Wall Street-correlated world stock markets remain remarkably well bid given the appalling macroeconomic data being announced. There remain two main explanations, aside from the over-the-top Federal Reserve policy response:

- The first is that the spread of the virus has not been as bad as feared in the middle of March, with hospital systems in the likes of America able to cope better than expected.

- Second, there remains growing focus on re-opening the economy, most particularly in America.

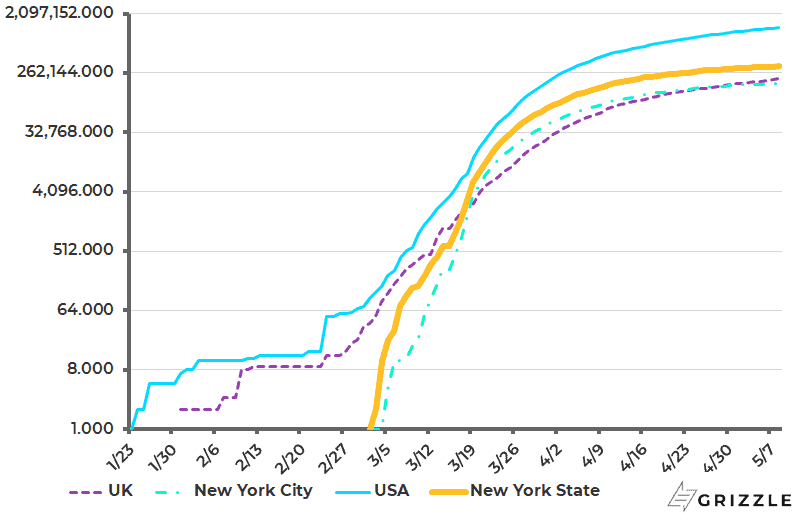

Europe is Now Post Peak COVID-19, British & American Curves Flattening

In relation to the health data, it is now reasonably clear that Western Europe peaked around the middle of April as anticipated.

The process of cautious re-opening has now begun in countries like Germany and Switzerland. Britain is behind the curve because it panicked and went from a strategy of crowd immunity to total lockdown thereby losing precious time.

Still even in Britain and America the curves on the log charts are flattening (see following chart).

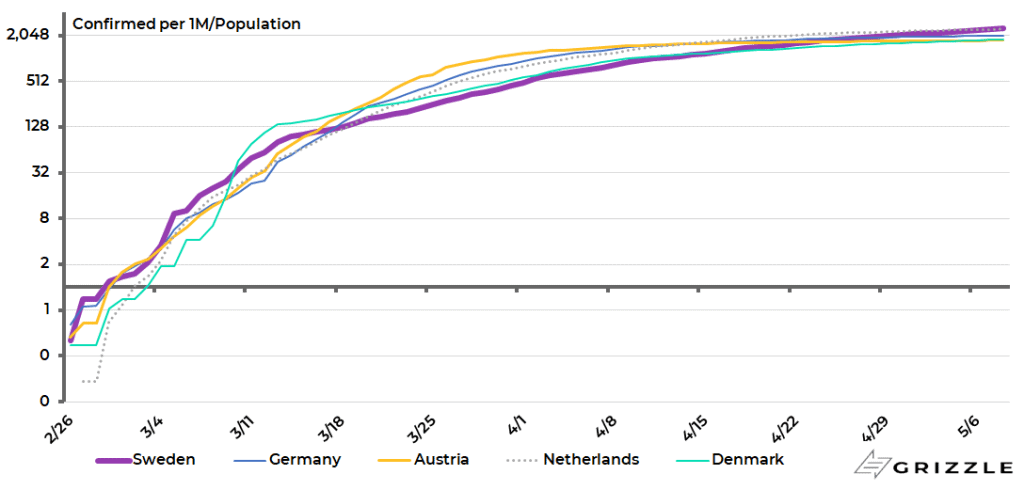

Meanwhile it is also interesting that the chart in Sweden, which has gone for crowd immunity, does not look so different from many other European countries.

There are now 25,265 confirmed cases in Sweden, or 2517 cases per 1m of population, compared with 1805, 1761 and 2043 cases per 1m of population in Denmark, Austria and Germany respectively (see following chart). Sweden’s Public Health Agency expects Stockholm to reach “herd immunity” in May (see USA Today article: “Swedish official Anders Tegnell says ‘herd immunity’ in Sweden might be a few weeks away”, 28 April 2020).

Stock Market Tuned into Re-Opening the Economy Not Body Counts

If this is the picture, the stock market is now more focused on news on re-opening than on the virus-related data, be it cases or deaths. This month will see a staggered process to start opening up the American economy. Because of America’s federal constitution this is going to go state by state, a process which will be further distorted by the politicisation of Covid-19 which is why Republican governed states will be leading the return to work.

Still it will make sense to try a gradual reopening. Aside from the obvious health risks of triggering a renewed surge in infections by a too rapid withdrawal from “social distancing”, the 45th American president’s political interests are best served by having the American economy perceived to be returning to normal by the third quarter.

This will be viewed as a big “win” politically in the current context of absurdly alarmist GDP forecasts being made by the likes of the IMF and hysterical talk of international travel shutting down for the next year and more.

For this reason the months of May and June should be viewed as a transitional process. But the more that things are opening up, without evidence of a renewed surge in infections, the more stock markets will like it.

In this context, the market’s attention will then turn to whether aggressive monetary and fiscal policies will be withdrawn. Most likely, the policies will be withdrawn much more slowly than they are introduced. That is if they are withdrawn at all.

For now the central bankers are still competing to announce more “easing” and being duly cheered on, as usual, by the financial chattering classes.

The Bank of Japan Governor Haruhiko Kuroda, in a desperate effort to be seen to be doing something, recently announced stepped up buying of corporate bonds and commercial paper in an announcement which was only of interest because of the almost complete lack of market impact it generated. The BOJ raised its cap on holdings of corporate bonds and commercial paper from ¥7.4tn to ¥20tn until the end of September.

More interestingly, the ECB has now effectively expanded its purchases of corporate bonds to the high-yield area, as the Fed has already done. To be precise, the ECB loosened in late April its collateral rules temporarily until September 2021 to accept so called “fallen angel” bonds which have been downgraded to junk status due to the health crisis.

As for the Fed, it has kept its forward guidance unchanged, saying at its latest meeting in late April: “The Committee expects to maintain this target range (0-0.25%) until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals.”

This means that the Powell Fed has, so far at least, not done a Ben Bernanke and committed not to raising rates for two years. Remember this is what former chairman Bernanke did in August 2011. But a repeat of such a ‘forward guidance’ policy remains quite possible, if not probable.

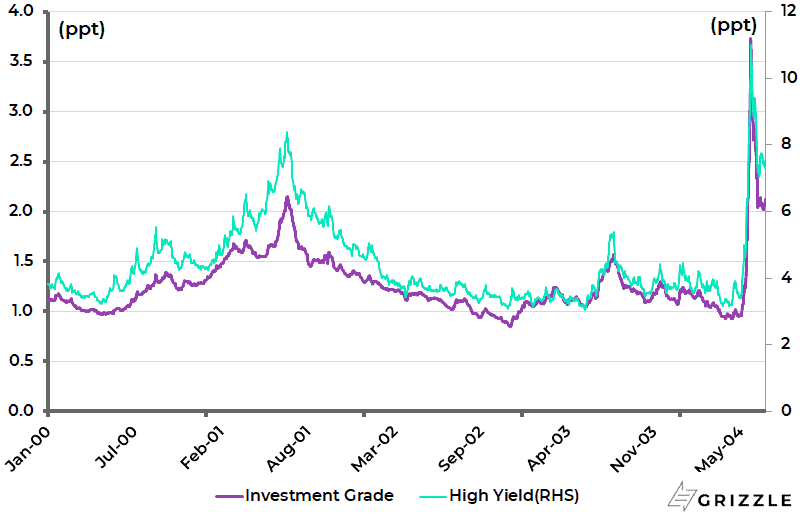

Still the Fed has already played its main role in this crisis by its aggressive signal on corporate bond purchases which reversed the alarming rise in credit spreads in March. US investment-grade and high yield corporate bond spreads peaked at 373bp and 1,100bp respectively on 23 March and have since declined to 212bp and 725bp (see following chart). This has provided a significant opportunity for investment grade corporates to issue bonds.

The next big move by the Fed will likely come when it imposes its version of the Bank of Japan’s yield curve control when Treasury bond yields will be fixed up the yield curve, as previously discussed here (see Stocks & gold assets to own, real bear market is in government bonds, 27 April 2020).

The timing of that potentially historic development is unclear. But it may happen, if not before, when the American economy is seen to be rebounding out of the health crisis, at which point there will be much talk from the chattering classes about a V-shaped recovery.

Such an introduction of formal price controls in the Treasury bond market will mark the formal introduction of a regime of so-called ‘financial repression’. Gold and bitcoin will be the obvious beneficiaries.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.