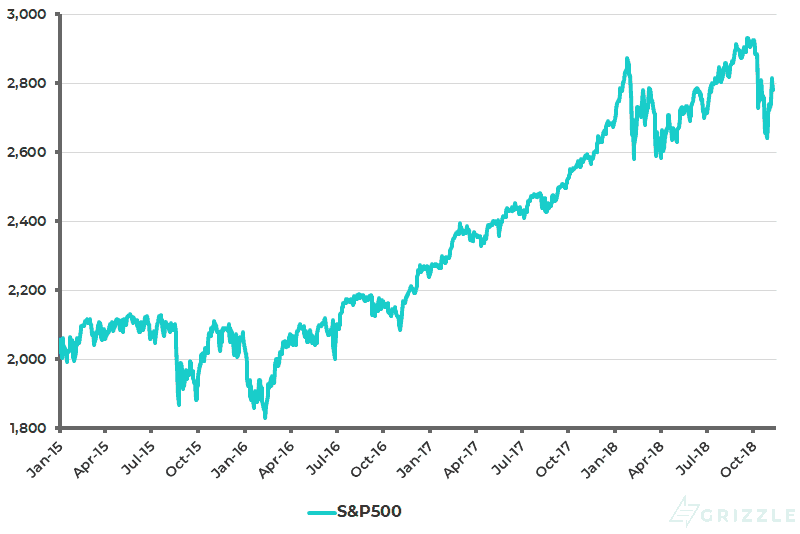

There is clearly the potential for more of a technical rally in stock markets with the bogey month of October having now concluded. The S&P500 has risen by 6.8% from its low reached on Oct. 29, after declining by 11.4% since Oct. 3 (see following chart). Also, stock markets normally rally into year end.

S&P500

China Trade Deal and Share Buybacks Point to an Extended Stock Market Rebound

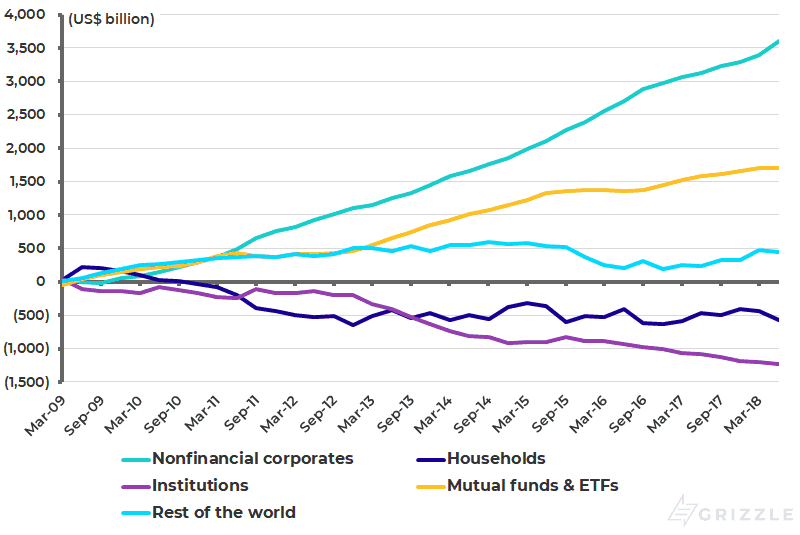

Perhaps the best argument for an extended rebound on Wall Street, aside from a deal on trade between China and America, remains a resumption of share buybacks after earnings season. This is a reminder that companies remain the major buyer of shares in America this year, as they have been since 2009 (see following chart).

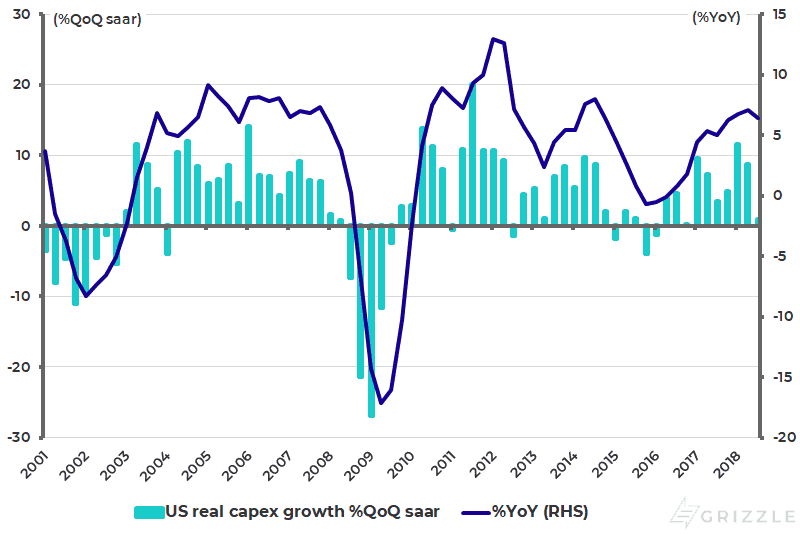

The latest US GDP data was also a reminder of this pattern. While the headline data was positive at an annualized 3.5%QoQ and 3.0%YoY growth, though the number was swollen by inventories, the most interesting detail was negative. That was the renewed weakness of business investment. Real private non-residential fixed investment rose by only 0.8% QoQ SAAR in 3Q18 and was up 6.4% YoY, down from 8.7% QoQ SAAR and 7.1% YoY in 2Q18 (see following chart). This supports those who have been arguing that the major consequence of the corporate tax cut and related corporate repatriation of offshore dollars will be to boost share buybacks rather than capex.

Cumulative net purchases of US corporate equities

US real private non-residential fixed investment growth

The Mid-term Election’s Impact on the Markets

Meanwhile, the mid-term elections have come out more or less as expected. But despite the House of Representatives narrowly being captured by the Democrats this is not a ‘blue wave’ for the Democrats since the Republicans did better than expected in the Senate.

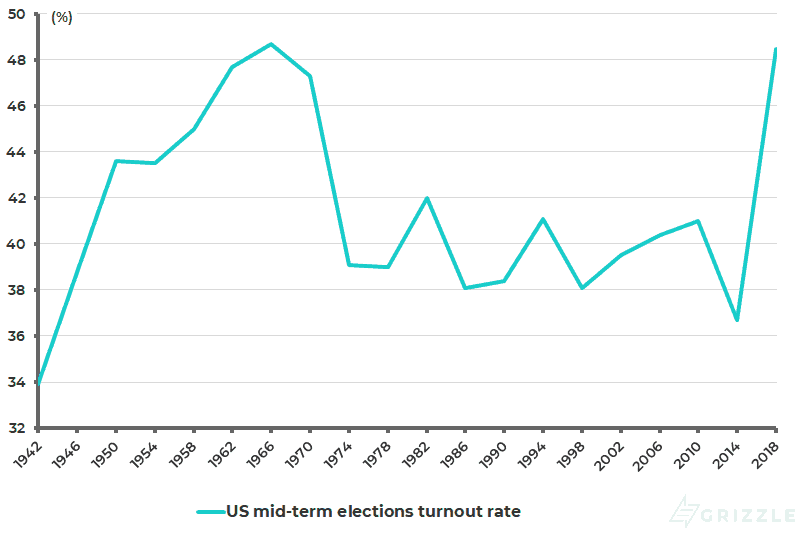

This is a positive for Donald Trump since his own personal campaigning targeted Senate seats. He also succeeded in what he needed to do. That is, he got out the ‘base’ to vote. If the Republican voters had not been energized by the Donald, then there really would have been a ‘blue wave’ since the anti-Trump bloc was definitely motivated to vote. The turnout rate is estimated at 48.5%, up from 36.4% in the last mid-term elections in 2014 and the highest since 1966 (see following chart). Meanwhile, the Republic Congressmen who lost in the House were often more moderate types, whom the Trump supporters were not motivated to vote for.

US mid-term elections turnout rate

From a stock market standpoint, the results should be viewed as a marginal positive since Trump’s position has not been too weakened, though there will doubtless be a lot of impeachment noise. Still, more important from an Asian market standpoint than the mid-term elections, has been newsflow over the past week which has revived hopes that the long-held base case here will end up prevailing, namely that Donald Trump will end up doing a trade deal with China before the next round of tariff hikes are due to be implemented in early 2019.

Positive China Trade Talks and Relaxed Sanctions on Iran

The main development, clearly, was Donald Trump’s tweet on Nov. 1 when he stated that he just had a “long and very good conversation with President Xi Jinping of China” and that trade discussions are “moving along nicely with meetings being scheduled at the G-20 in Argentina”. The key point here is that Trump referred to the fact that he hopes to meet Xi at the G-20 summit in Buenos Aires in late November. He also, interestingly, indicated he had discussed North Korea with Xi on the phone.

This further supports the base case here — namely that Trump will also end up doing a deal with North Korea that would set an investment cycle in that country, a development which will also be supported by China.

Still, as noted numerous times before, for Trump to do a deal with China on trade, and with Kim Jong-un on the nuclear issue, will involve Trump having to part company with his national security hawks, or for the latter to back down.

The latter development is certainly possible, as highlighted by the developments over the past week concerning Iran. After months of telling the world that all purchases of Iranian oil should stop by Nov. 4, the Americans have backed off significantly with eight arbitrarily selected countries (including Italy and Greece!) given slack from enforcing the sanctions. These countries have received waivers to import limited amounts of oil from Iran in the next 180 days.

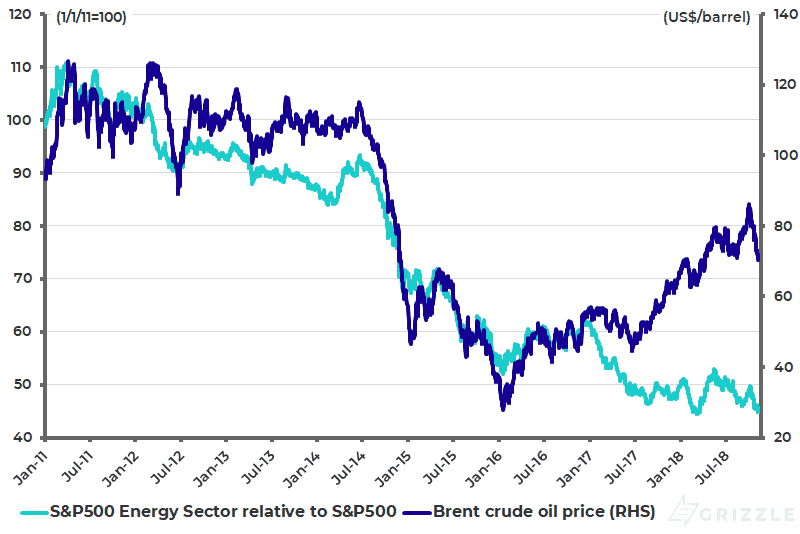

The reason for this U-turn is seemingly Trump’s concern that the oil price would otherwise have spiked, a concern amplified by growing concern that Saudi Arabia could not control the oil price, concerns which have clearly spread to other policy areas related to Saudi. Meanwhile, the recent 19% correction in the oil price to US$70/barrel (see following chart), triggered by the reality that Iran sanctions will be less severe than originally expected, should be viewed as an opportunity to accumulate energy stocks. As for the trade issue, investors should remember one simple point. Trump likes to do deals.

Brent crude oil price and S&P500 Energy Sector Index relative to S&P500

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.