The Liquidity Punch Bowl

It is appropriate with the inauguration of this weekly column to look at the ‘Big Picture’. The biggest risk to world stock markets, and asset prices in general, in 2018 is that G7 central banks (led by the Federal Reserve) are finally attempting to normalize monetary policy nine years after the American central bank commenced quantitative easing in December 2008, in the midst of the so-called “global financial crisis”.

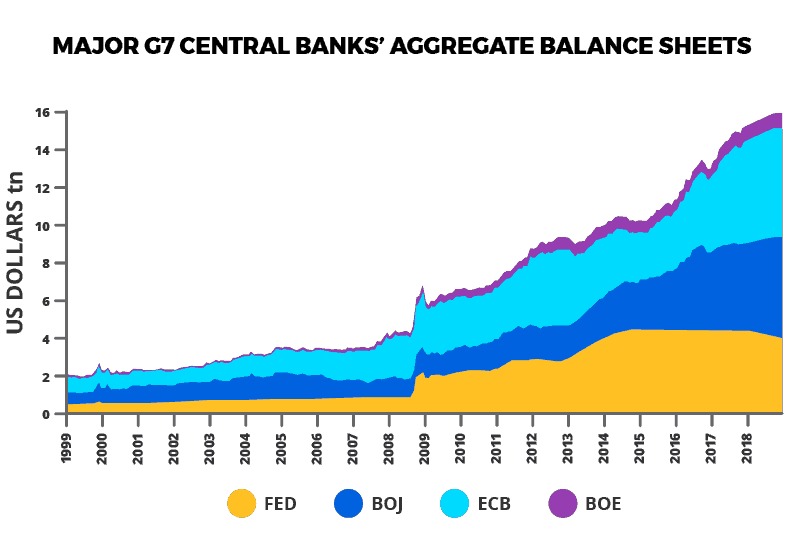

Since late 2008, G7 central banks, comprising the Fed, the Bank of Japan, the European Central Bank and the Bank of England, have committed to massive balance sheet expansion (through the purchase of mortgage and government debt). Their balance sheets continued to rise in aggregate during 2017 even though the Fed itself stopped expanding its own balance sheet in November 2014. Aggregate assets of G7 central banks increased by 17.2% last year to $15.2tn at the end of 2017, up from US$4.3tn at the beginning of 2008 (see following chart).

That the Fed has commenced balance sheet reduction from last October is a risk for stock markets since it amounts to another form of monetary tightening, in addition to interest rate hikes. That it has not yet caused market fallout reflects two factors:

- The Fed is beginning extremely tentatively by decreasing its reinvestment of principal payments from maturing bonds.

- Other G7 central banks are still expanding in aggregate, albeit at a slower pace. This is why there will be much focus on what the European Central Bank will do in coming months. For now, it looks like G7 central bank balance sheets will start to contract in aggregate in 2019 rather than 2018.

Uncharted Territory of Balance Sheet Expansion

How difficult will it be for central banks to normalize monetary policy in practice, and what will be the consequences of such policies for investors assuming that the central banks’ commitment to balance sheet reduction is maintained? This is uncharted territory.

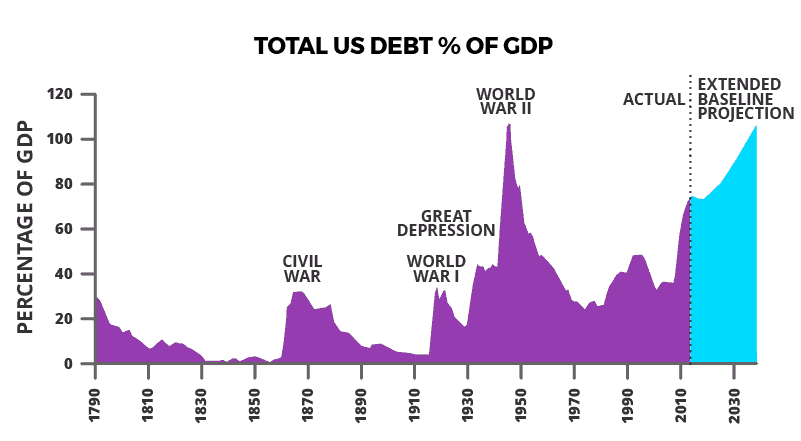

The only precedent for the scale of the central bank balance sheet expansion of the past nearly 10 years was during World War II, with government debt and government guaranteed assets now accounting for at least as large a share of central bank balance sheets as during World War II. Clearly, the purpose of such central bank balance sheet expansion in the 1940s was to assist the fiscal authorities in financing a war.

Quantitative Easing Bailed Out the Rich

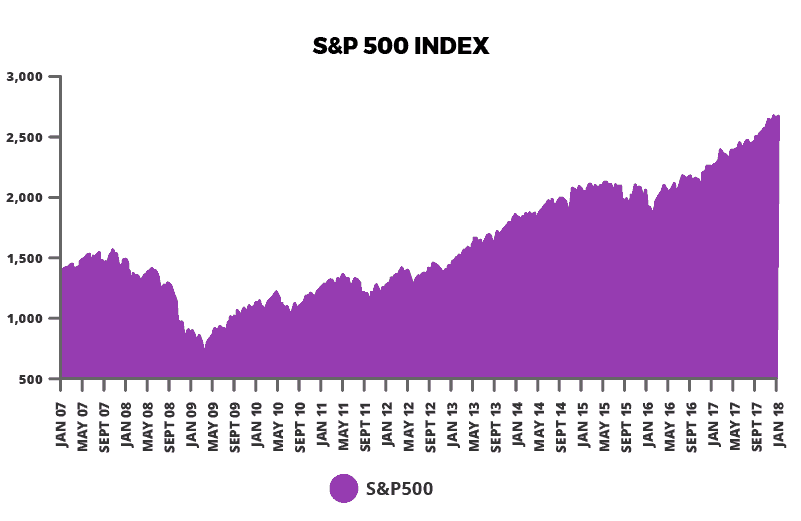

The ostensible purpose of balance sheet expansion since 2008 has been to stabilize “aggregate demand” in the neo-Keynesian sense of that term (lower borrowing costs and bid up asset prices in the hope of stimulating broad based economic activity). The real aim, so far as this writer is concerned, has been to stop debt liquidation and thereby prevent the creditor classes, be they bankers or bond owners, from losing money. This is the reason for the rising inequality which has been getting so much attention of late. The wealthy were bailed out while, as owners of shares and real estate, they also benefited from the rise in asset prices since 2009 triggered by quantitative easing (see following chart).

Global Economic Headwinds: Debt & Demographics

The other point is that central bank balance sheet reduction after World War II was achieved primarily by central bank balance sheets declining relative to GDP without central banks actually having to shrink their assets in nominal terms.

This balance sheet reduction was only made possible by the strong economic growth recorded after World War II. For the record, US real GDP rose by an annualized 4.4% between 1949 and 1969, while Japan’s real GDP increased by an annualized 9.7% between 1955 and 1970.

The situation is completely different today where aggregate debt levels in the developed world are much higher and where ageing demographics in the developed world are much less conducive to robust growth. Real GDP growth has averaged only 2.2% in America since 2009, 1.3% in the Eurozone and 1.7% in Japan since 2009.

Central Bank Credibility at Risk

The other issue raised by the years of quantitative easing is the inevitable blurring of central bank independence, in relation to the fiscal authorities, when the central bank is so active buying government bonds. The Bank of Japan, for example, now owns 42% of the Japanese government bond market.

This raises the critical issue of central bank credibility. For the risk raised by the Fed’s attempt to normalize is that a stock market downturn may force it to reverse course; and with such a reversal there is a much greater risk of a resulting loss of central bank credibility. This is because markets may conclude that central banks will never be able to exit so-called unorthodox monetary policy.

Velocity of Money Remains Low (For Now)

In such circumstances it is possible that there is an inflection point in the turnover of money, or what economists call ‘velocity’ (the rate at which money is spent), most particularly if the value of government-guaranteed debt is ever called into question. Gold is the only practical way of hedging such a development.

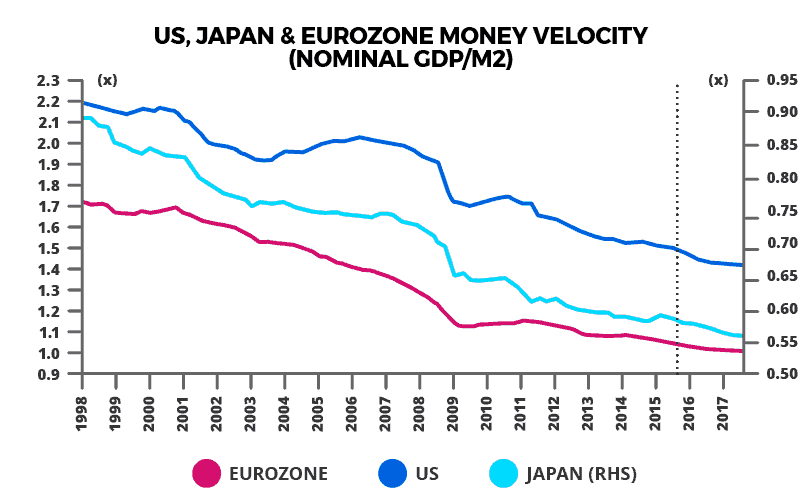

Meanwhile it is interesting to note that velocity has continued to decline since 2009 despite the frenzied G7 central bank money printing (see following chart). Indeed it is at a record low.

Like a rubber band. When it snaps, the inflection point may be dramatic.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.