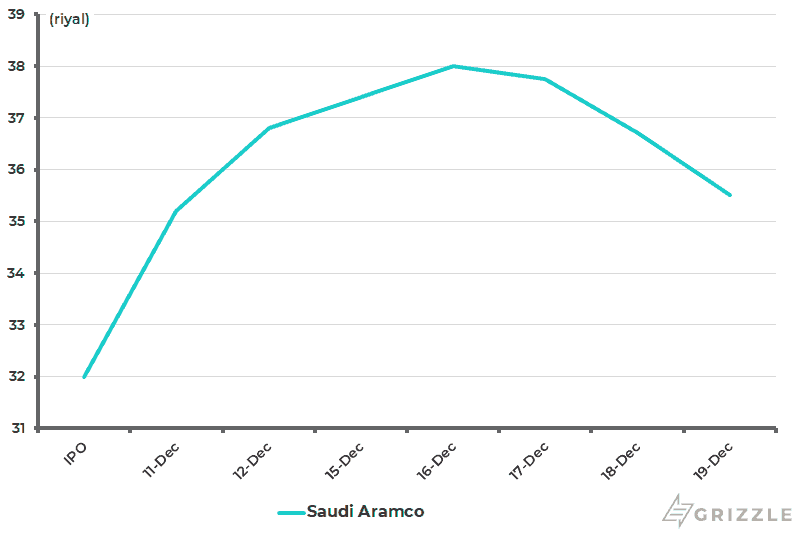

There has been a lot of coverage of late on the IPO of the long-anticipated listing of Saudi Arabian’s oil giant Aramco. Clearly the issue turned out to be smaller than originally anticipated and at a lower price. Aramco sold just 1.5% of the company, or three billion shares, at 32 riyals per share, valuing the IPO at US$25.6 billion. This put the company at a market value of US$1.7 trillion, below the US$2 trillion previously targeted by Saudi Crown Prince Mohammed bin Salman. The interesting technical issue is the generous margin facility offered to retail investors in what was primarily a domestic listing. Aramco began trading on the Saudi stock market on Dec. 11. It is currently trading 11% above the issue price (see following chart).

Saudi Aramco Share Price

De-escalation of Tensions in the Middle East

The Aramco issue is also a reason to focus again on the Middle East. In the summer it looked like the Middle East was closer to a full-scale conflict than it had been for a long time (see Grizzle article Oil: Market not Factoring in Iranian Political Risk, Sept. 5, 2019). One week later on Sept. 14, Saudi oil infrastructure was attacked by drones and cruise missiles launched from Yemen, a move that everyone in the region assumed to have been instigated by Iran. Indeed, the widely accepted view in the Middle East is that this attack was essentially a declaration of war by Iran in the sense that Tehran would have known that making such a move risked precipitating a full-scale conflict, as opposed to yet another of the region’s many proxy wars.

However, the opposite happened. Rather than retaliating, the opponents of Iran in the region have backed off. First, the Trump administration has conspicuously failed to come to the defence of Saudi, even though Saudi’s annual purchases of U.S. weapons are running at an estimated US$14 billion. Even better, from an Iranian perspective, national security hawk John Bolton, who has for years been publicly advocating going to war with Iran, was sacked from the Trump administration in September. This has increased the conviction level in the Middle East that the U.S. under Donald Trump is withdrawing from the region.

If Washington has not responded to the Iran aggression, the UAE and Saudi, the leading regional protagonists of the proxy war campaign against Iran in recent years, have also backed off. The UAE has effectively exited the disastrous proxy conflict in Yemen, while the view is that Saudi is in the process of trying to do so. Similarly, there are signs that the UAE and Saudi are re-thinking the 30-month-old blockade of Qatar that was originally triggered by Qatar’s close relationship with Iran.

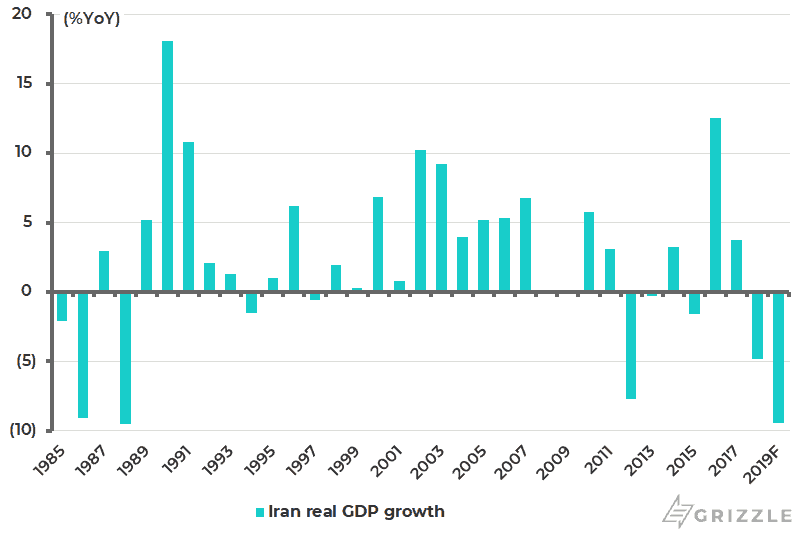

All of the above suggests that tensions have reduced markedly since the summer, when there was genuine concern that a full-scale regional war was imminent. This was because the feeling was that Iran had been pushed to the wall by the undoubtedly negative impact on its economy of the re-imposition of U.S. sanctions as a consequence of the Trump administration’s unilateral decision in May 2018 to pull out of the 2015 Iran nuclear deal, known as the Joint Comprehensive Plan of Action (JCPOA). Thus, estimates are that Iran GDP will contract by 9.5% this year, according to the IMF, after declining by 4.9% YoY last year (see following chart).

Iran Real GDP Growth

The message from that attack on Saudi oil infrastructure following other moves, such as the seizing of a British-flagged tanker in July, was that Iran had been pushed to a point of no return in terms of its willingness to risk a full-scale conflict. Similarly, the conclusion to be drawn from the reaction of Iran’s regional enemies is that they have no appetite for such a conflict, most particularly if Washington is not prepared to lend a helping hand. Indeed, sentiment has now swung to such extremes that there is even speculation that there are behind-the-scenes discussions between Washington and Iran in terms of reviving the nuclear deal and pulling back from the sanctions.

While a renewed détente between Washington and Tehran is certainly not the base case, anything is possible with the transaction-oriented Trump, most particularly with Bolton having departed the scene; though the recent large demonstrations in Iran regarding rising fuel prices will have strengthened the hawks looking for regime change.

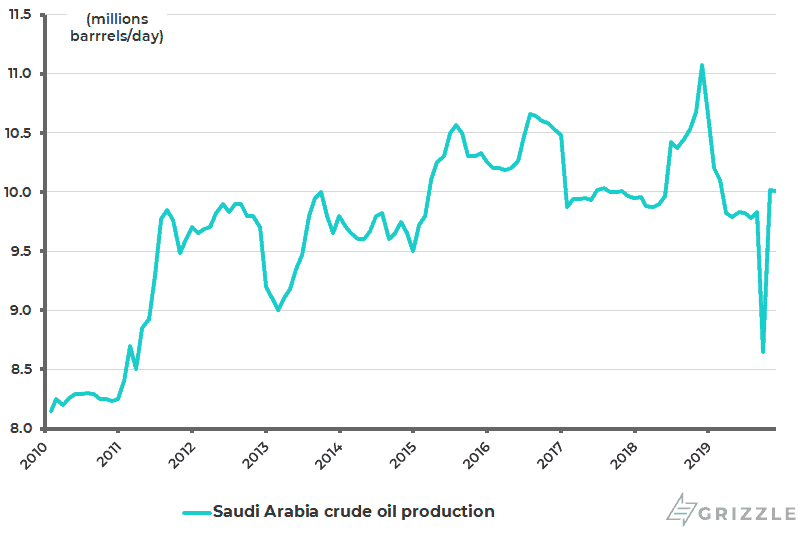

Meanwhile, Saudi and UAE foreign policy appears to have backfired badly in the sense that they seem to be in full-scale retreat from their previous foreign policy goals. This appears to be driven by real concern about further attacks on their infrastructure, which includes not just oil infrastructure but also desalination plants. In this respect, it is probably the case that the attack on Aramco’s two major oil facilities in mid-September has done more lasting damage than has been officially admitted to, though production is back to August levels, based on industry data (see following chart).

Saudi Arabia Crude Oil Production

Saudi’s Diversification Away from Oil

If this is the current context, it is also widely believed in the region that one reason America is in retreat from the Middle East is because it no longer needs the region’s oil because of its own domestic production, courtesy of the shale boom. This, and the now widely believed-in end-of-fossil-fuels story, is also why Saudi’s de-facto leader, Crown Prince Mohammed bin Salman (MBS), has pushed domestic reforms, the most notable of which is the new freedom given to women to enter the workforce.

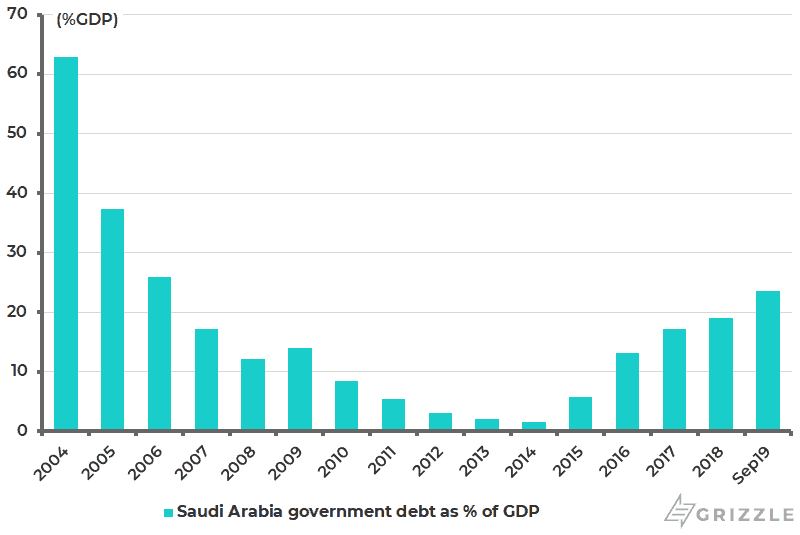

This should be very bullish for consumption and productivity. It also reflects the realization that Saudi cannot rely on oil and gas forever. Thus, one reason to list Aramco is to raise funds to finance the diversification of the economy. Saudi needs oil at US$85/barrel to balance its budget, while Saudi’s government debt to GDP is now at 24%, up from 1.6% in 2014 (see following chart).

Saudi Arabia Government Debt as % of GDP

Where Do Oil Prices Go From Here?

This raises again the issue of the oil price. Although the fossil fuel industry is seemingly living on borrowed time, with much talk of “stranded assets” by central bankers wishing to establish their “climate” credentials, I still believe there is scope for another big move up in the oil price before all the predictions of the end of the oil era become reality.

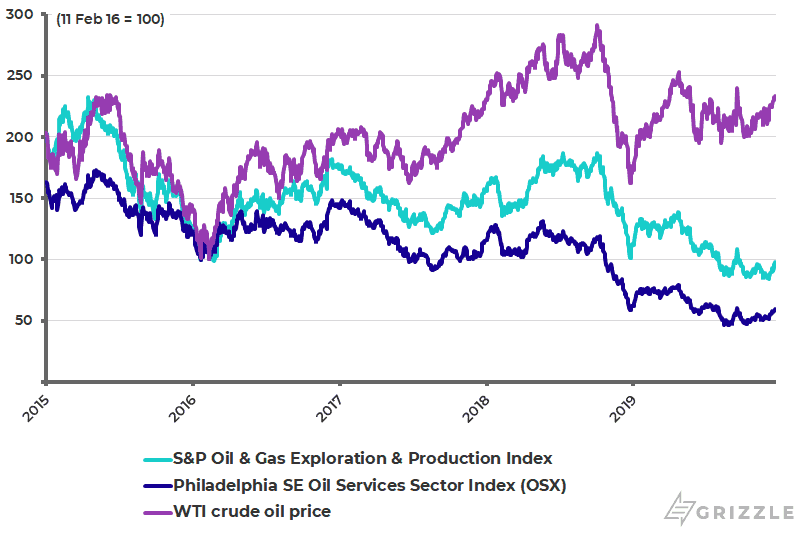

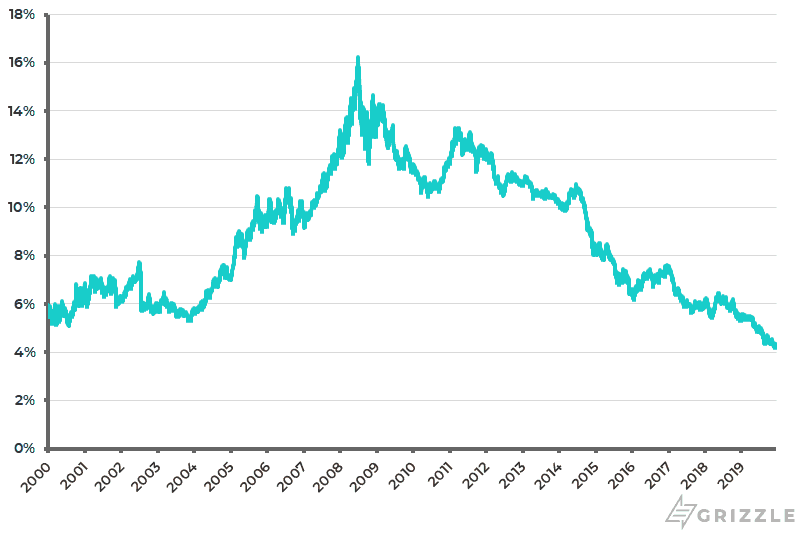

In this respect, there is also scope for a big move up in oil stocks, which are the big laggards in the now fashionable pro-cyclical “value” trade. Indeed, oil stocks have massively underperformed oil since oil bottomed in early 2016. Thus, the WTI crude oil price has risen by 135% since bottoming in February 2016, while the S&P Oil and Gas Exploration and Production Index and the Philadelphia Oil Service Sector Index (OSX) are down 2% and 40%, respectively, over the same period (see following chart). Indeed oil-related stocks now account for only 4% of the S&P500, down from a peak of 16% in mid-2008 (see following chart).

Oil Stocks and Oil Price

S&P500 Energy Index’s Weighting in the S&P500

U.S. Oil Production Not as Strong as Believed

The continuing constructive view on oil is partly based on the assumption that demand in emerging markets will remain strong and partly on the view that investment by the conventional oil industry will remain weak precisely because of the widespread view that the fossil fuel industry is living on borrowed time.

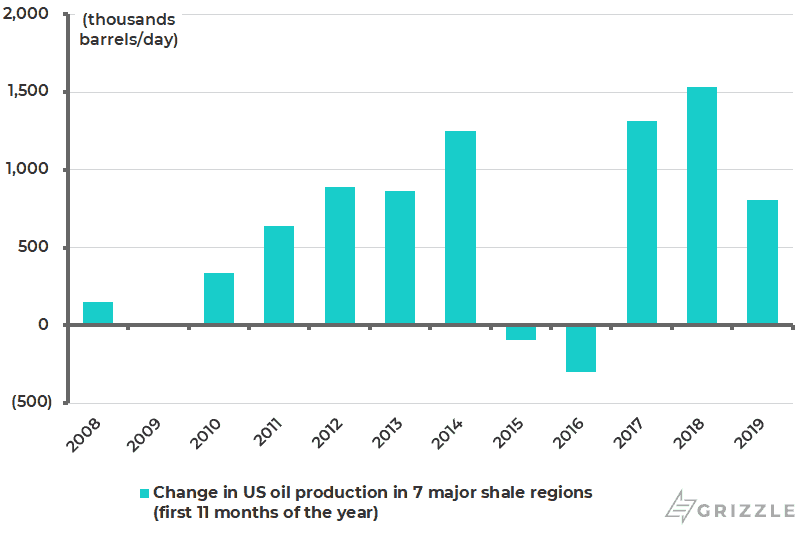

Even if both premises are valid, the assumption until now has been that the U.S. shale boom will continue to make up for the shortfall from the decline in conventional investment. This is why it is worth highlighting that U.S. shale production growth has slowed sharply this year. Thus, U.S. oil production in seven major shale regions increased by only 73,310b/d per month in the first 11 months of 2019, compared with 139,526b/d in the first 11 months of 2018 (see following chart).

Change in US Oil Production in 7 Major Shale Regions (January-November)

The issue raised by this slowdown is whether this is just a temporary phenomenon, or whether shale has reached an inflection point because the most productive areas of America’s main shale areas, which are the Bakken, Eagle Ford, and the Permian, have peaked. I hear that Bakken and Eagle Ford are exhausted, which means that, going forward, most non-OPEC production growth will have to come from the Permian.

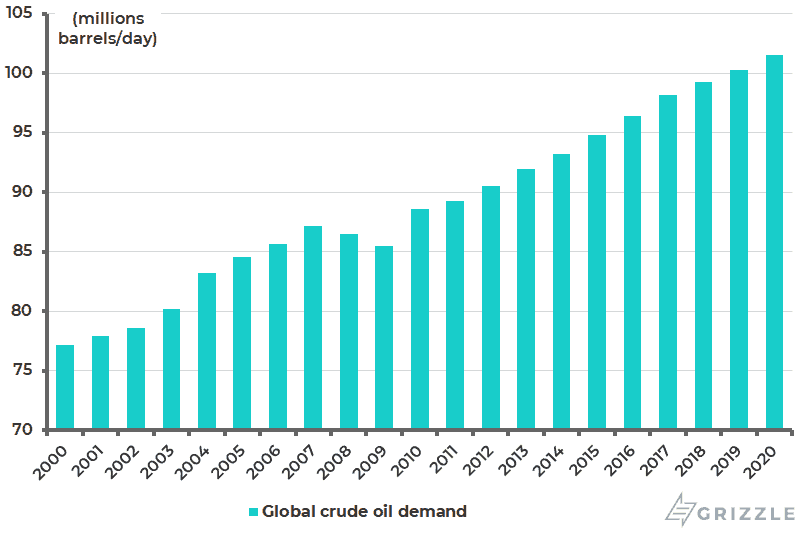

This is the context in which it needs to be remembered that global crude oil demand has increased by 11m barrels/day over the past eight years (see following chart). So, if the fossil fuel era is ending, there is little sign of it right now. Indeed, it is also worth noting that the International Energy Agency (IEA) has a long-established track record of underestimating demand almost every year, particularly emerging market demand.

Global Crude Oil Demand

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.