India has long been my favourite Asian stock market. It is, therefore, of note that the result of the Indian general election is due to be announced in the next few days. The local stock market will want to see Prime Minister Narendra Modi re-elected for another five years.

The latest opinion polls released in early April show a range of 261-310 of the 543 parliamentary seats for Modi’s BJP-led National Democratic Alliance (NDA) with an average of 280 seats, eight seats higher than the required majority of 272 seats (see following chart). This compares with only 137 seats for the opposition Congress-led United Progressive Alliance (UPA). It should be noted that the Election Commission has banned exit polls during the election period between April 11 and May 19.

Opinion polls forecast seats for India general elections (polls released in April 2019)

| Polling Agency | NDA | UPA | Others |

| TV9-Cvoter | 261 | 143 | 139 |

| CSDS-Lokniti | 273 | 125 | 145 |

| India TV-CNX | 275 | 147 | 121 |

| Times Now-VMR | 279 | 149 | 115 |

| Repbulic-Jan Ki Baat | 310 | 122 | 111 |

| Average | 280 | 137 | 126 |

Note: Total parliamentary seats = 543 seats. Source: Polling agencies

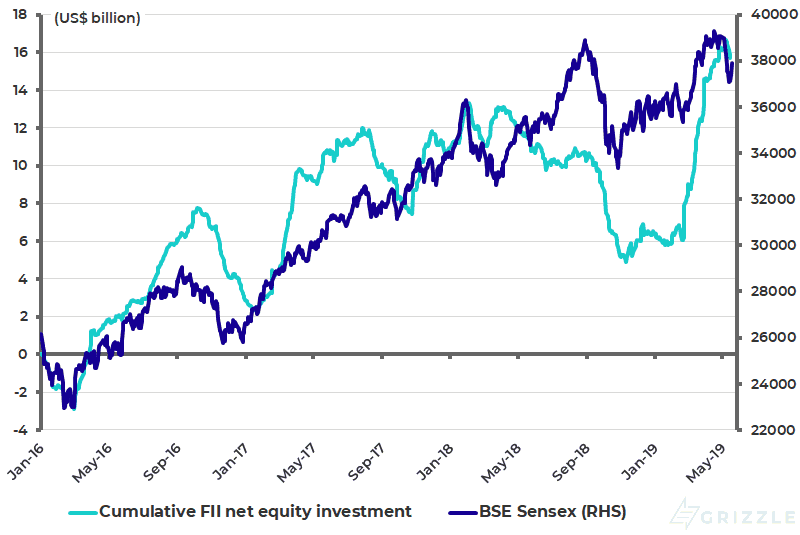

Meanwhile, there has been US$7 billion of net buying of Indian equities by foreign investors since an opinion poll was published in early March by India TV-CNX (see following chart) showing a big increase in support for the BJP following the Indian airstrikes in late February in Balakot in Pakistan.

Cumulative net foreign buying of Indian equities

Modi’s Impact on India’s Economy

The base case has always been that Modi would win again. But there is no doubt that concerns had been growing in price to the military skirmish in Pakistan that Modi’s structural reforms, such as demonetization and the introduction of a Goods and Services Tax (GST), caused economic pain in the first instance. Demonetization, when all Rs500 and Rs1,000 banknotes were taken out of circulation, particularly hit small businesses.

This is why the military skirmish with Pakistan may prove the equivalent for Modi of what the Falklands War was for former British Prime Minister, the late and great Margaret Thatcher, in 1982. For prior to that event, and the related surge in jingoism, Thatcher was looking far from guaranteed for re-election as the media and the masses attacked government spending “cuts”.

As for Modi, he has seemingly reaped the rewards of a robust response to the killing of more than 40 Indian soldiers in Indian-administered Kashmir on Feb. 14. To remain effective, Modi’s style of highly centralized government requires a big majority for the BJP.

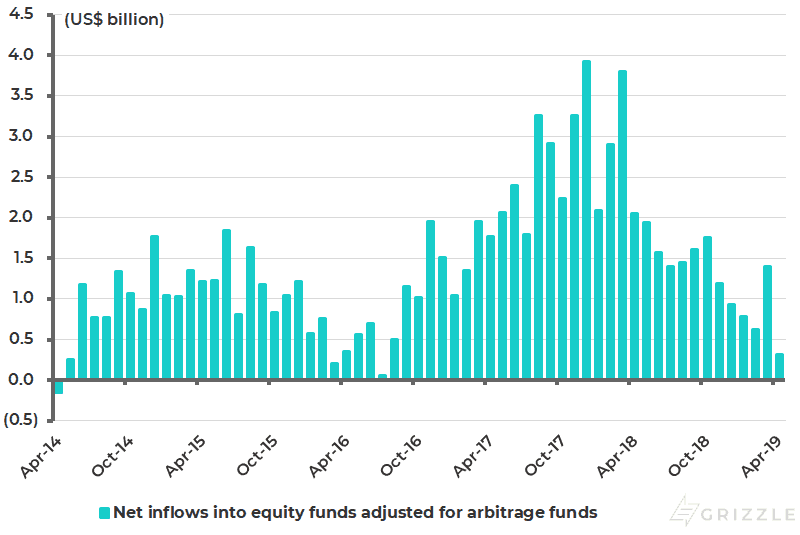

Meanwhile, one point is crystal clear. Domestic investors like Modi since domestic equity mutual funds have seen net inflows every month since he assumed power in May 2014. Domestic equity mutual funds’ monthly net inflows, excluding arbitrage funds, have totalled US$3.1 billion in the first four months of calendar 2019 and US$86 billion since May 2014 (see following chart). Prior to Modi’s arrival inflow there had barely been any inflows.

Net inflows into Indian domestic equity mutual funds (excl. arbitrage funds)

Foreign Investment in India

Despite their recent buying, there is definitely room for foreign institutional investors to increase weightings further as they have not really added to their holdings in Indian equities for three years. Thus, net foreign portfolio investor equity inflows into India, adjusted for dividends paid on their holdings, were almost zero over the past three calendar years.

Foreign portfolio investors have recorded net inflows into Indian equities of US$6.4 billion over the past three years, equivalent to about 4% of their outstanding investment at the end of 2015. This is almost the same as the aggregate dividend yield for the Indian stock market over the past three years, which has been running at around 1.3-1.5%. Foreigners have bought a net US$9.4 billion worth of Indian equities so far in 2019, equivalent to about 5% of their estimated holdings at the end of 2018.

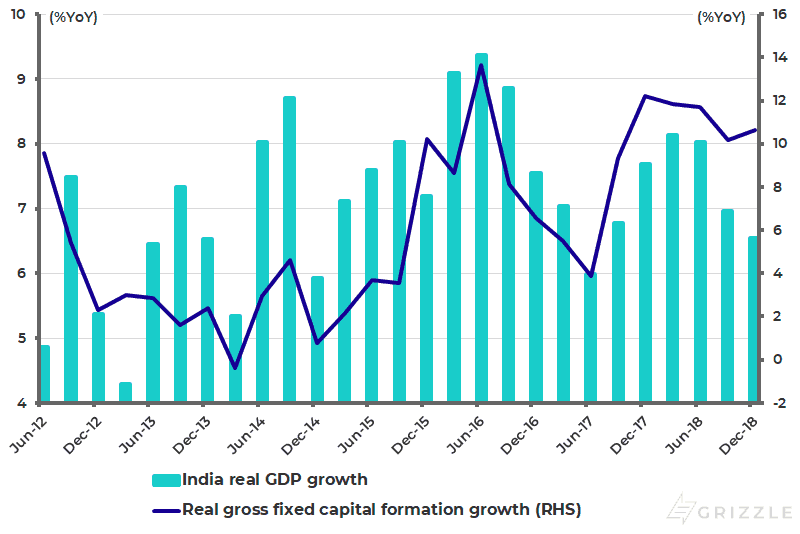

The general election will be held in the absence of clear cut evidence of an accelerating economic upturn. Indeed real GDP growth for 4Q18, at 6.6%YoY, was the weakest in 16 quarters aside from when GST was implemented on July 1, 2017 (see following chart). Still, the long-term dividends from the structural reforms introduced by Modi during the past five years will start to become visible in his next five-year term, assuming he is re-elected. And if he does not, his successor will reap the benefits.

India real GDP growth and real gross fixed capital formation growth

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.