https://www.youtube.com/watch?v=bwp7Kn7ppFk

Microsoft reported fiscal Q3 2020 earnings results that beat analyst’s estimates.

The stock is up in after-hours trading due to the strong results.

Results were once again driven by a surge in business from Azure, Microsoft’s cloud computing platform with sales up 39% year over year.

The market is still waiting to see what the CEO says in regard to next quarter on the conference call.

Revenue of $35Bn beat estimates for $33.7Bn by 4%

Earnings of $1.40/sh also beat estimates of $1.27/sh by 10%.

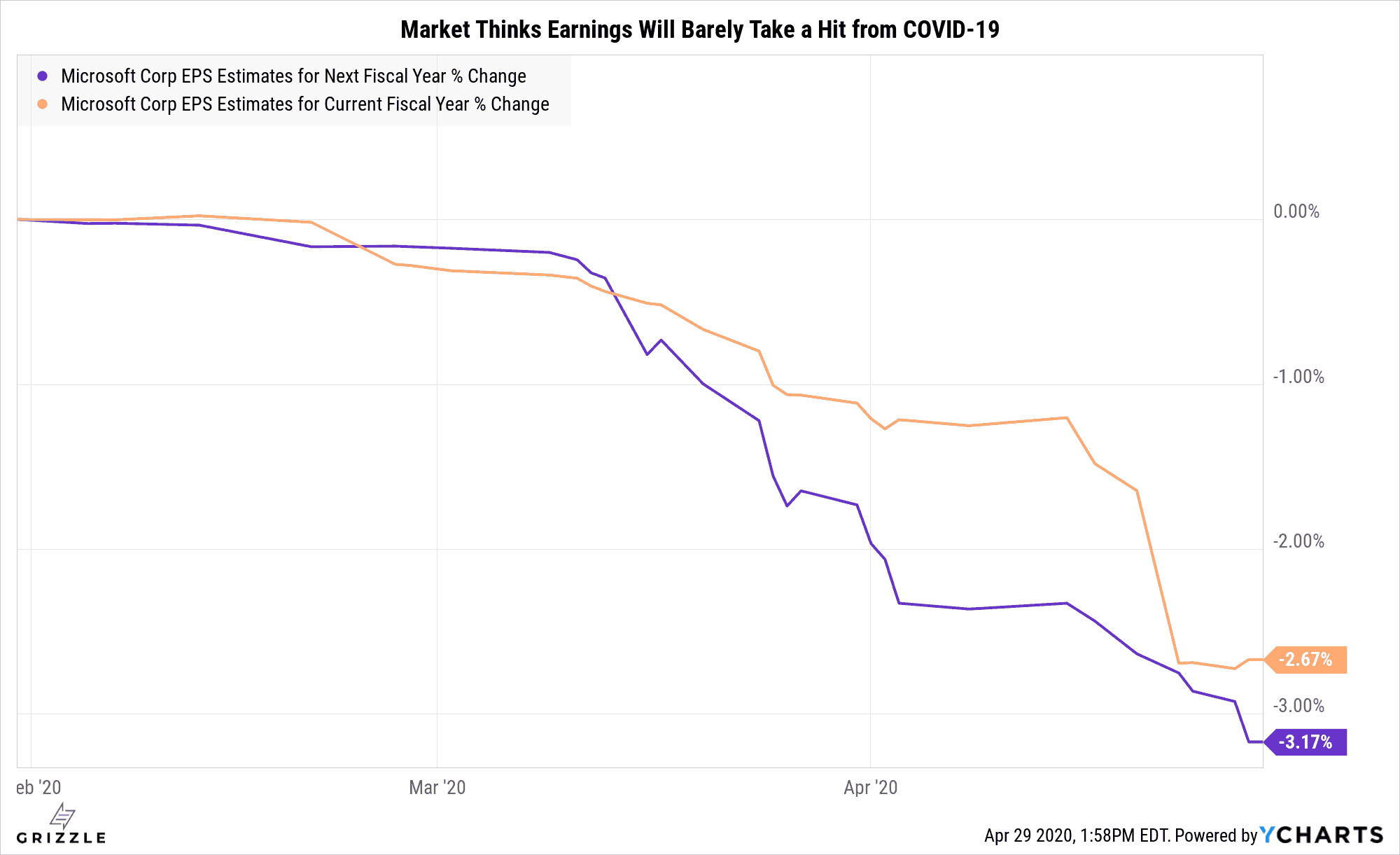

The market remains bullish on Microsoft with earnings estimates for the 2020 and 2021 fiscal years that end in June only coming down 2-3% since the Coronavirus made its debut.

EPS Estimates Only Down 3-4% Since COVID-19 Appeared

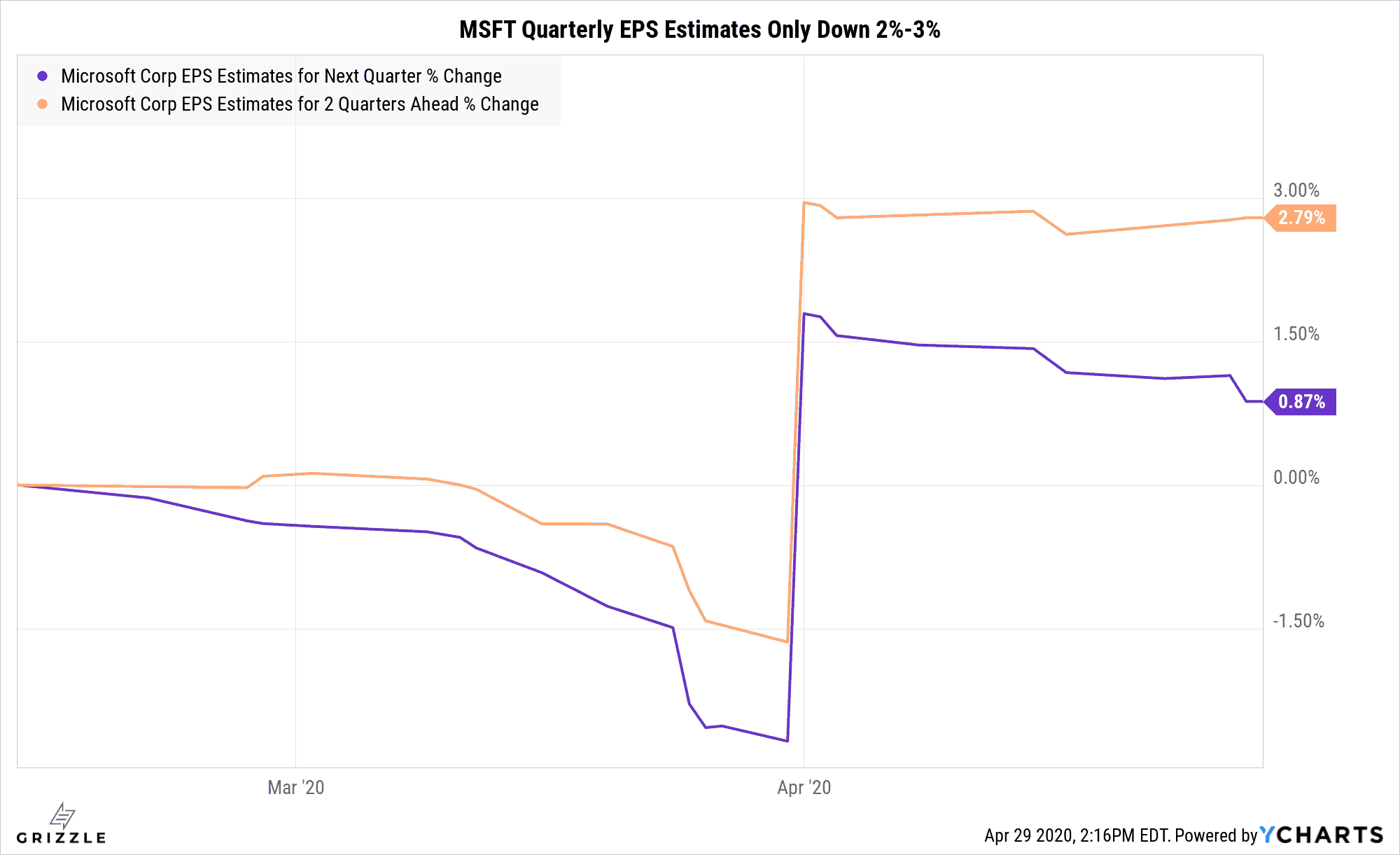

The next two quarters of earnings estimates tell the same story as the annual estimates.

The next two quarters of earnings estimates tell the same story as the annual estimates.

Analysts think earnings will only fall 2-3% due to the economic effects of the Coronavirus.

Quarterly Estimates Also Down Only 2%-3%. Virus What!

This view that software companies are immune to a global slowdown is rampant in the stock market.

If consumers pull back on spending so will the businesses who represent Microsoft’s customer base.

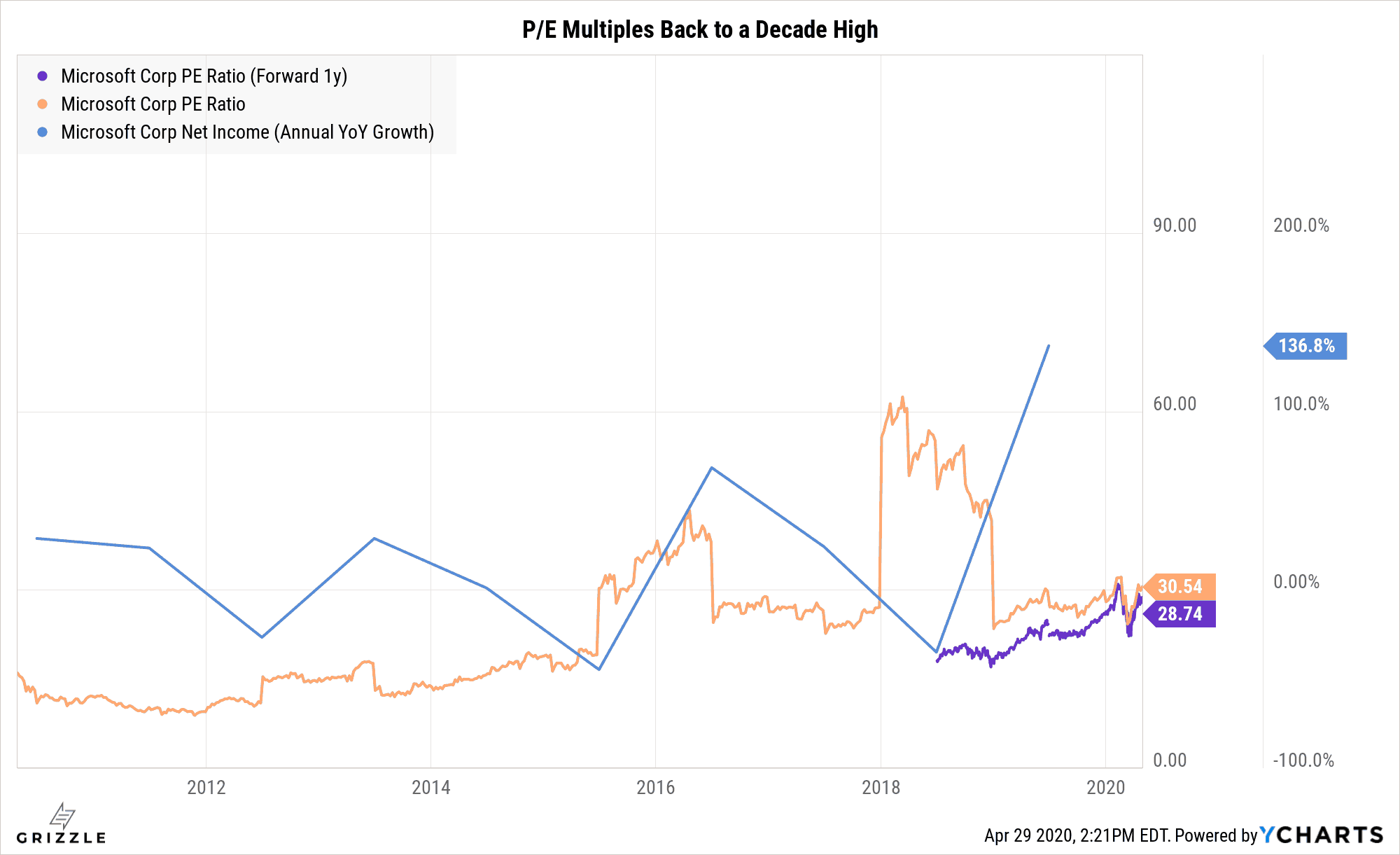

[su_panel]Investors should watch consumer spending data closely and should be wary of SaaS (Software as a Service) stocks in general if consumer spending does not rebound quickly to pre-COVID-19 levels. These stocks are already priced for a rebound. [/su_panel]Microsoft remains a juggernaut in the software space but with the P/E ratio back to a decade high and earnings growth slowing, you are paying a decade high PEG ratio (stock price/earnings growth) to own this stock.

Given the potential risks around a COVID-19 driven pullback in consumer spending we would wait for confirmation that the consumer is truly unfazed before buying in at these levels.

Yes, you’ll miss some upside potentially, but this stock has years of stellar returns ahead of it so being a bit late won’t hurt much at all.

Both the Forward and Historical P/E Multiples are back to a Decade High

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.