The Fed duly delivered on its 25bp cut at the end of last month, the first monetary easing since December 2008. The issue now, of course, is whether this is an insurance cut or the beginning of an easing cycle. On this point, Fed Chairman Jerome Powell sensibly kept all options open at his post-meeting press conference, saying that the rate cut is a “mid-cycle adjustment” but adding: “I didn’t say it’s just one”. Needless to say, this was not appreciated by Donald Trump.

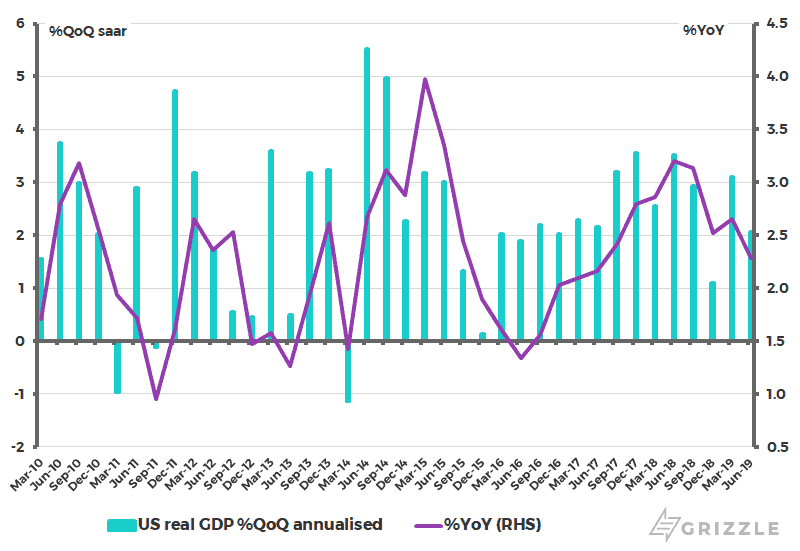

I stick with the view that this is the commencement of an easing cycle. Still it is the case that U.S. economic data is not, as yet, ostensibly that weak. The second-quarter data released in late July shows the U.S. economy slowing, as expected, to the trend growth rate of 2.3% YoY recorded since bottoming in 2Q09. U.S. real GDP rose by an annualized 2.1% QoQ and 2.3% YoY in 2Q19, down from an annualized 3.1% QoQ and 2.7% YoY recorded in 1Q19 (see following chart).

U.S. real GDP growth

U.S. Consumer Hanging In There For Now

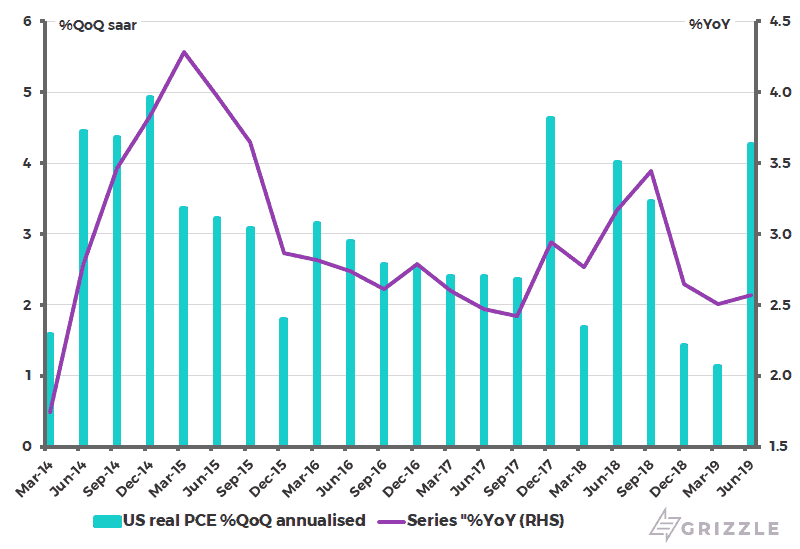

The main positive in the latest data was the relative health of the consumer with personal consumption contributing 2.9 percentage points to the 2.1% annualized real GDP growth. Still, it is worth noting that real personal consumption expenditure (PCE) has been decelerating in recent quarters on a year-on-year basis. Thus, U.S. real PCE growth slowed from 3.4% YoY in 3Q18 to 2.5% YoY in 1Q19 and was 2.6% YoY in 2Q19 (see following chart).

This is why if Donald Trump really went ahead with the second round of threatened tariff increases on the remaining US$300 billion of Chinese exports, it would be an undoubted negative for the American consumer. On this point, Trump announced at the start of this month to impose a 10% increase in tariff on the remaining US$300 billion worth of imports from China from Sept. 1; though he has lately moved to delay the tariff increase on about half of those imports to Dec. 15, including cell phones, laptops, and toys. Still the base case remains, despite the threats and bluster emanating from the White House, that this is not going to happen because of the obvious collateral damage to the economy in the run-up to next year’s presidential election.

U.S. real personal consumption expenditure (PCE) growth

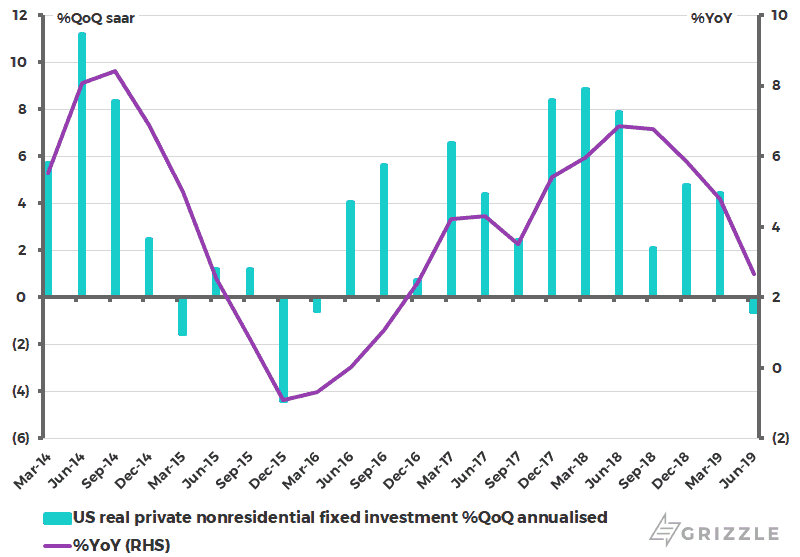

U.S. real private nonresidential fixed investment growth

Corporates Continue to Choose Buybacks over CapEx

Meanwhile the classic “beta” areas in the U.S. economy, in terms of what could swing America into recession, remain capital spending and housing. The CapEx data was again weak, suggesting the pickup last year was primarily driven by the 100% deduction allowed under last year’s tax reform. Nonresidential private fixed investment declined by an annualized 0.6% QoQ in 2Q19, the first decline since 1Q16. On a year-on-year basis, non-residential private fixed investment growth has slowed from 6.9% YoY in 2Q18 to 2.7% YoY in 1Q19 (see previous chart).

In this respect, it is ever clearer that the prime beneficiary of last year’s tax cut was the renewed surge in share buybacks, a process which continues to benefit the American stock market as corporates remain the main buyers of equities.

Annualized S&P500 share buybacks rose by 43% YoY to a record US$823 billion in the four quarters to 1Q19. The Fed’s flow of funds data also shows that non-financial corporates have repurchased a net US$3.9 trillion worth of U.S. corporate equities since 2009, compared with net purchases of US$1.7 trillion by mutual funds and ETFs (see following chart). Meanwhile from a CapEx standpoint, the capacity utilization rate remains relatively low while the continuing uncertainty on trade wars cannot be a positive for investment. The U.S. manufacturing capacity utilization rate was 75.4% in July.

Cumulative net purchases of U.S. corporate equities

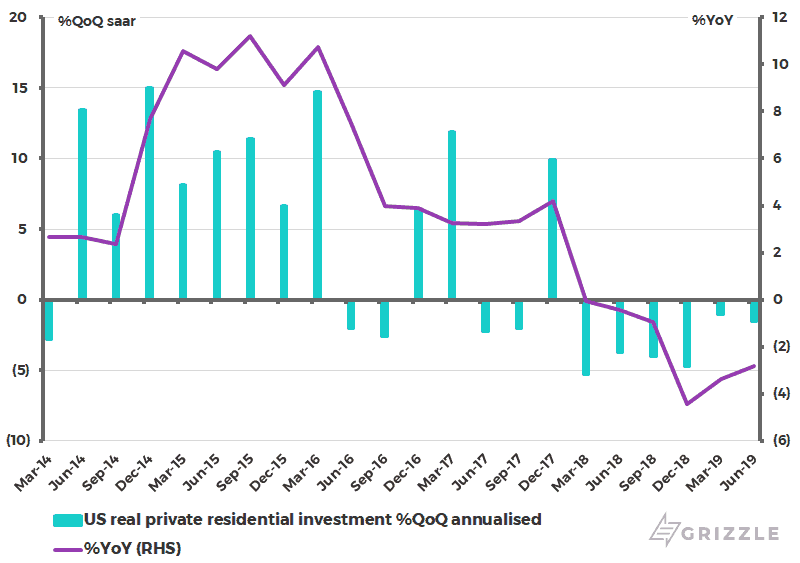

U.S. real private residential investment growth

Declining Mortgage Rates Should Provide Boost to Housing

What about housing? This has been slowing since late 2017 but should get some support from the Treasury bond market rally which has seen mortgage rates declining from 4.94% to 3.6% since mid-November 2018.

While residential investment remained weak in the last quarter, it makes sense to be prepared for a potential pickup in housing in coming months, for example in new and existing home sales. Real residential investment declined by an annualized 1.5% QoQ in 2Q19 and is down 2.8% YoY, the sixth consecutive quarter of decline (see previous chart).

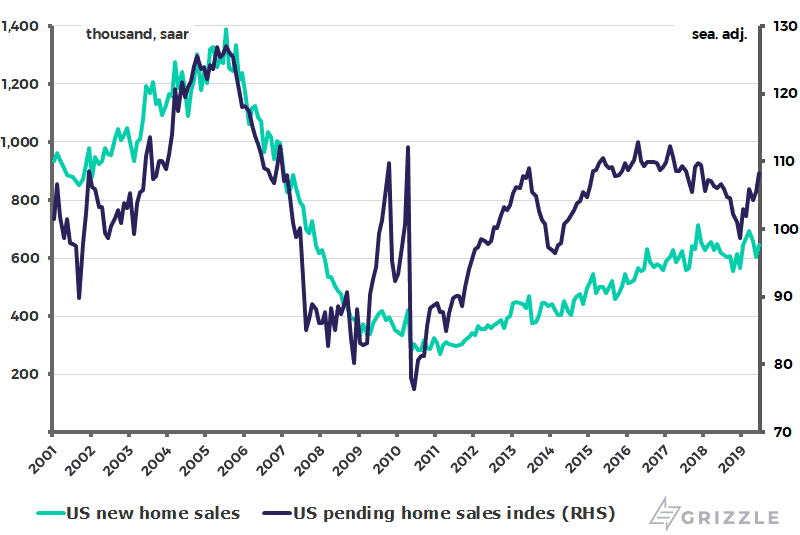

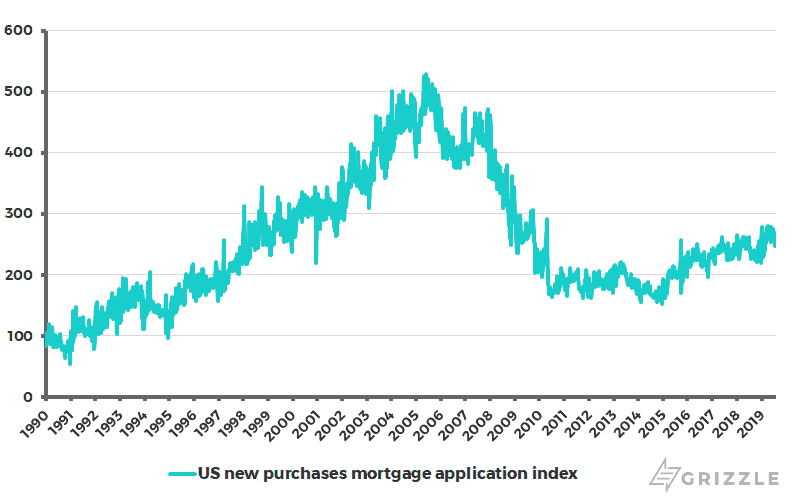

However, new home sales rose by 4.5% YoY in June and are up 16% from the recent low reached in October 2018. While the pending home sales index of existing homes rose by 1.6% YoY in June and is up 9.7% since bottoming in December (see following chart). It is also the case that new purchase mortgage applications have been rising year-to-date. The U.S. new-purchase mortgage application index has risen by 15% so far in 2019 (see following chart).

U.S. new home sales and pending home sales index of existing homes

U.S. new-purchase mortgage application index

Bet on the Fed Easing Cycle to Continue

If the American economic data is far from conclusive in terms of the recession risk, it remains the case that the main reason to bet on a continuing easing cycle is twofold.

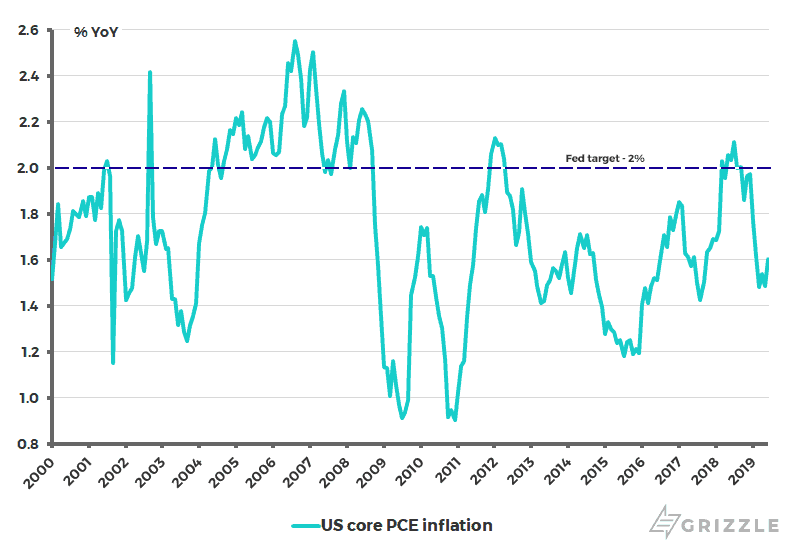

The first is that inflation remains below the Fed’s 2% target though of late there has been a marginal pickup. Thus, core PCE inflation slowed from 2.1% YoY in July 2018 to 1.5% YoY in May and was 1.6% YoY in June (see following chart).

U.S. core CPI inflation

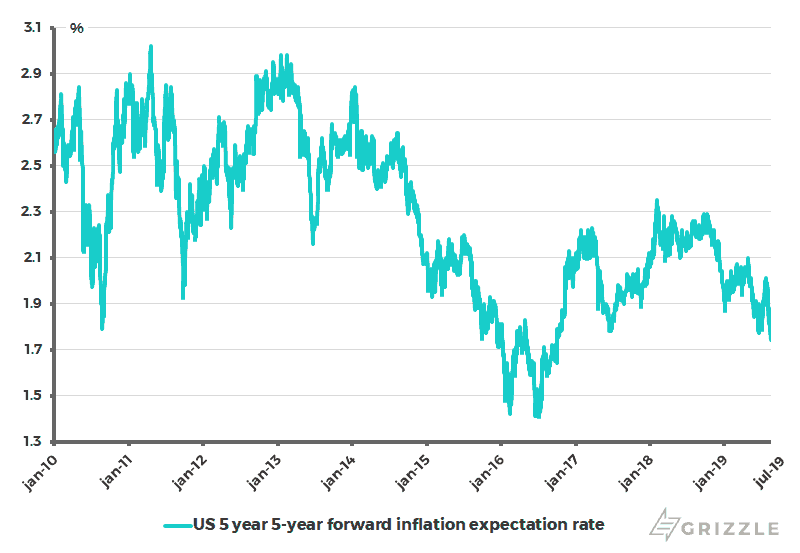

The second is the Powell pivot, the most dramatic Fed U-turn relative to the reported data I can remember, and the related surrender of intellectual leadership at the Fed by Powell to the Bernanke clones and the resulting renewed obsession with market-driven inflation expectations and the like. The 5-year, 5-year forward inflation expectation rate has declined from 2.29% in October 2018 to 1.74% (see following chart).

A reminder of this new dovishness was a speech made last month by New York Fed President John Williams. In a speech on monetary policy near the zero lower bound (ZLB) at the annual meeting of the Central Bank Research Association in New York on July 18, Williams said central banks should “take swift action when faced with adverse economic conditions” and “keep interest rates lower for longer”. He continued: “Don’t keep your powder dry… When you only have so much stimulus at your disposal, it pays to act quickly to lower rates at the first sign of economic distress.”

US 5-year, 5-year forward inflation expectation rate

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.