MedMen (CSE: MMEN; OTC: MMNNF) is the poster child for the excesses of the legal cannabis market.

Huge management pay packages, even larger spending and new shares, new shares, and more new shares.

With the capital watering hole evaporating as we speak, MedMen is facing a reckoning.

The company had only $34 million of cash in the bank as of June 29 while it burned $95 million of cash a quarter on operations and facility construction.

With a balance sheet that looks like MedMen ran out of cash in August, investors need to be asking themselves, is MedMen effectively bankrupt?

We went digging to find some answers.

MedMen Needs Cash and Lots of It

With a cashflow burn rate of $90 million per quarter, MedMen needs to keep borrowing for the foreseeable future.

The only reason the company hasn’t run out of money yet is because of a generous loan from Gotham Green Partners.

In the last six months MedMen borrowed $135 million out of a total $250 million, not to mention another $30 million equity deal through Wicklow Capital and Gotham Green. This cash is keeping the lights on.

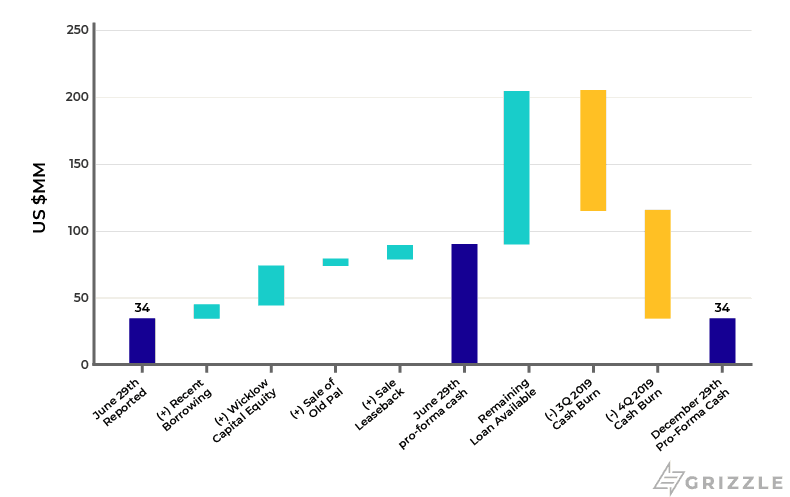

Looking ahead to where MedMen’s cash balance will likely sit at year end, we find a company just hanging on by a thread.

Forecast of MedMen’s Cash Situation

| Cash Balance (Million) | |

| June 29 Cash | $34 |

| (+) Recent Borrowing | $10 |

| (+) Wicklow Capital Equity | $30 |

| (+) Sale of Old Pal | $5 |

| (+) Sale Leaseback | $11 |

| June 29 Pro-forma cash | $90 |

| (+) Remaining GGB Loan Available | $115 |

| (-) 3Q 2019 Cash Burn | $90 |

| (-) 4Q 2019 Cash Burn | $81 |

| December 31st Pro-forma Cash | $34 |

Even if management cuts costs by another 15% over the next six months, the company will enter 2020 with only $30 million or about 1 month of cash.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Keep in mind we assume management maxes out the remaining $115 million loan, even though this is not guaranteed. The lenders have the option but not the obligation to hand out the money to MedMen.[/su_panel]The only way they can avoid borrowing more or going bankrupt would be to cut the cashflow burn by another 60%, an effective 180 degree turn from the growth-focused strategy this management team has favoured all along.

Either way, shareholders are in store for more dilution at best, or will lose it all at worst, as lenders push the company into the bankruptcy courts.

Low on Cash, but Is There Still Value Left for Stockholders

The cash balance is one thing while the value of the company is yet another.

Investors need to be asking themselves if there is enough asset value left for them as MedMen takes on more and more debt to stay solvent.

We have bad news.

Lenders will effectively own MedMen by the end of the year.

MedMen had $635 million of asset value at the end of June, however 40% of that is goodwill and intangibles.

With the current route in Cannabis stocks and lack of profitability, the true value of these assets is likely far lower than where they are listed at today.

We removed goodwill from the asset value, but left some intangibles, assuming a 50% haircut over time.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]We estimate assets left over for investors as of the end of October are only worth $35 million or only $0.07/sh. By the end of the year, assuming MedMen continues to fund the cashflow deficit with debt, there will be negative $0.08/sh of asset value, meaning shareholders will have been wiped out.[/su_panel]| Total Assets (June 29) | $635 MM |

| (-) Goodwill | $86 MM |

| (-) Intangibles 50% discount | $88 MM |

| (+) Value of New Construction | $43 MM |

| Tangible Assets (Oct 29) | $504 MM |

| Total Liabilities (June 29) | $434 MM |

| (+) Debt Since June | $35 MM |

| Total Liabilities (Oct 29) | $469 MM |

| Total Liabilities with Lending Facility (Dec 31) | $584 MM |

| Equity Value (Oct 29th) | $35 MM |

| Per Share | $0.07 |

| Equity Value with Lending Facility (Dec 31) | ($41) MM |

| Per Share | ($0.08) |

What Does This All Mean?

Even though the management of MedMen is justifiably hated by investors who are sitting on large losses, this is a team that built the most well-known cannabis brand in North America.

Owning a strong cannabis brand and some of the most profitable dispensaries in North America means there is huge potential in this business model.

It’s just too bad current shareholders will own very little of that upside.

Management’s aggressive growth has led to runaway debt levels and a situation where when all is said and done, lenders will be the ones owning MedMen, not shareholders.

Unless management immediately begins selling assets while simultaneously going into emergency cost cutting mode, investors should just cut their losses and move on.

There doesn’t look to be any value left for the rest of us.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.