Macy’s (NYSE: M) has posted results for Q4 2020.

Revenue came in at $8.33B which was roughly in line with analysts’ estimates of $8.317B

EPS came in at $2.12 which beat analyst’ estimates of $1.96

The stock has been hammered in the markets for the past 5 years as it has been the case with most retail giants. The so-called “retail-pocalypse” has hit Macy’s hard. Consumers are continuously flooding to eCommerce platforms like Amazon for their daily shopping. Although other retail chains like Walmart has been pushing hard into the online space, Macy’s in contrast seems to have fallen asleep at the wheel and is now playing catch-up. The stock has suffered as a result, now trading around $15/share compared to above $24/share at this time last year.

Getting Hit From All Sides

Macy’s is one of the oldest companies in America still in operation. Macy’s was founded all the way back in 1858 by Rowland Hussey Macy and in 2015, Macy’s was the largest U.S. department store company by retail sales.

But in more recent times, Macy’s has encountered quite a bit of headwinds and the company’s long-term future seems very in question, as Macy’s seems to announce store closures every few months. On January 8, 2020, Macy’s announced that it would close 29 underperforming stores (one Bloomingdale’s location in Miami and 28 Macy’s locations).

Wall Street expectations for Macy’s is exceptionally low. Comparing forward P/E ratios of Macy’s versus other retail brands, we see that Macy’s trades at a heavy discount compared to just about every other retail chain (many of whom are significantly smaller compared to Macy’s in terms of market cap and scale).

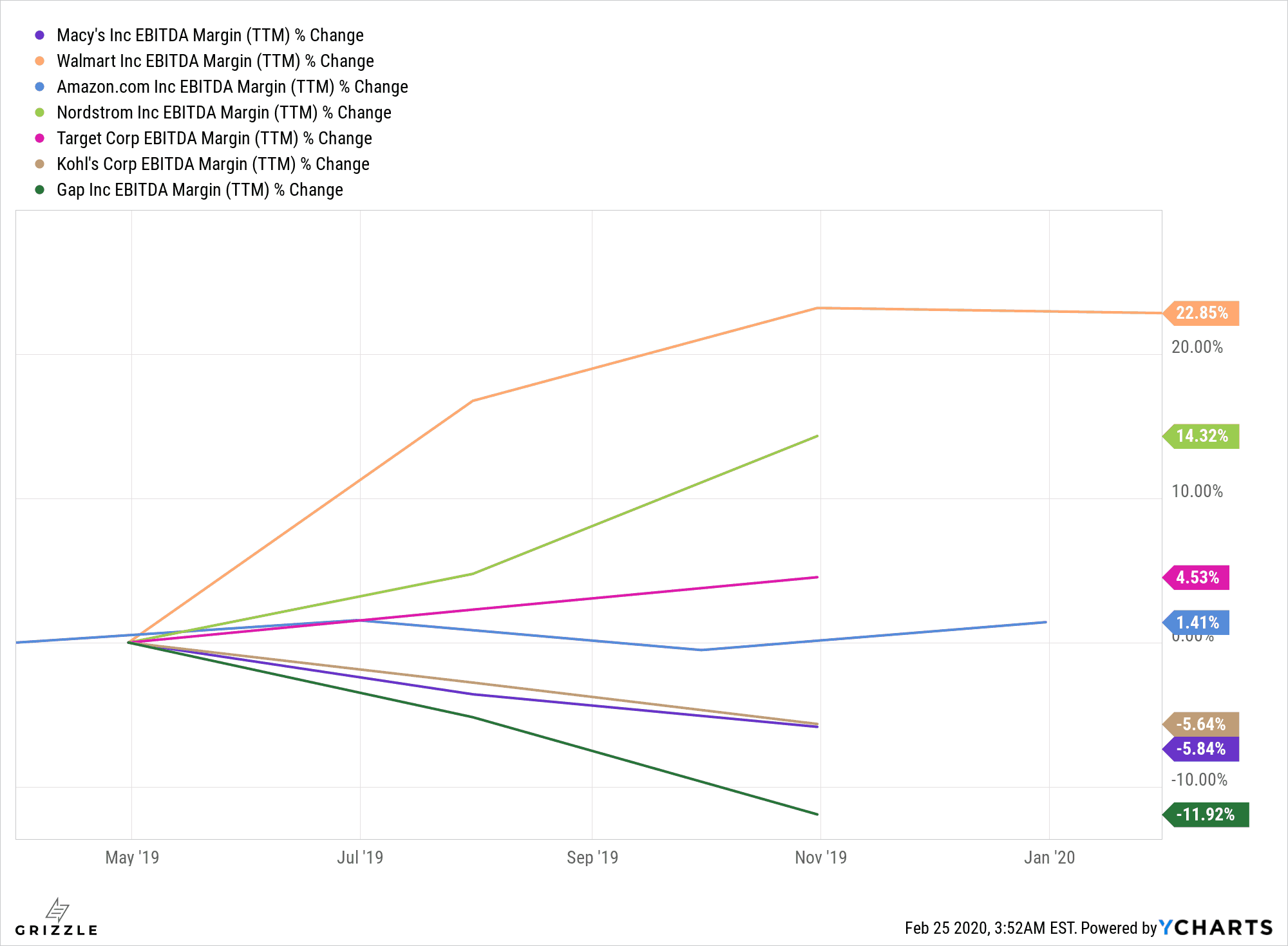

Although some may argue that Macy’s looks undervalued due to its exceptionally low P/E, taking a look at the EBITDA Margin on Macy’s reveals that the company’s margins have declined quite significantly over the past year which is concerning.

Compared to Walmart’s impressive EBITDA Margin growth, it is no wonder why Walmart deserves to trade at a much higher valuation than Macy’s.

As if all this news is not already bad enough, recently, Standard and Poor has cut the credit rating of Macy’s to “junk”. The sentiment among both Wall Street and consumers seem to say that Macy’s is old news and is on its way down into the dustbin history if management cannot not turn the ship around soon.

It is also not helping that China’s production capacity is temporarily vastly reduced due to the coronavirus outbreak which have sent investors selling retail stocks in droves as supplies for products become increasingly constrained. Despite its low valuation Macy’s is a solid pass for now. Until there is some evidence that the company can be turned around, it will likely remain dead money.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.