Bottom Line

Lyft (NASDAQ: LYFT) put out another strong earnings result this quarter at first glance, beating consensus on both the top and bottom line.

Revenue beat by 4%, adjusted EPS by 44% and the EBITDA loss was 40% lower than expected, all good signs.

However, investors should realize the smaller than expected losses across the board were due to a huge fall in marketing spending.

Management mentioned multiple time on the conference call that the industry is giving out fewer ride discounts, which means fares are going up and the need to advertise to bring in riders is going down.

If marketing spending had been flat with last year, the EBITDA loss would have been worse than last quarter instead of improving by 40%.

[su_panel]We think Lyft’s recent guidance for positive EBITDA by the end of 2021 depends in large part on less industry competition, a very risky bet to make.[/su_panel]With the stock only up 2% we think investors have made it clear Lyft is not out of the penalty box yet.

If you own Lyft now you need to wait 8 more quarters to see positive “adjusted” EBITDA which still means there are no earnings in sight.

A $13 billion valuation seems a little crazy for a company still losing more than $1 billion a year when EBITDA isn’t “adjusted” to remove real-life costs like stock options and insurance claims.

The market is obviously giving both Uber and Lyft credit for far more than just ride hailing or food delivery.

With less than 30% revenue growth expected next year and profitability nowhere in sight, we think Lyft will continue to struggle to find a direction.

We would frankly rather own Tesla looking at both multiples, profitability and growth.

Consensus Estimates for 2020

| (2020 Estimates) | Price/Sales | Revenue Growth | EBITDA Margin |

| Uber | 3.1x | 32% | -15% |

| Lyft | 3.0x | 25% | -15% |

| Tesla | 1.9x | 21% | 13% |

| Ford | 0.24x | -1% | 7% |

| Honda | 0.34x | 2% | 8% |

We still don’t like Uber or Lyft based on their long runway to profitability, which makes any long-term forecast a butt of a joke.

If you absolutely must have exposure to the ride-hailing revolution, we recommend owning Uber and going short Lyft due to Uber’s superior unit economics.

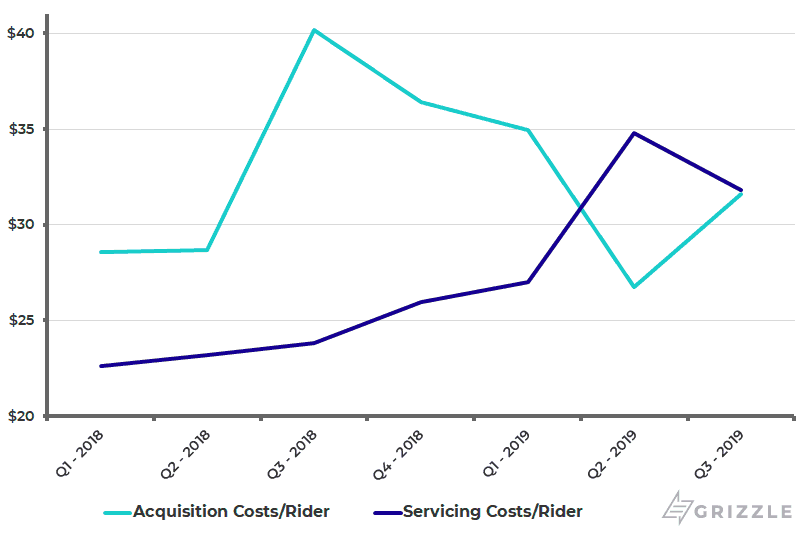

Per rider metrics continue to concern us at Lyft with both user acquisition costs and the costs to service current riders still going up even as the company added 8 million riders.

Our overall take on ride hailing stocks is why bother.

We recommend investors either go short a dud like Peloton (NASDAQ: PTON), or own fast-growing tech stocks with a better road to profitability like MongoDB (NASDAQ: MDB) or Slack (NYSE: WORK)

Per Rider Costs are Still Going Up at Lyft

A Review of Earnings

Lyft’s third-quarter non-GAAP loss per share was $0.41, 32 cents ahead of analyst estimates. The loss per share on a GAAP basis was nine cents ahead of estimates at $1.57. Revenue of $955.6 million was comfortably ahead of estimates and 63% higher than a year ago. Analysts surveyed by FactSet expected revenue to reach $915 million for the quarter.

The number of active riders increased 28% from a year ago to 22 million. Revenue per active rider increased 27% to $42.82 for the quarter.

The net loss, which was estimated at $478 million, came in at $463 million, widening from $249 million a year ago. However, the adjusted net loss for the quarter of $121 million improved significantly from the $245 million loss a year ago. The difference can be attributed to stock-based compensation, amortization of intangible assets, and related charges.

Outlook Raised for the Full Year

Lyft’s management team expects revenue of $975 to $985 million in the fourth quarter, with an adjusted loss of $160 to $170 million. The revenue outlook for the full year was raised from a midpoint of $3.48 billion to between $3.57 and $3.58 billion. This will represent annual growth of 66%.

CEO and co-founder Logan Green said the company expects to be profitable on an adjusted EBITDA basis in the fourth quarter of 2021.

Sequential Improvement in Costs and Operating Expenses

Year-on-year costs and expenses widened throughout the income statement. The cost of revenue increased from 55% to 61% of total revenue, and operating expenses increased from 62% to 90% of revenue.

While annual expenses widened, sequential costs and expenses fell as a percentage of revenue. The cost of revenue fell from 72% to 62% of revenue, and operating expenses fell across the board. This resulted in the operating loss falling from $672 million in the second quarter to $490 million.

If there is a concerning element to the results it may be the ballooning of stock-based compensation and related expenses. This accounts for the large discrepancy between the GAAP and non-GAAP loss per share.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.