MedMen (CNSX:MMEN), a multi-state cannabis operator, reported another disappointing set of results for the December 2019 quarter-end.

The company remains in a liquidity crisis, and recent cost-cutting just doesn’t look like it will be enough to turn around the stock price without more drastic measures.

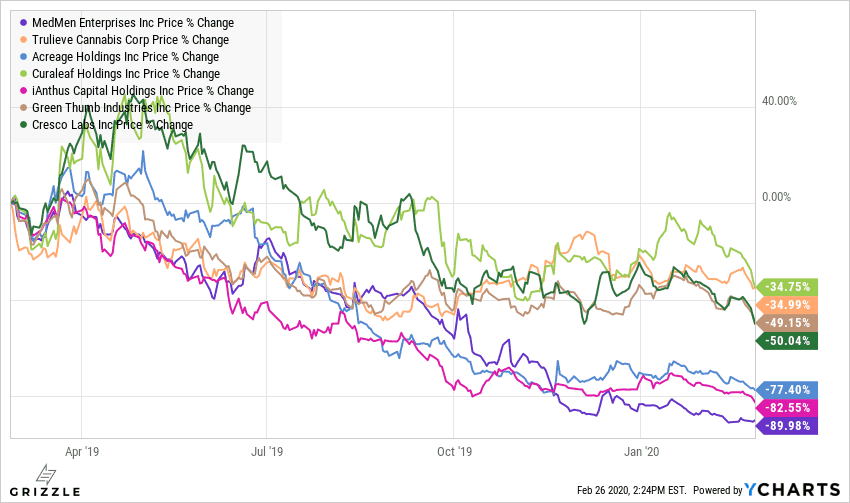

As a result of this cash squeeze, MedMen has been the worst-performing U.S. multi-state operator over the last year and has underperformed similar-sized peers like Trulieve and Cresco Labs by a massive 40%.

Turning to the actual results, revenue came in at $44 million, 32% worse than consensus of $65 million.

Revenue growth of 11% year over year decelerated significantly from last quarter’s annual growth of 105% and has taken the last selling point, growth, out of this story.

With huge losses and cash issues, growth was the last thing MedMen had going for it.

The earnings per share loss of ($0.09) beat estimates of a ($0.10) per share loss.

The company spent $52 million on marketing and salaries this quarter, compared to $50 million last quarter, so even though management is touting an 11% decrease in SG&A, total non-stock-option related corporate expenses actually increased.

If losses don’t shrink dramatically by the end of March we question if management is taking the situation seriously enough.

MedMen’s stock price may have short term rebounds but over the next 1-2 years, the stock will be a loser for investors unless management makes drastic changes.

The time to buy and hold this stock will be when management admits they are insolvent, converts all the outstanding debt to shares and raises adequate cash to start over.

There is still a risk this company is sold for pieces so we highly recommend investors stay on the sidelines and watch the drama play out from a safe distance for now.

Recent U.S. Potstock Performance

We’ve written extensively on how MedMen is a stock in trouble.

Part 1: LINK

Part 2: LINK

Part 3: LINK

To the company’s credit, it does have one of the most recognizable cannabis brands in America and a few dozen prime dispensary locations with high foot traffic.

However, it is struggling to find the cash to pay for a top-heavy corporate structure and the interest on the millions of debt management borrowed to pay for breakneck growth.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]MedMen owes $12 million a quarter in interest and has absolutely no way of affording it with a cashflow loss of $48 million this quarter alone.[/su_panel]Even if management cuts the cost structure and is able to generate positive EBITDA, they still are on the hook for more than $190 million of debt coming due in two years (April, May, and July 2022).

These debt payments will remain a dark cloud hovering over this stock for two reasons.

Number 1: If the company can’t borrow or build enough cash to pay off the debt, they may be forced to restructure again in two years. The stock price could be lower in 2022 than where it is today as a result, even if cashflow has improved.

Number 2: Even if the stock price moves high enough for the debt to convert into shares, that would mean ~100 million shares (25% of the total), would be owned by an entity whose only motivation is to cash out.

The selling of these options by Gotham Green and others could act as a significant ceiling on the stock price until the shares are fully disposed of.

Warning Day Trader’s Only

There are too many things that can go wrong with this stock for investors to dive in looking for a sustainable rebound.

Until the fundamentals tell us otherwise, MedMen remains a vehicle for day traders and nothing more.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.