The rug has officially been pulled out from underneath one of the largest bubbles in global equities: Canadian pot stocks.

Retail Investors Gone Wild

Euphoric retail punters stratospherically bid up the sector over the last year, liberally opening their wallets to questionable management teams at even more questionable valuations. Investors had hoped that 2018 would be a ‘victory lap’ with the legalization of the Canadian recreational marijuana market set for the summer — it has been anything but.

The Global Cannabis Index is off -44% from the peak in January (see chart below). The market fully capitulated today with the three largest producers down significantly: Canopy Growth ($4 billion market cap) – 12.0%; Aurora Cannabis ($3 billion market cap) – 8.5%; and Aphria ($3 billion market cap) – 9.9%.

Global Cannabis Stock Index

Fundamentals for Marijuana Stocks are as Sketchy as the Management Teams

In early February, Grizzle highlighted the risks in our deep dive report, Up in Smoke: The Overvalued Haze of Marijuana Stocks. We confronted the three inconvenient truths about the sector:

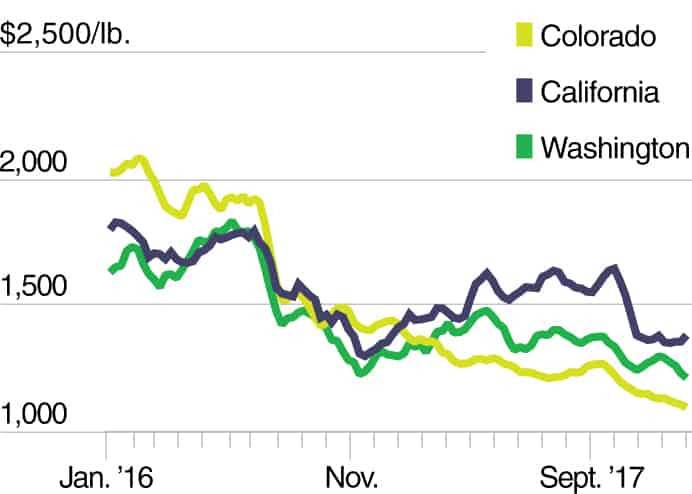

1. Legalization of marijuana always equals price deflation – In every legal market, retail and wholesale prices peak near the date of legalization due to lack of supply and then quickly begin to fall, driven down by new entrants.

Spot Legal Prices

2. The black market is the biggest competitor for licensed producers – The marijuana market is mature in Canada with the black-market supply already exceeding demand (Canada exported 20% of marijuana production in 2017). Legal supply will have to compete on a price basis for market share — the black market won’t magically disappear.

3. Extreme valuations are reminiscent of the 2010 rare earth bubble. The bulls want to believe marijuana is a manufactured and branded product. It’s not. Marijuana is a commodity and always will be (see Colorado, Washington, and California).

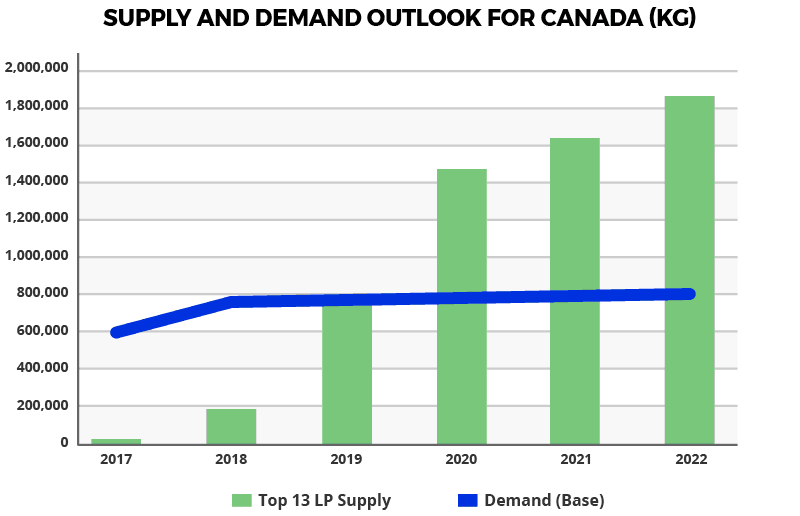

Market will be Flooded with Planned Legal Capacity – 2X of Demand

Grizzle compiled the planned capacity of the top 13 legal producers in Canada. Based on estimated consumption rates, Canada will be at least 850,000 kg (85%) over supplied by the end of 2021. Importantly this oversupply doesn’t account for smaller producers or the black market, which is already fully supplying the market.

With no valuation support, marginal management teams, and a skittish retail investor base — the outlook for marijuana equities is bleak. A long summer awaits.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.