There are all kinds of concerns currently percolating in world financial markets, such as a US-China trade war. But what really blows up markets, because it unwinds the models of the algo-driven machines currently dominating US stock market trading, is stocks and bonds declining together, or in other words becoming positively correlated again.

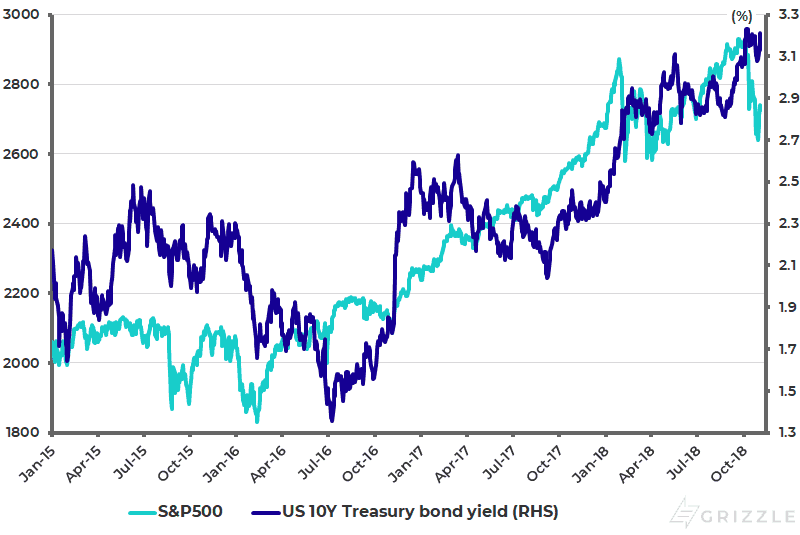

That said, the negative correlation between the two remained during last month’s correction in the US stock market. The S&P500 declined by 10% between Oct. 9 and Oct. 29, while the 10-year Treasury bond yield was down 20bp over the same period to 3.06% (see following chart) which means the price of bonds went up. If this trend finally breaks, in terms of stocks and bonds declining together in price terms, it will be bad news for the so-called the “risk parity” trade and the numerous mechanistic quantitative investment strategies based around some variation of risk parity.

S&P500 and US 10-year Treasury bond yield

The Big Picture is Deflating

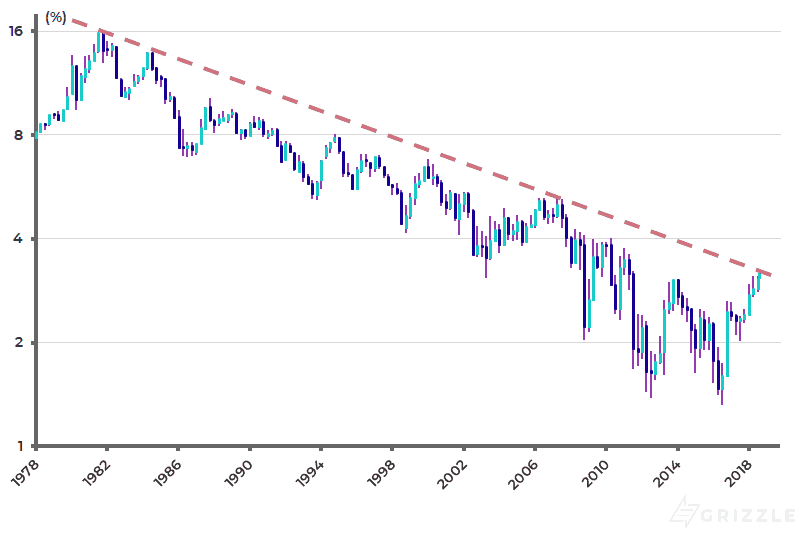

If this is what blows up the machines, and the related quanto-investment strategies investing in this manner, it is not the base case of this writer that the positive correlation resumes. The reason is because the “big picture” trend remains deflationary for all the obvious reasons relating to debt, demographics and technology. In this respect, the 10-year Treasury bond yield has not yet technically broken above the 37-year old trend line based on the quarterly log-scale candlestick chart (see following chart), though the 10-year Treasury bond yield just touched the long-term trend line last month when it reached an intraday high of 3.26% on Oct. 9.

US 10-year Treasury bond yield (quarterly log scale chart)

The Importance of Oil

Still there clearly remains the potential for a further correction in Treasury bonds, driven by a late cycle inflation scare, most particularly if there is a dramatic further spike in the oil price. In this respect, a period of stocks and bonds declining together, even if it is only for a few weeks, can potentially trigger a lot of wealth destruction given the huge amount of leverage invested globally on the assumption that long-term Treasury bond yields will decline when equities correct sharply. In this respect, the so-called ‘risk parity’-influenced models can be discredited even if, after the wipeout, the deflationary trend then resumes and, with it, the likelihood of renewed monetary easing.

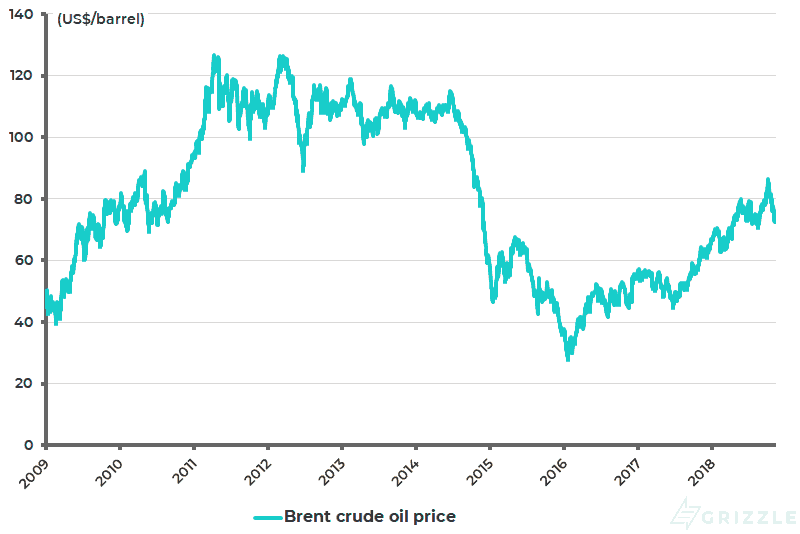

The above is one of many reasons why oil remains a critical factor to monitor. While in the long-term an oil spike through US$100 towards US$150 will be a massive hit to US consumers’ discretionary incomes, the interesting point in the short-term is whether such a move will lead to higher or lower long-term Treasury bond yields.

This is highly relevant because this writer remains firmly of the view that all the risks point to oil trending higher. Oil is also another area where politics is becoming increasingly the critical near-term driver despite the obvious importance of demand and supply issues. Indeed the main reason oil has declined in recent weeks is political. This is because America has backed off enforcing the sanctions on stopping the world buying Iranian oil as previously threatened.

Brent crude oil price

The Politics of Middle Eastern Oil

On this point, to return to the present, Donald Trump made a major bet on Saudi Arabia when he decided to support the Saudi-Israel agenda for America to walk out of the 2015 Iran nuclear deal. One quid pro quo for this is the US$110 billion sale of arms to Saudi agreed in May 2017, the consequences of which are beginning to backfire politically as the world finally starts to wake up to what has been going on in Yemen.

But, more importantly, Trump is now questioning the other ‘quid pro quo’, namely that Saudi will keep a lid on the oil price. This became an even more pressing question for the American president as, with the mid-term elections this week, the risk of a spike in the oil price was rising because of another consequence of Trump supporting the Saudi-Israel agenda on Iran, namely America’s extraordinary unilateral demand that the world should stop buying Iranian oil by Nov. 4.

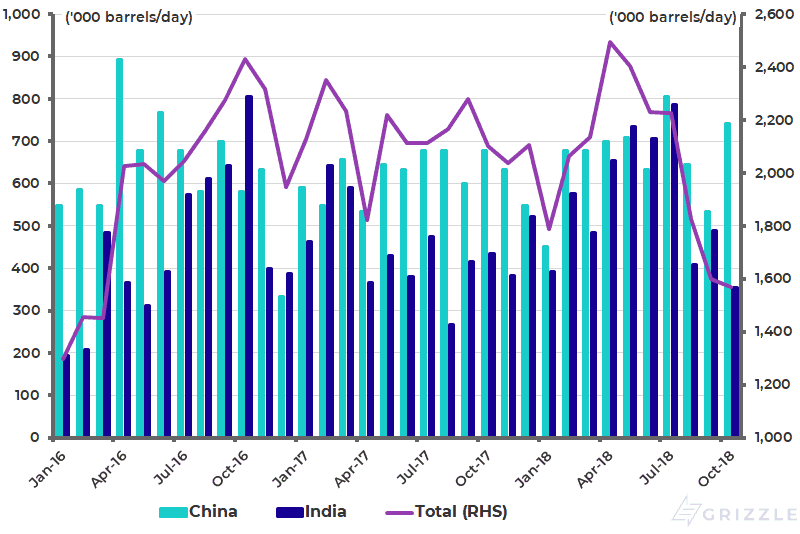

The result is that Iranian oil exports were still running at 1.57 million barrels/day in October, though down from the recent peak of 2.5 million reached in April, according to the tanker-tracking data compiled by Bloomberg (see following chart). That is, even though the ban on purchases of Iranian oil is meant to be effective on Nov. 4.

Iran total crude oil exports and exports to China and India

Meanwhile, the interesting longer-term point is whether Saudi has the technical ability, in terms of excess pumping capacity, to increase production in the way it claims to have. This needs to be questioned given the fact that the Saudi Aramco IPO is not happening. This lends credence to those who have been arguing for years that Saudi’s oil reserves are nothing like as high as the 260 billion barrels they are claimed to be.

The original work on this was done by Matthew Simmons in a 2005 book Twilight in the Desert: The Coming Saudi Oil Shock and the World Economy. The historic point to note about this issue is that the last published reserve figure, complying with US reserve reporting requirements, was published 42 years ago in 1976. Meanwhile, the more Saudi’s real oil reserves are lower than the official figure, the less likely it becomes that Saudi can pump oil at 10m barrels/day forever, as the world’s oil traders have always assumed.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.