riders as the company is seeing a multiplier effect from existing riders choosing to book more rides than they did the year before. For example, ridership was up 35% in 2018, but the number and total value of rides increased by 65% and 75% respectively.

Lyft Operational Growth

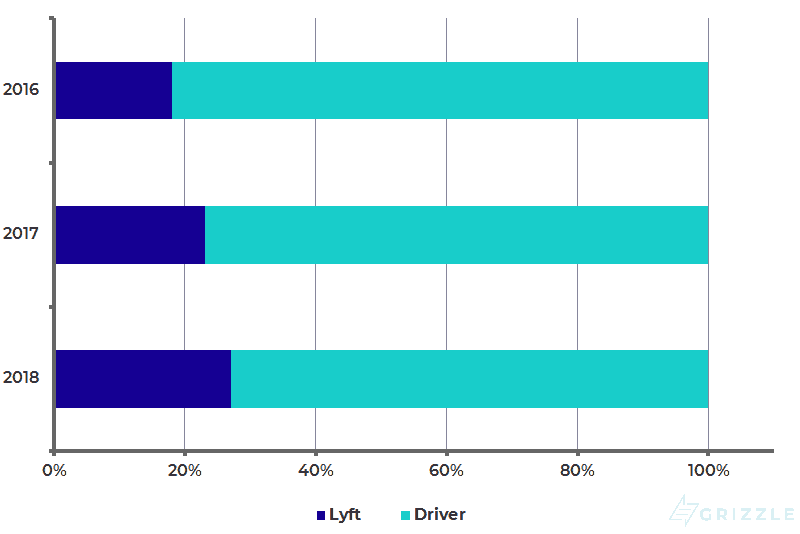

Lyft has also been very successful at taking a larger and larger slice of the fare charged to the rider. In 2016 Lyft took only 18% and gave 82% to the driver. By 2018 Lyft was taking 27%, leaving 73% for the driver.

Lyft/Driver Split of the Fare

On top of a higher cut of the ride, Lyft has drastically decreased driver incentives, which we think was largely due to public missteps by Uber. Uber antagonized drivers and local governments in 2017, allowing Lyft to convert both drivers and passengers to its platform. We think the strong demand among drivers allowed Lyft to cut driver promotions significantly.

Lyft spent $2.60 per ride on sales and promotions in 2016 but brought that number all the way down to $1.30 per ride by 2018. With Uber refocusing on winning back the hearts and minds of the public and drivers we wonder if this is the bottom for incentives and the end of Lyft’s ability to continue squeezing drivers.

Additional Revenue Streams Will Appear

The current economics of ride-hailing do not look particularly attractive judging by the losses both Lyft and Uber are still generating. However, Lyft’s focused and simplified business model will not be the same five years from now. Below is just a sample of potential new revenue sources Lyft can exploit as its platform grows and adapts.

Sell rider data

Facebook and Google have shown that user data has value. Lyft captures millions of data points on rider behaviour, locations, and travel patterns every minute and there will be opportunities for the company to sell access to this information.

Sell advertising and entertainment on mobile and in-car screens

If the Lyft app eventually becomes a resource for riders both before and during a trip, there is an opportunity to sell advertising space within the app to generate additional revenue. The arrival of autonomous vehicles would open up a huge marketing opportunity.

Replace underutilized public transit with ride-hailing

Uber is already doing this with pilot programs in Canada and smaller cities in America. Small towns with limited demand for public transportation can cut down on their operating costs by subsidizing car rides for citizens instead of paying for expensive buses to ferry people around. A pilot program in Innisfil, Ontario, is costing the town $250,000 a year, saving them $750,000 vs owning and running their own public bus service. The revenue opportunity from replacing underutilized mass transit in smaller towns and cities is a significant opportunity longer term.

Self-driving Fleet

The transition away from human drivers is already underway. New cars today come with autonomous features like lane assist, collision detection, and so on. Being able to provide rides to customers without a human driver would remove a significant cost driver (yes, the pun is intended) for Lyft which explains why management is investing heavily in partnerships and research towards fully autonomous vehicles.

While autonomous vehicles are potentially the key to unlocking profitability in Lyft’s business, they will also present several challenges for the company. First, of course, are the technological challenges of ensuring these robot cars will perform as well as human drivers, which some predict may not happen until 2035. Then there will be the inevitable patchwork of different regulations and policies on how to treat driverless vehicles in different jurisdictions where Lyft operates, akin to the many battles the company already faced operating under municipal taxi and livery regulations.

On an even higher level there are bigger uncertainties on the path towards autonomous driving. How many people will want their own private autonomous vehicles vs those who merely rent time on a fleet? Will auto manufacturers start their own TaaS offering and will public transit be able to modernize to stay competitive?

There are also external costs to the environment and society. Even though it’s likely that autonomous vehicles of the future will be electric-powered there is still a potential environmental impact as studies have pointed out that AVs could increase the number of Vehicle Miles Travelled (VMT) due to empty vehicles traveling between pickups. Not to mention the potential societal impact on city planning, traffic, and access to transportation for those with low incomes or disabilities.

There are many ‘IFs’ that need to be answered before Lyft moves decisively into an autonomous driving future. However, in the long run, Lyft needs to incorporate Autonomous Vehicles if it wants to reach the true profit potential it touts to investors.

Autonomous vehicles from a profit perspective really are the holy grail for any ride-hailing company. Self-driving cars will eventually make human drivers obsolete, giving Lyft 100% of every fare instead of paying out 70%-80% to drivers. The potential of a dramatic increase in profitability is what justifies annual R&D expenses in the hundreds of millions for both Lyft and Uber.

Ride Economics With and Without Drivers

| Driver | Autonomous | |

| Value of Ride | $16 | $16 |

| Lyft Revenue | $4 | $16 |

| COGS | $2 | $4 |

| Gross Margin | $2 | $12 |

Source: Grizzle Estimates

Self-driving cars are still at least a decade away according to some industry estimates, forcing these companies to turn a profit while still earning only $0.20-$0.30 cents for each dollar of travel booked through the app.

Affiliate fees for connecting riders to other transportation providers

Both Uber and Lyft are investing in the nascent e-scooter and e-bike businesses and are offering ways of connecting a ride-hail to a scooter or bike ride, thereby up-selling their customers on another service. But beyond scooters and bikes, Uber has already begun testing additional in-app content to help users plan trips through other transportation providers.

In Denver, a user can look up public train and bus times in the Uber app though they can’t yet book travel without going outside the app. Over time ride-hailing companies may allow users to book additional transportation options on buses, trains, or public transit, earning a cut of this additional ticket value.

Growth is Strong but Economics Leave Much to Be Desired

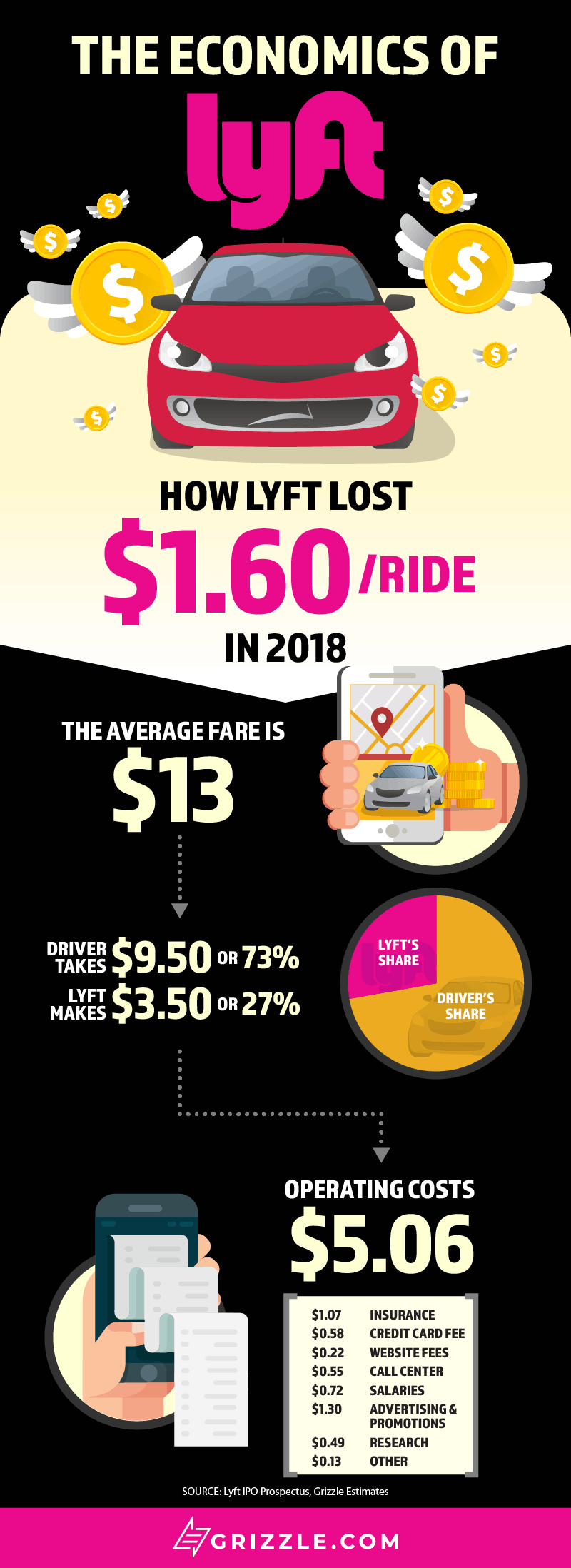

On the one hand this is a company seeing rapid adoption and a growing take of the total ride value, but on the other hand, losses are mounting. Lyft lost $1 billion in 2018, up from a loss of $700 million the year before. Lyft is choosing to go public when the size of the losses are still growing, making it very hard for investors to forecast how management will turn these losses around.

Putting the losses in perspective, for every $13 ride Lyft facilitated, it lost $1.60 in 2018. This is an improvement from losing $4.30 per ride in 2016, but still a long way from profitability prior to the Lyft IPO.

What is most concerning to us is the lack of data showing that economies of scale are kicking in as the company grows. For example, the company increased its take of the value of a ride by 9% over the last two years while the gross margin, which is revenue minus direct costs, increased only 8%. This tells us the direct costs of running the app did not scale at all over a period when the company tripled the rides it gave.

With its current cost structure, Lyft needs to facilitate 1.6 billion rides annually to break even. Given the company handled 600 million rides in 2018 and is growing at 70% a year. We estimate Lyft would break even by late 2021, but only if fixed costs do not increase in coming years. 2021 matches up with the profitability timeline being given out by management to big bank analysts.

Keep in mind that reaching profitability in 2021 assumes corporate costs stay flat going forward which is an unrealistic assumption. After the Lyft IPO as the company grows it will have to staff up call centres, hire new corporate employees and spend more on advertising and R&D, which will all contribute to rising costs. Without a drastic decrease in corporate costs (currently $3.00 per ride), Lyft is going to have trouble turning a profit anytime soon.

Based on a few different sensitivities we have run (explained below), the company will struggle to break even before 2026.

Forecast Operating Income

Base Case: 20% cut of revenue

- Lyft’s cut of revenue falls to 20% from 29% over 5 years.

- No self-driving.

- Ride growth falls from 11% to 5%, falling by 2% a year.

- Operating costs per ride fall at a similar run rate to 2016-2018.

Scenario 1: 26% cut of revenue

- Lyft’s cut of revenue falls to 26% from 29% over 5 years.

- No self-driving.

- Ride growth falls from 11% to 5%, falling by 2% a year.

- Operating costs per ride fall at a similar run rate to 2016-2018.

Scenario 2: Faster Growth

Same as scenario 1, except rider growth is maintained at the 2018 level of 11% per year.

Scenario 3: Self Driving

- Drivers are phased out over a 5-year period beginning in 2025.

- Lyft purchases and maintains its own fleet of autonomous vehicles.

- Vehicle capital and operating costs are added into overall costs.

The Cut Uber and Lyft take has been rising, but Cities and Drivers are Fighting Back

Over the past three years, Lyft has been very successful in increasing its share of the value of a ride by cutting driver incentives and increasing fees drivers have to pay. Revenue is up six times as a result. However, we think there are real risks that may start driving Lyft’s cut back down again.

The economics of driving full time for ride-hailing services are marginal at best with some sources estimating that half of drivers make less than $10 an hour. If Lyft pushes driver earnings down too far they may start to run into driver retention problems, which are already an issue. Just this week, thousands of drivers are striking in Los Angeles to protest recent cuts to their per mile pay.

A more immediate risk to Lyft may be local governments – they are beginning to lobby for higher wages on behalf of the drivers who are also tax-paying citizens. New York City, for example, enacted the country’s first minimum wage for ride-hailing drivers. Average driver pay went up 50% which all came out of the ride-hailing company’s pockets. There is a real risk that increasing competition, regulatory change, and driver pushback reverse recent successes Lyft has made in increasing its share of each ride.

Uber is the Elephant in the Room

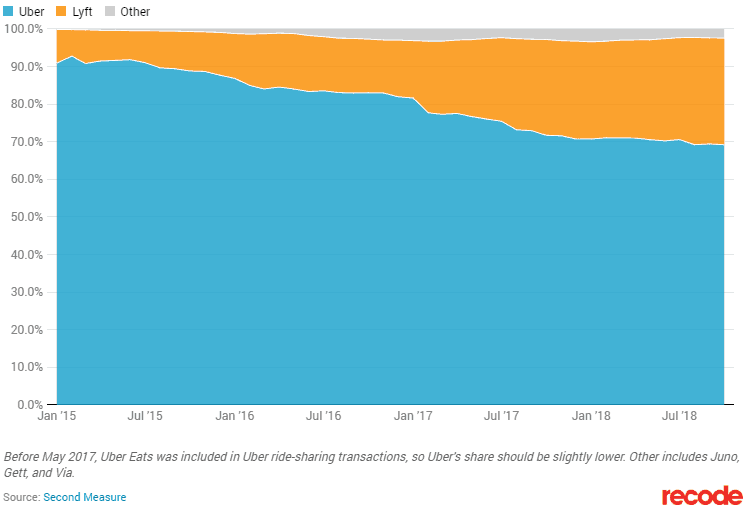

Any investor conversation has to include Uber, Lyft’s main competitor and the clear market leader in North America. The ride-hailing ecosystem in America is defined by these two companies and though Lyft has been gaining market share, Uber still generated the vast majority of on-demand rides in North America.

In 2017 Lyft was the primary beneficiary of a series of public missteps by Uber management. Uber antagonized local governments and drivers, enabling Lyft to stand out as the kinder alternative with more earnings potential for drivers. Lyft is estimated to have grown its share of the market to 30% in 2018, from less than 15% in 2016, all at the expense of Uber.

U.S. Ride Hailing Market Share

Since 2017 Uber replaced its CEO and has gone on a charm offensive to win back the trust of drivers by adding a tipping feature to the app and adding 24/7 customer service which did not exist before. The company also did away with certain promotional events that effectively increased the per hour pay of drivers on the platform.

Uber’s renewed focus on fixing its public image and winning back the trust of drivers looks to have slowed the market share loss to Lyft in 2018 and a continued refocusing by Uber back on the U.S. market may start to put pressure on Lyft’s growth and ability to attract drivers without large upfront incentives.

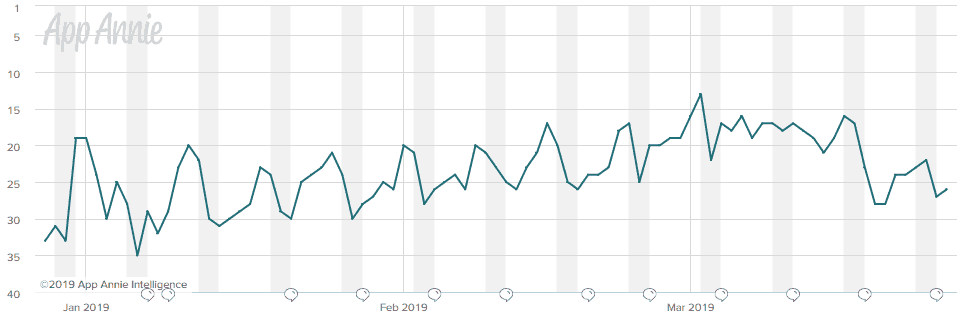

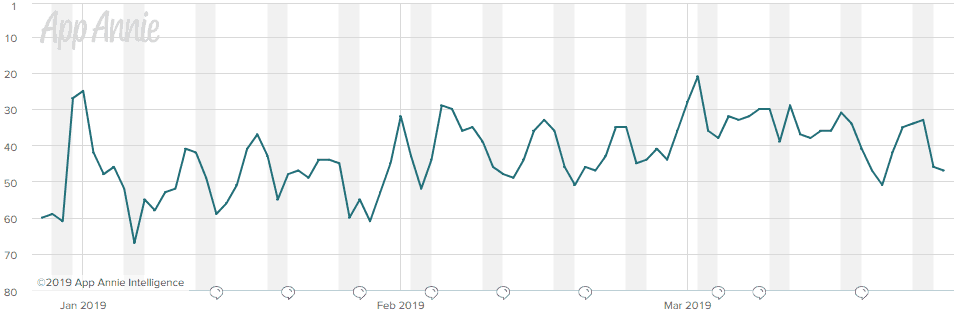

Uber remains immensely popular in America, consistently ranking as the #1 travel app download in the Apple app store and ranking in the top 20 most popular downloads nationwide. Lyft is #2 in travel but ranks as only the 50th most popular app on the platform.

Uber iOS App U.S. Popularity Last 90 Days

Lyft iOS App U.S. Popularity Last 90 Days

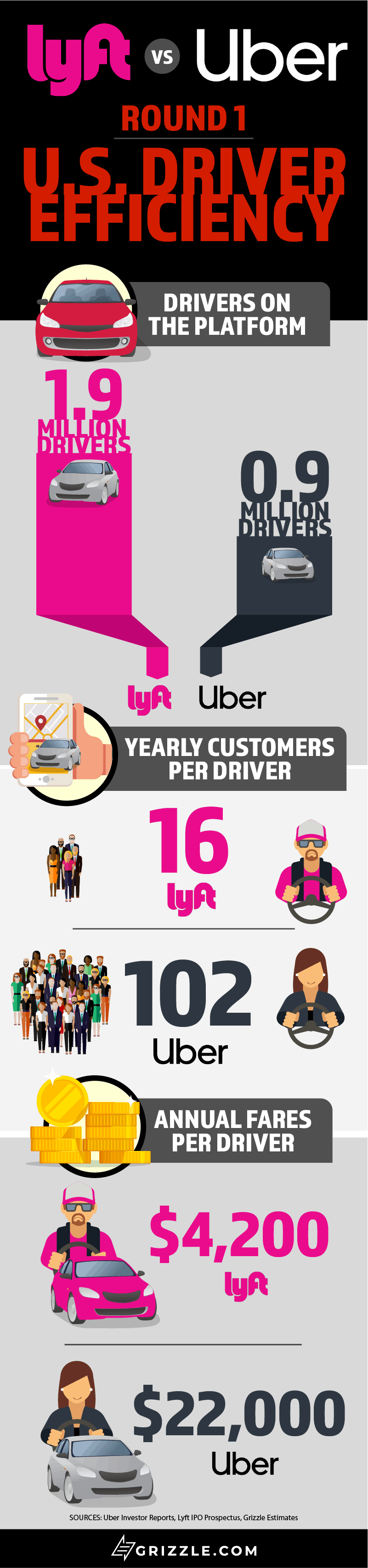

Lyft vs Uber from the Driver’s Perspective

Employees are the lifeblood of any business and Lyft and Uber are no exception. Though ride-hailing companies classify drivers as independent contractors, not employees, the drivers are the workforce that keep these companies humming. Keeping the drivers happy is integral to low driver turnover and providing customers with a pleasant ride and fast pickup times.

A recent 1,200 driver survey by TheRideShareGuy.com helps us understand if there is brand loyalty among drivers and how drivers think of Lyft vs Uber.

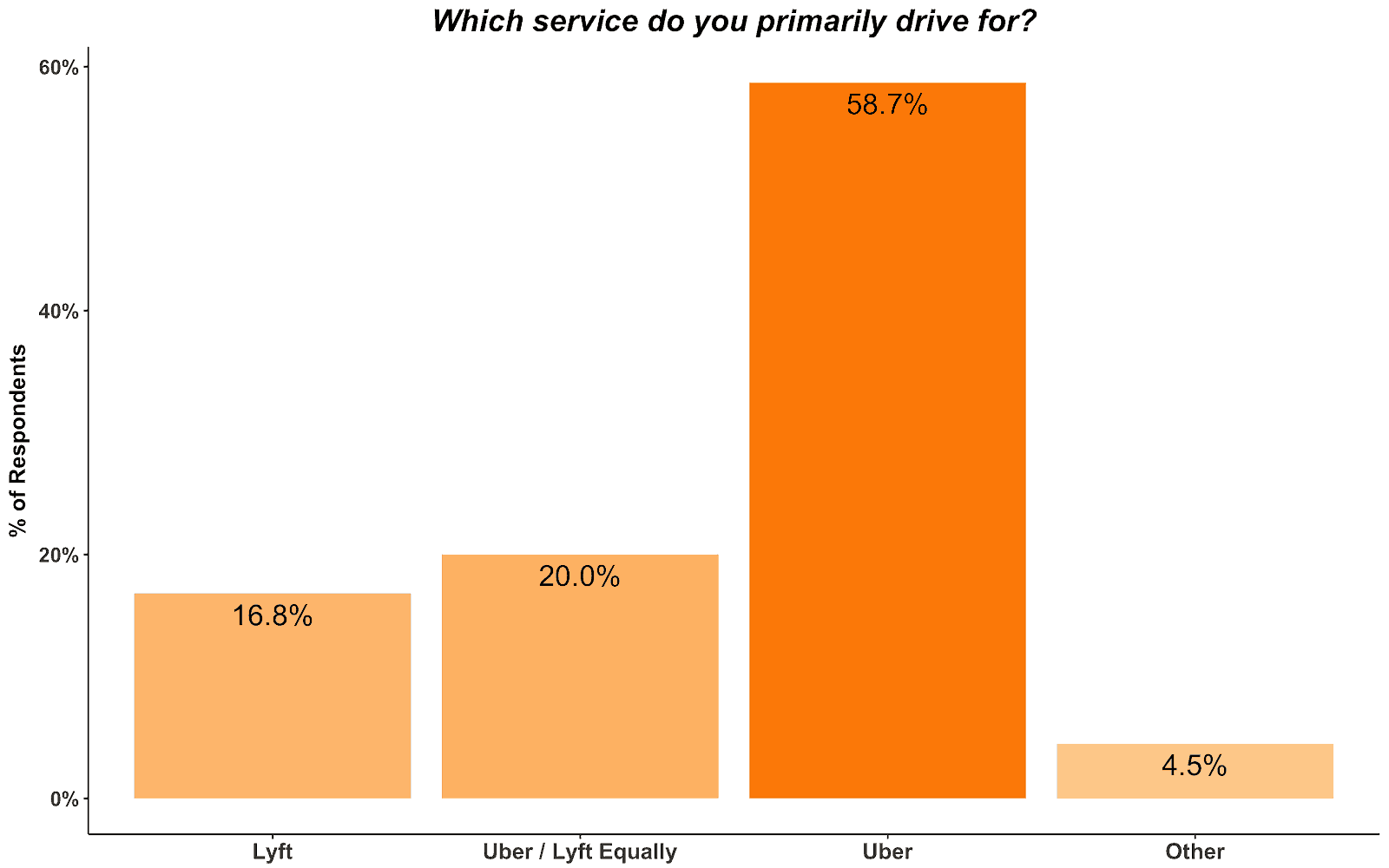

Uber is the most preferred driving service by far

60% of drivers say they mostly drive for Uber compared to only 17% for Lyft.

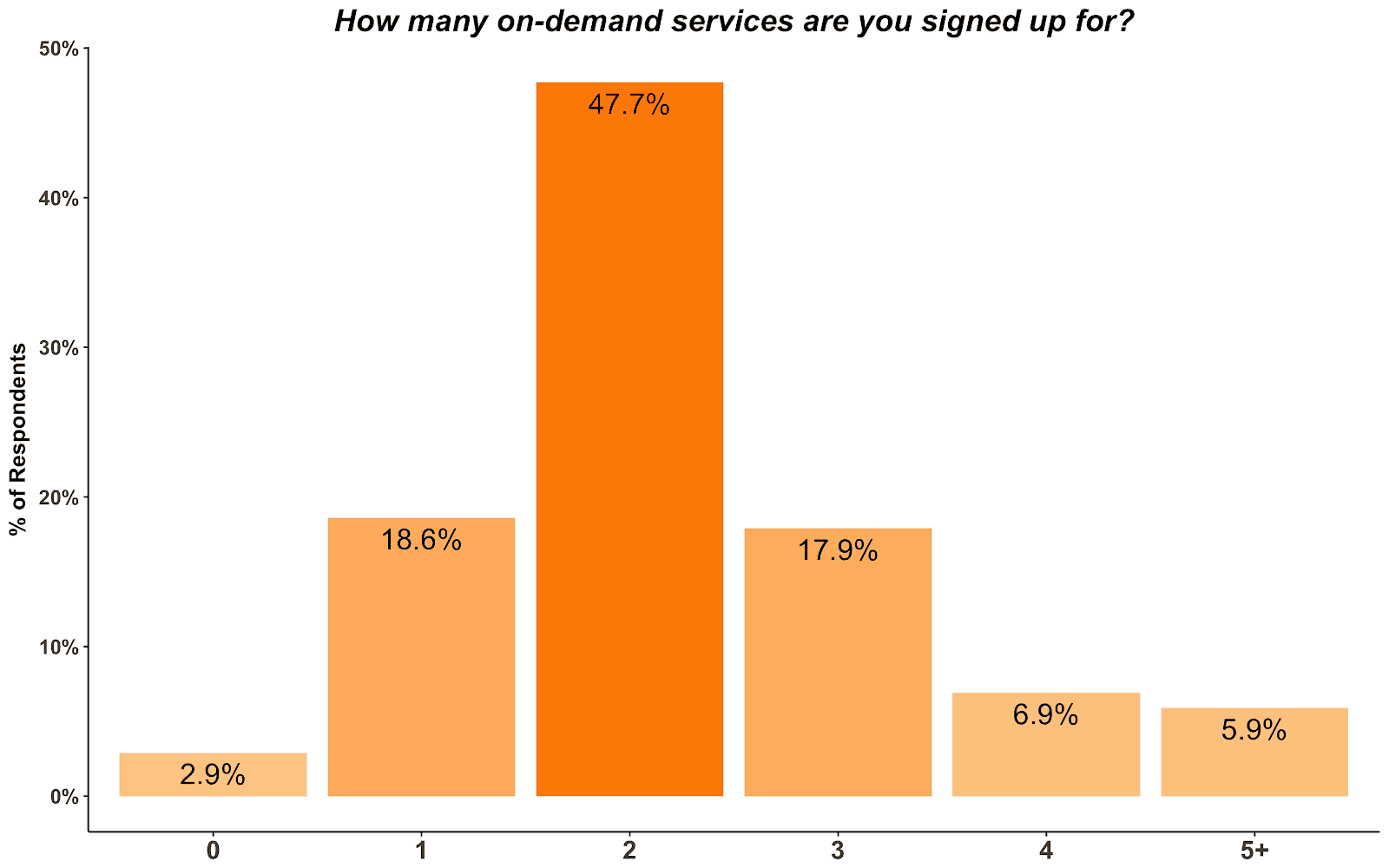

Driver loyalty is actually very low

80% of drivers have signed up for 2 or more on-demand apps including Lyft and Uber. With the proliferation of programs that scan both Uber and Lyft and choose the best fare automatically, driver loyalty is likely decreasing, not increasing.

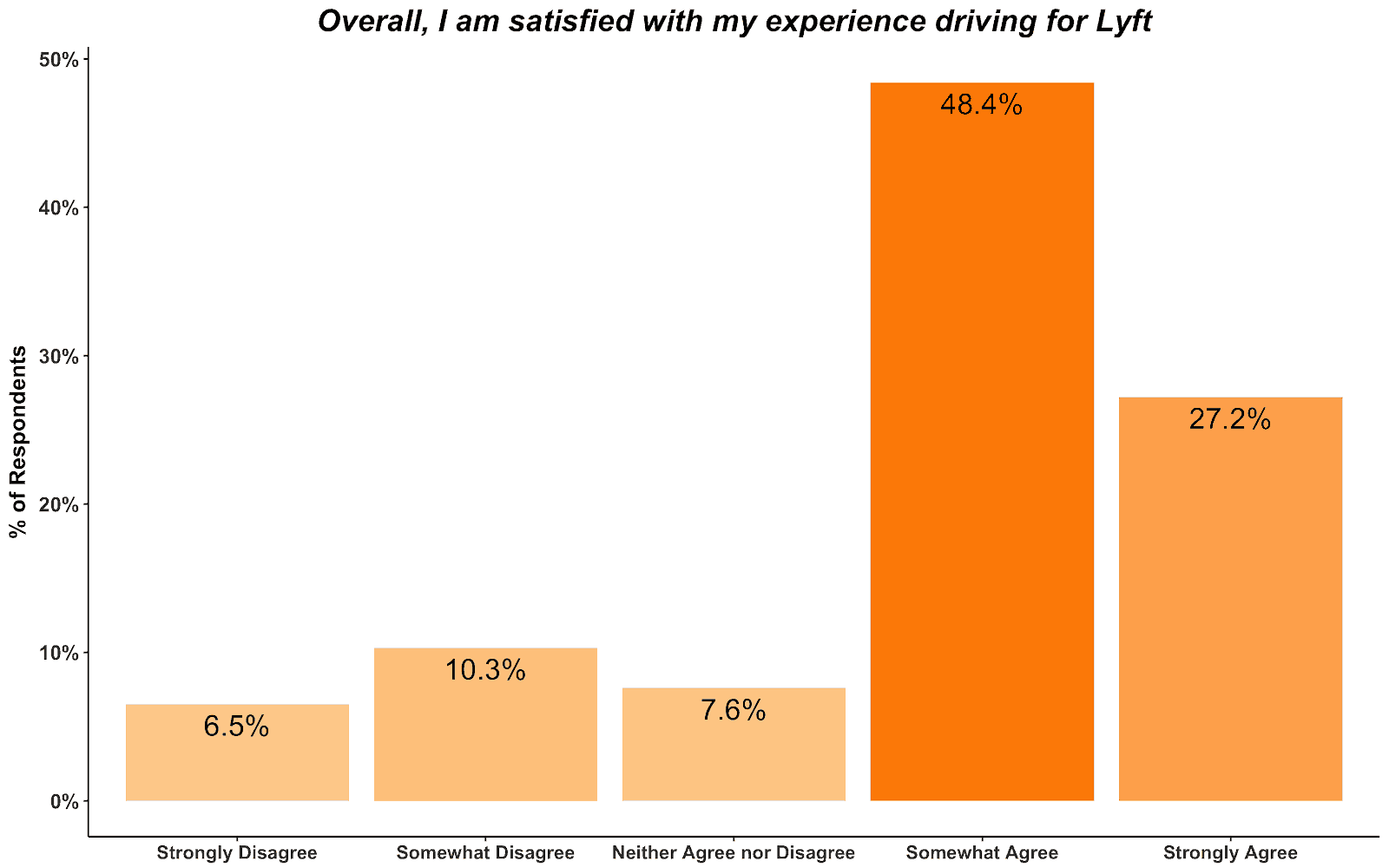

Drivers prefer Lyft for its customer service and higher customer tip rate

76% of Lyft driver’s said they are satisfied with their driving experience compared to only 58% for Uber.

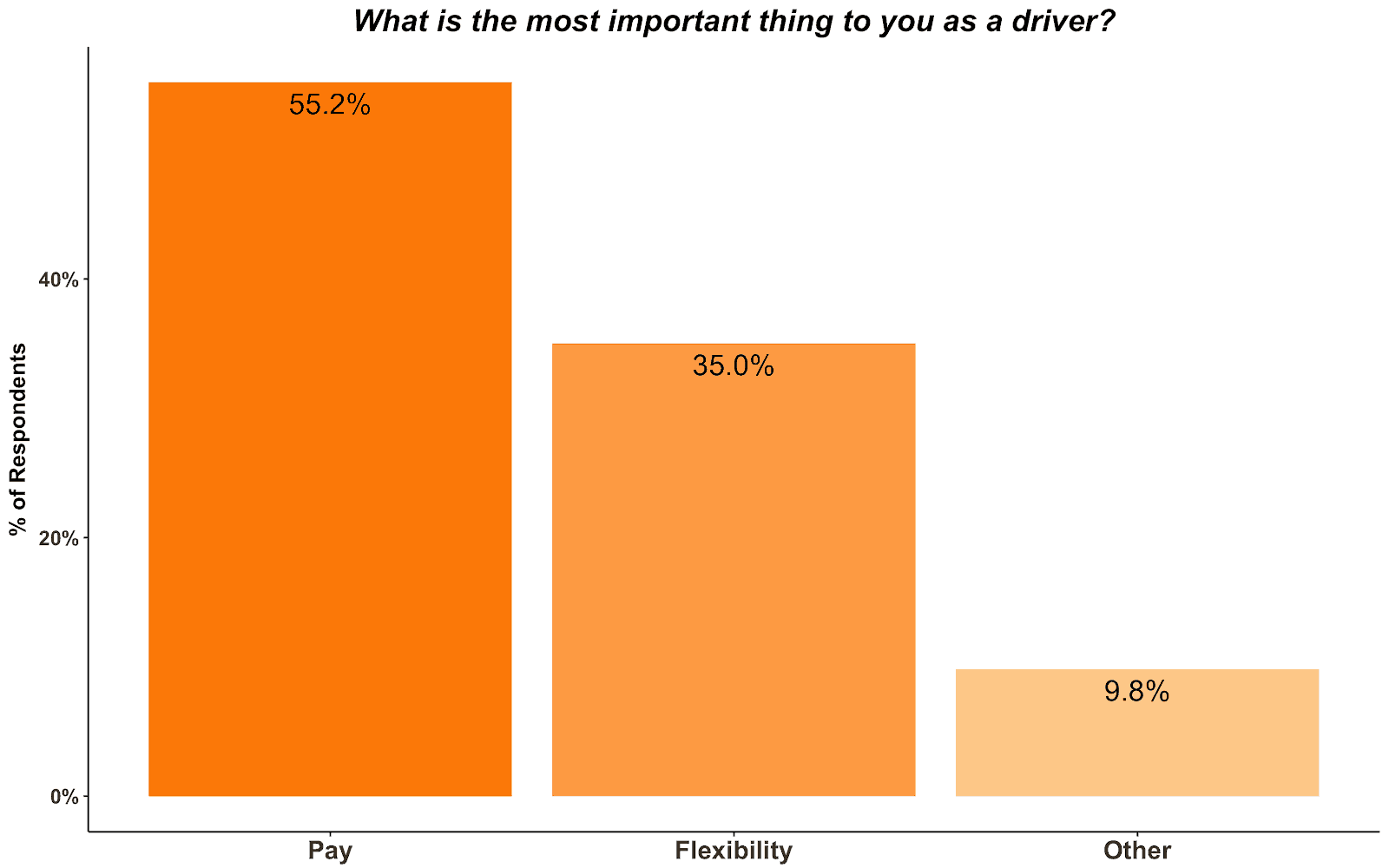

Even though Lyft is the most liked, the value of fares determines who a driver works for

55% of drivers said pay was the most important part of driving for Uber or Lyft. The second most important was flexibility, which both companies provide equally. At the end of the day a driver is going to go with whichever service offers the highest earnings opportunity as long as there is not a massive difference in customer service levels.

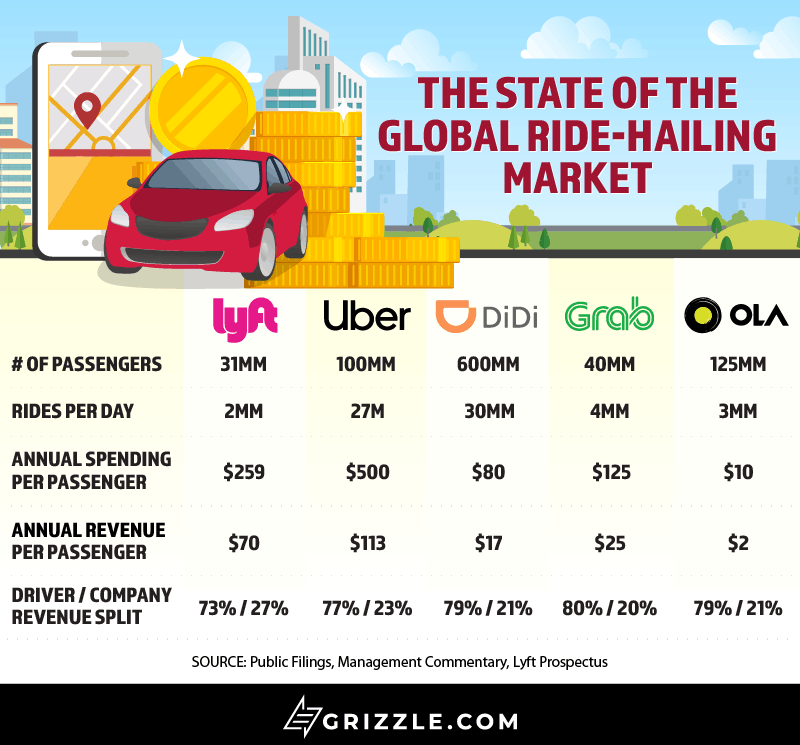

Looking at the Pricing of Comparable Companies

Lyft and Uber are not the only ride-hailing companies out there. Looking at global competitors from Asia we can see that the profitability of a passenger and the way the company is valued in its home market vary widely.

For example, Ola in India makes only $2.00 per rider annually compared to Uber which makes $113. The market has adjusted for this, valuing Uber at $720 per rider compared to Ola at only $34 per rider. Overall, U.S. ride-sharing companies were priced at 6x sales during their last fundraising round, below faster-growing Asian peers but higher than Didi in China due to lower growth expectations in the near term for that market.

| Company | Gross Billings (bn) | Revenues (bn) | Rev /Rider | P/S Per Rider |

| Lyft | $8 | $2.1 | $70 | 10.5x |

| Uber | $50 | $11.3 | $113 | 6.4x |

| Didi (China) | $48 | $10 | $17 | 5.6x |

| Grab (SE Asia) | $5 | $1 | $25 | 10.0x |

| Ola (India) | $1.2 | $0.25 | $2 | 17.2x |

| Global Weighted Average | $28 |

Source: Aswath Damodaran, Grizzle Estimates *Lyft Priced at IPO Valuation

Using comparable company “price to billings” and “price to revenues” Lyft should have priced between $15 and $23 billion ($42-$65/sh). The Lyft IPO looks like it will debut with a market cap of $23-$25 billion which is in line with the valuation of Uber at the whispered IPO size of $120 billion, but far above valuations implied by recent funding rounds of global ride-hailing companies. The Lyft IPO is going to set a new high water mark for ride share company valuations.

Expected IPO Pricing of Lyft based on Comparable Company Values

| (MM) | Price/Billing | Price/Revenues |

| Uber – Last VC Pricing | $11,598 | $13,737 |

| Uber – Rumoured IPO Price | $19,330 | $22,896 |

| Using Global Average | $17,730 | $21,428 |

| Using Global Weighted Average | $11,837 | $14,398 |

Source: Aswath Damodaran, Grizzle Estimates

Capital Structure

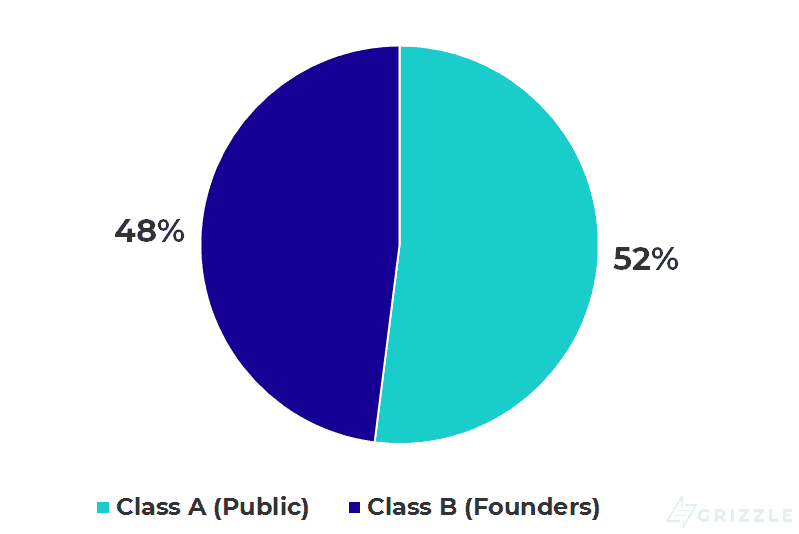

Lyft has a relatively straightforward capital structure. Class A shares are common shares with 1 vote each while Class B shares are a special class created just so the founders Logan Green and John Zimmer can retain more control over the company. Class B shares have 20 votes each and control about 48% of voting power in the company. Lyft founders and employees own a majority of the company and are firmly in voting control meaning common shareholders will have little say in company decisions. This split voting structure is becoming more and more common and unfortunately is par for the course if you want to own a piece of a high growth company in demand with investors.

Voting Power

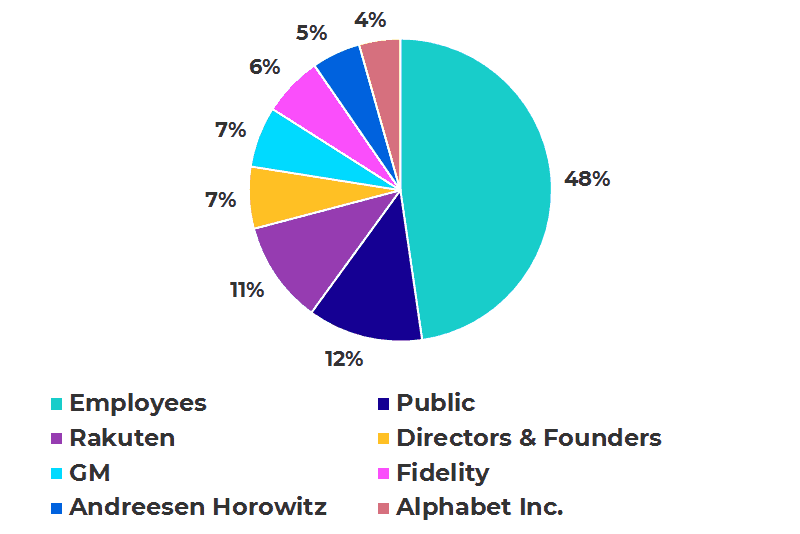

Looking at share ownership, not voting structure, the two founders and directors own 7% of the shares while employees and institutional investors with smaller stakes own another 48%. Large backers like Alphabet, GM, Rakuten, and private equity firm Andreesen Horowitz own another 33%.

Share Ownership

Lyft Lockup Period

Most of the shares owned by insiders are locked up for 180 days from the date of the prospectus filing. Insiders can start to sell their shares on the 181st day after the filing which falls on Sept. 2, 2019, however, if the date the lockup ends falls on a blackout period just prior to earnings, the lockup will end 10 trading days prior to the blackout period. Sept. 2 is not close to an earnings reporting period so we expect Sept. 2 will be the ultimate lockup expiration date.

Looking at Google, Facebook, and many other stocks, lockup expiration often puts downward pressure on share prices for a week or two. Solid companies with high growth and good fundamentals easily grow through this weakness, but for traders, lockup expiration dates are important milestones to track.

According to the prospectus for the Lyft IPO, it has 14 million options outstanding and another 46 million restricted share units (RSU) given to employees.

Calculation of Basic and Diluted Shares (mm)

| Class A Shares | 271 |

| Class B Shares | 13 |

| Over-allotment A | 5 |

| Common Shares | 289 |

| Options | 14 |

| RSU’s | 46 |

| Diluted Shares | 349 |

Source: Lyft Prospectus

Lots of Uncertainty Around How Long the Cash from the Lyft IPO Will Last

If Lyft goes public at $70/sh, in the middle of the new higher offering range, the Lyft IPO will net the company $2.4 billion after all listing fees are paid. Adding the current balance of cash and liquid investments and subtracting the taxes due of $404.8 million from the IPO, Lyft will have $4 billion to work with.

Looking at the cash burn, the company spent $280 million on operations and another $330 million on equipment and buying other companies in 2018 for a total burn of $600 million. If the burn rate continues at this pace the company would run out of money in four years (2022).

However, breaking apart working capital we see significant positive working capital changes in the last three years which offset a good portion of operating losses. In 2018, positive cash from insurance reserves and accrued liabilities offset $740 million of the $911 million net loss. We think it’s unlikely that the company will continue to see the same level of positive working capital changes year after year. Looking at operating cashflow without these positive adjustments, Lyft has enough cash for only three years of operations at the current burn rate.

As an offset to the operations burn, the company spent $250 million buying another company last year, contributing to a big cash burn from investing. If management takes a break from buying companies, the cash burn from 2018 will be at least 30% lower, giving the company an extra 10 months to operate before the cash is gone.

Years of cash is so important because Lyft is up against the clock to turn a profit before their money runs out. In the roadshow presentations, management would not commit to a timeline to turn a profit so this is the big unknown hanging over the stock.

Realistically, with interest rates low and a risk-on mood in the market, Lyft can continue to issue stock and debt to fund operations if needed. The longer losses continue the higher the risk that the company may be unable to raise money when it needs it most, sparking a fall in the stock price and a hostile takeover by a financial or strategic buyer.

So Should I Buy Shares of the Lyft IPO?

Even though we’ve spent most of our time talking about the fundamental opportunities and risks for Lyft, we are not naïve, and readily admit that overvalued stocks can go higher, and undervalued stocks can fall.

Over time, the public trading price of Lyft should approach its underlying value, which we think is lower than the IPO price, but in the short-term, the stock will trade on sentiment and supply/demand.

A reader of ours made a very smart comment about the IPO. Lyft is just the appetizer before the main course, the Uber IPO.

https://twitter.com/BullishBearz/status/1108821668691132416

Seeing as Lyft is the first ride-hailing company to go public, banks want the IPO to go smoothly to make sure investor appetite for future ride-hailing stock offerings remains strong. Bankers are also fighting to get a piece of the upcoming Uber IPO and will likely use a successful debut from Lyft as a sales pitch to participate in Uber as well.

Lyft has a one to two-month window where it will be the only ride-hailing game in town, not to mention possessing one of the fastest revenue growth rates of any publicly traded company. Judging by the small public float (11% of shares), the oversubscribed Lyft IPO and support from Wall Street, we would be buyers and think the stock should trade well directly after the IPO date on March 28.

Price to Sales Will Drive the Stock, Not Cashflow

Our positive opinion on the stock, despite all of the uncertainty around profitability, stems from understanding how the market values high growth companies like Lyft. The Lyft IPO is priced off of sales and in the current risk-on market environment, this will remain the preferred metric.

Tech Company Price to Sales Multiple Over Time

| Company | IPO Date | P/S at IPO | Current P/S | Annual Decline |

| Amazon | April 15, 1997 | 3.0x | 3.0x | 0% |

| April 18, 2012 | 20.4x | 6.1x | -10% | |

| August 19, 2004 | 8.5x | 4.4x | -3% | |

| Snap | March 2, 2017 | 34.3x | 8.7x | -36% |

Source: Sec Filings, Yahoo Finance

Historically high growth tech companies see their IPO multiple compress by 10% a year. As long as Lyft can grow revenue by faster than 10% a year the company should see a rising stock price in this market environment. We estimate Lyft will grow revenue at least 20% a year over the next 10 years, pointing to a rising stock price even if the company fails to turn a profit.

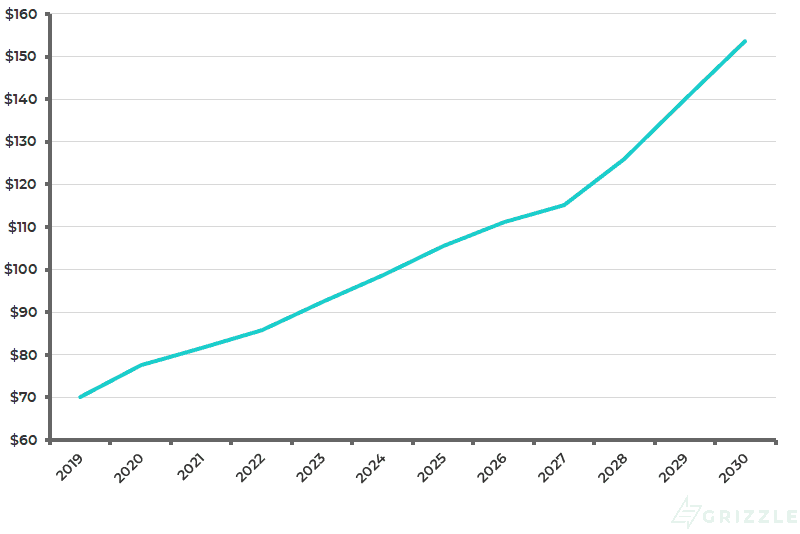

The theoretical stock price below assumes 22% revenue growth on average over the next 12 years and a multiple that falls 10% a year from 7.2x in 2019 to 3x by 2028 where it stays.

Theoretical Stock Price Forecast

Trade Lyft Don’t Own it

We would own Lyft stock only until the end of April or May. Once Uber goes public, it’s market-leading position may attract investors away from Lyft, putting pressure on the stock price. More importantly, Lyft’s insider share lockup expires Sept. 2.

Lockup expirations almost always leads to short-term pressure on a company’s share price as company employees and insiders who are sitting on large unrealized gains attempt to cash out by selling their shares on the open market. Considering the average insider has a cost basis of $23/sh and the stock will open above $60, the incentive to sell on Sept. 2 is high.

Cost Basis of Lyft Lockup Up Shares

| # of Shares Issued | Cost Basis |

| 6,063,921 | $0.23 |

| 8,129,364 | $0.76 |

| 7,067,771 | $2.10 |

| 14,479,445 | $4.25 |

| 24,674,534 | $10.13 |

| 47,099,094 | $19.45 |

| 37,263,568 | $26.79 |

| 18,662,127 | $32.15 |

| 42,771,492 | $39.75 |

| 12,964,393 | $47.35 |

| Weighted Average | $23.55 |

Source: Lyft Prospectus

Our Conclusion

Overall the Lyft IPO presents a compelling way to play the rise of the part-time “gig” economy. If the company can exploit new streams of revenue and maintain or grow its U.S. market share, the company will eventually be able to stand on its own two feet without additional cash from the market. But until that time comes, we think this stock is a trading vehicle and nothing more.

If you liked our coverage of the Lyft IPO, check out what we’re saying about Slack’s direct listing.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.