https://youtu.be/hMcdrgB9wts

Thomas George gives his take on Chris Wood’s latest piece on how Modern Monetary Theory is a socialist economic theory is trying to counter quantitative easing, but in reality both are just quackery.

This column referred recently to the current competition among Democratic presidential candidates to sound more socialist. But the resurgence of the political left, the subject of a cover story in The Economist last month (“The Rise of Millennial Socialism”, Feb. 16, 2019), also has relevance for monetary policy. This is because of the growing popularity on the left of so-called Modern Monetary Theory (MMT).

What is MMT?

A glance at Wikipedia defines MMT as “a heterodox macroeconomic theory that describes the currency as a public monopoly and unemployment as the evidence that a currency monopolist is restricting the supply of the financial assets needed to pay taxes and satisfy savings desires”.

If such a definition is not particularly satisfactory, a better one perhaps is provided in the relevant article in the above mentioned issue of The Economist which described MMT as a theory “which holds that the primary constraint on government spending is not how much money can be raised through tax or bonds, but how much of an economy’s capital and labour the state can use without sparking rapid inflation”.

Why is MMT Gaining Traction?

The significance of the above is, clearly, that belief in MMT undermines all the arguments for government austerity and fiscal rectitude. Indeed it turns such arguments completely on their head. If this is the theory behind MMT, the practical reason why it is gaining traction on the left is because ten years of quantitative easing and surging fiscal deficits in the G7 world have not led to surging inflation. In fact, they have led to the opposite. This leads to the tempting conclusion that there is lots of room to increase government debt still further.

Indeed this theorizing has been encouraged by the advocates of unorthodox monetary policy themselves. Take for example a book written three years ago by Adair Turner, a former British financial regulator and chairman of an entity with the self-important title, the “Institute for New Economic Thinking” (Between Debt and the Devil: Money, Credit and Fixing Global Finance by Adair Turner, Princeton University Press).

Turner argues in this book that in a fiat paper money system the authorities can never run out of ammunition to stimulate demand. In terms of his specific recommendation of central bank financing of fiscal deficits, he argued that the authorities should make an explicit commitment that this increase in financing is “permanent”. How would this work in practice? Say a government is running a fiscal deficit of 10% of GDP, the authorities would make an explicit commitment that, say, 5% of this deficit is overtly financed with central bank money; that this increase is permanent, and that the additional 5% does not increase the formal measure of government debt as a percentage of GDP.

With such theories being advocated by conventional types, it is not surprising that the so-called “radical left” has been tempted to take such arguments to their logical conclusion. Indeed MMT is the logical consequence of the fundamental blurring of the distinction between monetary policy and fiscal policy which was a central characteristic of quantitative easing.

How Quanto Easing Caused Income Inequality

There is, of course, an irony here since Ben “Billyboy” Bernanke’s aggressive pursuit of quanto easing after the global financial crisis was, as discussed here on several occasions in the past, the chief driver of the growing inequality of wealth distribution which now so upsets the political left. This is precisely because quanto easing in the developed world led to surging asset prices, and assets are primarily owned by the rich either because they have the wealth to buy the assets or because they have had, under QE, access to ultra-cheap credit to borrow lots of money to buy still more assets.

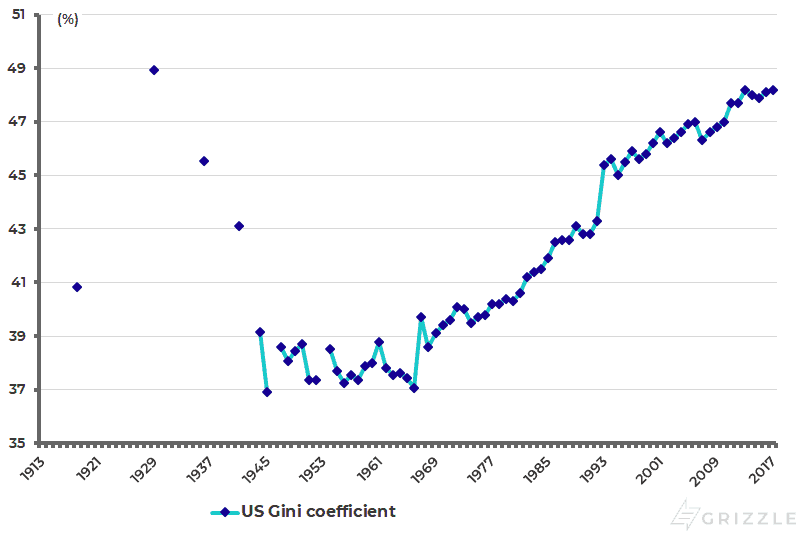

The result of the above is that the Gini coefficient (a statistical measure of income inequality — a coefficient of zero expresses perfect equality, while a coefficient of 1 expresses maximal inequality) did not peak in America with the financial crisis in 2007, as it should have done and as it did with the Wall Street crash in 1929.

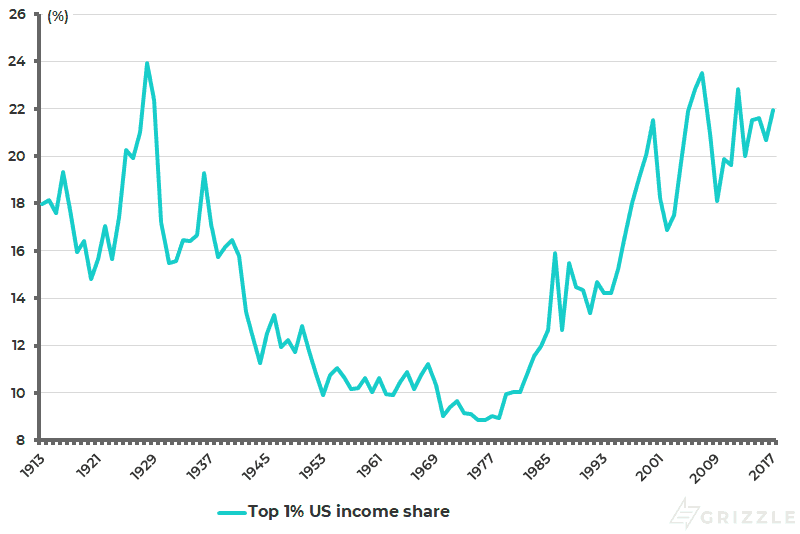

The top 1% of Americans’ share of U.S. income has risen from 18% in 2009 to 22% in 2017, while it declined from a peak of 24% in 1928 to 15% in 1931 (see following chart). So wealth inequality became further extended as the rich were bailed out of the massive losses they would have sustained in leveraged credit instruments in 2007 and 2008 if capitalism had been allowed to work as it should have been. Thus, the Gini coefficient for U.S. households has risen from 0.463 in 2007 to 0.482 in 2017 (see following chart).

Top 1% U.S. income share

U.S. Gini coefficient

The above actions have discredited the system in the G7 world and therefore discredited the political, financial, and business elite in the G7, who can perhaps best be defined as the people who show up at Davos or, at least, used to show up. One consequence was the election of Donald Trump who, for all the antagonism directed at him by the millennial left in America, has nothing in common with the Davos mob. Another consequence is the risk of a much more left-wing president in America should Trump loses the next election. Consider, for example, the 29-year-old Democratic Congresswoman Alexandria Ocasio-Cortez’s advocacy of a 70% marginal tax rate on the highest incomes or for a “Green New Deal”. Clearly, one aspect of the new millennial socialism is a politicized obsession with the environment and “climate catastrophe”.

Can MMT Actually Work?

It is the case that most people understand that “soak the rich” taxation, however appealing personally, does not raise revenue meaningfully on a macroeconomic basis. But this is precisely why the appeal of MMT is so strong because it allows for seemingly unlimited fiscal expansion so long as inflation is quiescent. That is not surprising since advocates of unorthodox monetary policy have already pushed the envelope out a long way.

If financial conjuring tricks were as simple as outlined by the advocates of MMT, it would really mean that there is such a thing as a free lunch which, of course, there is not. This is why governments and central banks who connive in such policies will ultimately be discredited along with the currencies and the currency systems they preside over. In this respect, I agree with The Economist in its editorial on millennial socialism when it opines on MMT that “the notion that unlimited borrowing does not eventually catch up with an economy is a form of quackery”. Still, I have also always believed, unlike The Economist, that quanto easing is another form of quackery.

What Investors Need to Know

If all of the above is true, investors need to understand that MMT now exists as a theory to justify ever more extreme unconventional policies in the next downturn, and that there will be plenty of politicians willing to jump on that bandwagon. That is a political reality for those with capital to protect, which is why ownership of gold bullion remains essential as the financial equivalent of term life insurance. It is also why the blockchain-enabled cryptocurrency approach remains an area of promise for those who want to escape the statist nightmare which would be the practical consequence of a government implementing MMT.

In this respect, if MMT is taking the logic of quanto easing to its ultimate conclusion by effectively eradicating the distinction between monetary policy and fiscal policy, it is also the logical consequence of the current U.S. dollar-based fiat paper monetary system which has been in existence since former U.S. President Richard Nixon broke the last link with gold in 1971. This is simply because this 48-year-old system has no real discipline attached to it.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.