The Globe and Mail reported today that MedReleaf (TSX: LEAF) management is shopping the company around to other larger licensed producers, specifically Aurora Cannabis Inc. (TSX: ACB). The outcome of a deal, if it does happen, will give marijuana investors a rare look at what company insiders think the future holds for the legal marijuana market in Canada.

See our MedReleaf analysis for a full valuation of the company.

Hint: We think the stock isn’t worth more than $10 per share.

The fact that MedReleaf is looking to sell itself even before marijuana is legal should give all investors pause.

If the upside potential in this industry is as high as all of the management teams tell the public in interviews, earnings calls and press releases, why would MedReleaf management want to sell just when the market is about to take off?

Maybe CEO Neil Closner is actually worried about some of the industry risks Grizzle has been highlighting since January in our back-to-back reports Up in Smoke: The Overvalued Haze of Marijuana Stocks and The Marijuana Export Mirage.

Pro Tip: Watch how much of a premium LEAF sells for if a deal is finalized. This will tell you how much upside marijuana management teams think there is post legalization. If the MedReleaf CEO thought there was more upside than the takeout premium he would never sell the company, so a completed deal will speak volumes about insider sentiment.

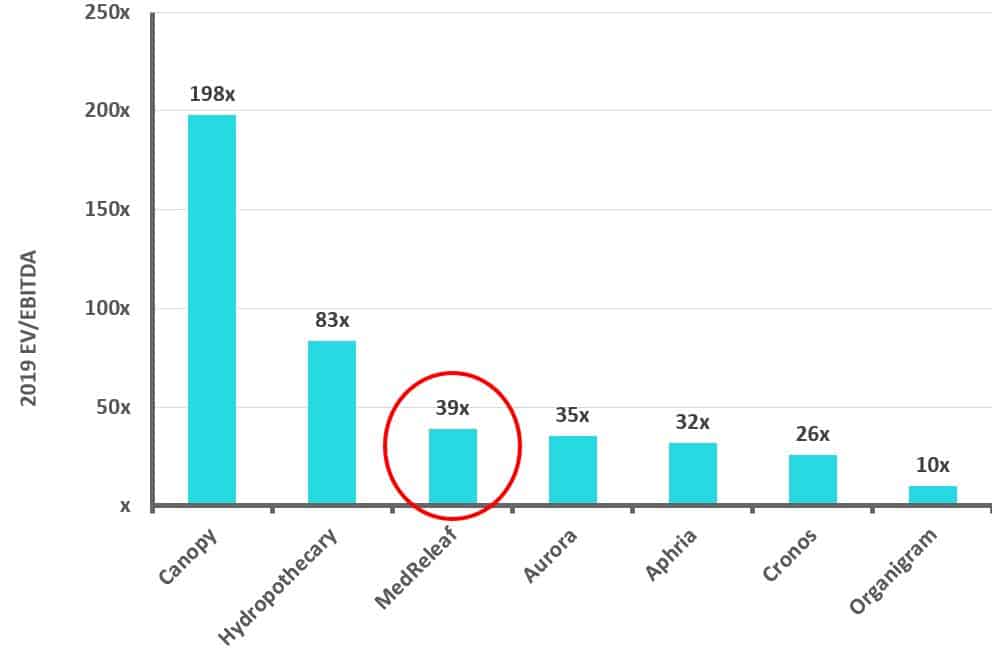

Deal Metrics

EV/EBITDA – LEAF trades at a 39x EV/EBITDA multiple in 2019, a premium to Aurora at 35x, so any deal would immediately dilute Aurora shareholders. Canopy Growth trades at a multiple of almost 200x 2019 EBITDA so a deal with MedReleaf would be accretive any way you slice it.

2019 Consensus EV/EBITDA Multiples

What is a reasonable price to pay for capacity?

We think any deal done at over $12 per gram of capacity will struggle to make money. At $12 per gram a company would need to sell marijuana for $6.50 per gram to make a 10% return on the deal. Aurora and Aphria both paid $50 per gram for deals at the top of the market, requiring them to sell that capacity for $20 per gram for the next 10 years, an impossible goal.

A 20% deal premium would see MedReleaf trade hands for $17 per gram. The acquirer would need to sell LEAF’s 140,000 kg of future capacity for $7.60 per gram equivalent. Assuming 50% of sales are in oil $7.60 requires a wholesale price for oil of $11 per gram, a tall order when this price doesn’t even include excise tax and sales tax.

MedReleaf currently sells its oil for $11.83 per gram to patients but once it has to start selling wholesale to government entities the price they receive will fall at least $2 to pay for the government’s excise tax and allow for a provincial margin.

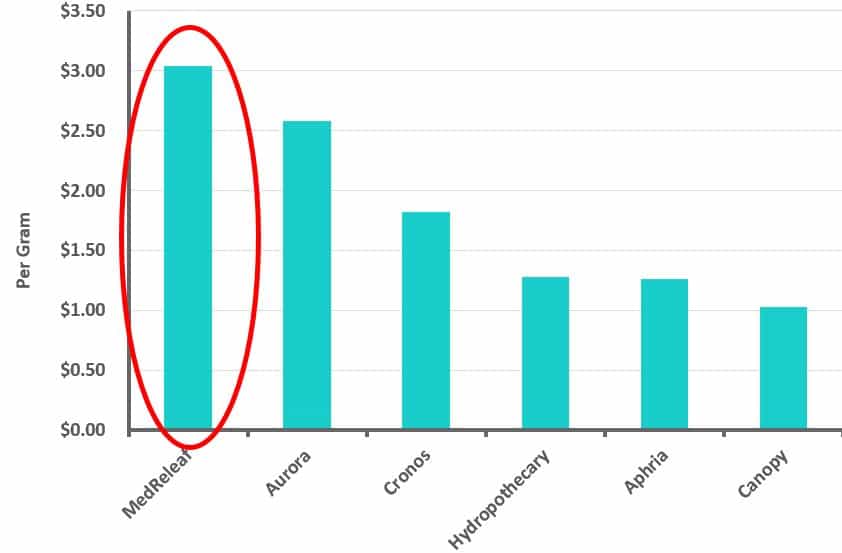

MedReleaf has the highest production costs in the industry

MedReleaf is largely an indoor cultivator and has the highest production costs in the industry as a result. Any licensed producer who buys them will report increasing production costs in the quarter after integration, likely not what the market wants to see when the industry keeps promising lower production costs from ‘economies of scale’.

Production and Processing Costs Per Gram

Source: SEDAR

Bottom Line

Investors should be very wary of an industry where the third largest company is cashing out before the massive market opportunity (their words) has even opened. What do they see coming that public investors don’t?

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.