Mitek Systems Inc. (NASDAQ: MITK) has flown under the radar in recent years as the Trump bull market shined the spotlight on large-cap stocks. Cyclical rotation and the ensuing FAANG bleed out of Q4 has forced many investors to broaden their horizon, even when it comes to the high-flying computer and technology group. Mitek offers a combination of strong historical growth, sector outperformance, and suitor buyout protection for investors keen on snatching up small caps on the cheap.

Niche Player in a High-Growth Segment

Mitek is a California-based software company that specializes in digital identity verification using mobile capture technology and artificial intelligence. Its flagship mobile check deposit software has been integrated into various mobile banking apps, which allow customers to deposit checks using their smartphone’s built-in camera. Mitek is essentially a fintech company that innovates so traditional banks don’t have to – something that is fairly common in the financial sector.

According to Mitek’s official website, its mobile check deposit product is trusted by 99 of out of the top 100 U.S. banks. The rise of digital natives and preference for online/mobile banking means digital identity verification isn’t running out of style anytime soon. The fact that Mitek works with financial service providers and not against them (like Square, for example) gives it a high ceiling with limited downside.

Buyout Offers

It’s worth mentioning that Mitek is a highly coveted enterprise that has been the subject of takeover speculation for quite some time. Just last quarter, the California-based company rejected a $380 million buyout offer from the Elliott Management-funded ASG Technologies Inc. According to Reuters, ASG first made an offer to buy Mitek last summer at a “significant premium” in an effort to expand its fintech offerings.

Mitek’s official response suggests the company is confident its growth will eclipse the $10 per share offer tabled in November:

ASG has since upped its offer to $11.50 per share, according to Reuters.

Strong Revenue, Strong Guidance

Mitek’s fiscal first quarter surpassed analysts’ expectations on both the top and bottom lines. The company earned $0.03 per share on revenues of $17.7 million. Analysts had called for per-share earnings of $0.02 on revenue of $17.25 million. Sales surged 44% compared to a year ago.

Annual revenue growth has been on a tear since at least 2014:

| Year | Annual Revenue |

| 2014 | $19.15 million |

| 2015 | $25.37 million |

| 2016 | $34.70 million |

| 2017 | $45.39 million |

| 2018 | $63.56 million |

Source: Company Filings

For fiscal 2019, Mitek Systems has a sales target of between $83-$86 million. Investors can, therefore, expect another record-setting year for the software company.

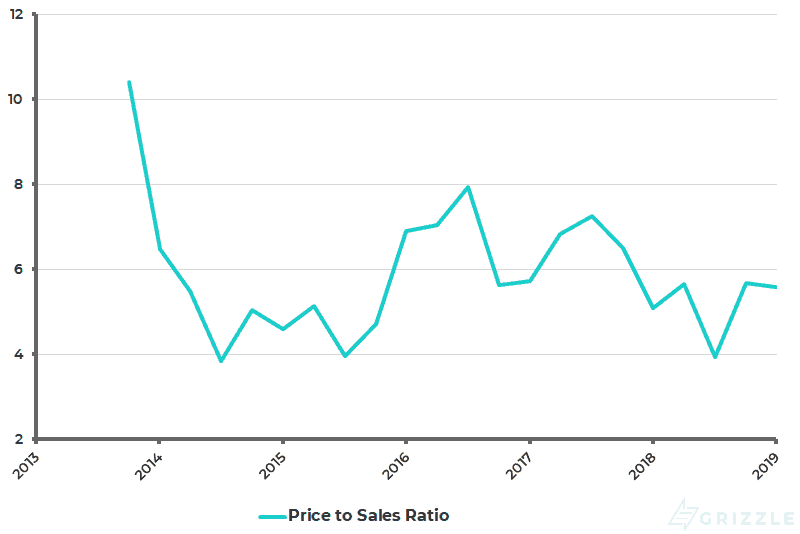

MITK shares currently trade at $10.60. The company is considered significantly undervalued based on the profit-to-sales (P/S) ratio, especially when you factor the above-mentioned revenue growth. Mitek’s P/S ratio was valued at 5.60 as of Feb. 26.

Despite struggling this year, Mitek’s share price has been a perennial outperformer. The stock has returned 36% over the past 12 months and 77% in the last two years, way above the Nasdaq Composite Index.

Mitek Systems has emerged as a revenue stalwart in the small-cap space. Analysts believe the stock’s ceiling is quite high given the underlying investment thesis and history of steady growth.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.