Magna International (TSE:MG, NYSE:MGA) has posted their results for Q4 2019.

Revenue was $9.40B which beat analysts’ estimates of $9.11B.

EPS was $1.41 which beat analysts’ estimates of $1.32

The stock has been relatively flat compared to the price at around the same time last year, though it has had a fair number of dips and spikes. Magna manufactures car components for many big name brand car companies such as General Motors and Ford. Due to the cyclical nature of the business, the stock price seems to be rather cyclical too. It will be interesting to see how the stock plays out in the future since the automotive industry has been in decline lately with GM and Ford posting negative revenue growth or expected revenue growth.

If You Want To Know How Car Companies Are Doing But They Won’t Tell You, Just Ask Magna

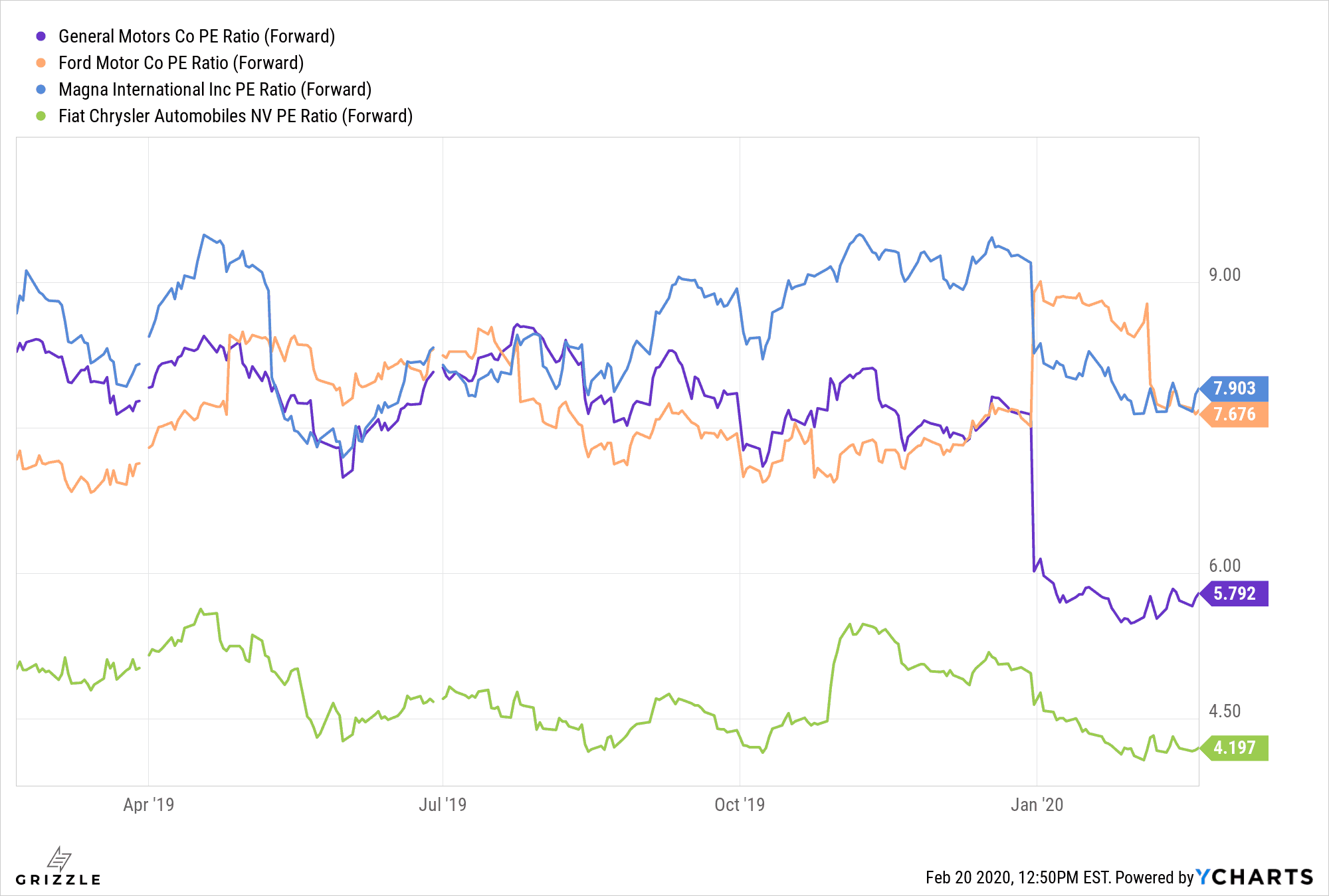

Taking a look at the valuation of Magna compared to car companies, we see that Magna is trading at a slightly higher forward P/E than its big name automotive manufacturing clients.

Although this is not saying much since it is still very low, coming in at a forward P/E of just under 8. This means that, in general, Wall Street has very low expectations for Magna as well as the Big Three U.S. automakers, signaling that they believe Magna’s business is expected to decline over the years.

The revenue growth trend is also somewhat concerning. On a year-over-year basis, Magna’s revenues have declined 0.5% while according to SeekingAlpha, the sector as a whole has increased revenues on average of 4.53%.

Is Magna Ready For The EV Revolution?

With that being said, Magna may be a much better bet on the automotive industry than the traditional automakers like GM or Ford. This is because Magna has been rapidly adapting to making components for EVs and boasts Tesla as one of its main customers. Besides, not every component of an EV is different than a traditional fossil fuel vehicle, so there are indeed economies of scope that Magna can exploit if everyone switches to EVs.

In 2015, a division of Magna called Magna Steyr based in Austria sold its battery pack business to Samsung for $120 million. Clearly, other companies see the potential for Magna to make a meaningful impact in the trend that is the electrification of vehicles.

There’s still reason to be bullish on Magna, even despite the low valuation (or because of the low valuation, depending on how you view it), the company has beat earnings estimates for 2 out of the 3 last quarters. If you are willing to take the risk of investing in a business that’s trading at a low valuation due to declining revenues, and you believe a turnaround might be coming in soon, then perhaps Magna is worth a second look.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.