It is my view that cutting interest rates is not appropriate for fighting an epidemic.

But, unsurprisingly, this has not stopped the Federal Reserve cutting rates by 150bp to zero in 13 days as the evidence has accumulated of the Coronavirus hitting the U.S., in terms of both the rising number of cases and the rising impact on the American economy as more and more cities and states announce varying forms of lockdown.

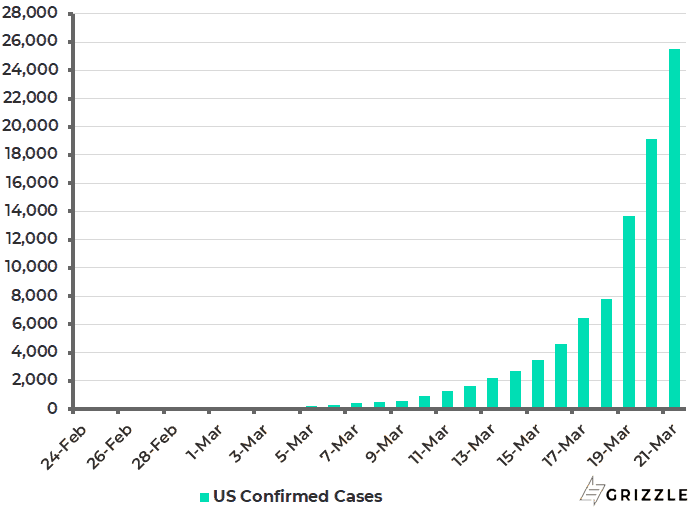

There are now 26,747 confirmed cases in America, up from 74 cases at the beginning of March.

U.S. number of Confirmed Coronavirus Cases

What Action Will the Fed Take With Coronavirus?

The question now is what further action the Fed takes.

It remains firmly the view here that the American central bank does not want to venture into negative rates. That is sensible on economic grounds. It is also the case that negative rates would probably be politically explosive in America.

Still this does pose the question of how it is possible to stop government bond yields being driven into negative territory by investors as has happened in Europe and Japan; though admittedly that process was encouraged by the Bank of Japan and the European Central Bank formally moving the benchmark rates into negative territory.

The most obvious way that is countered is by a more elaborate version of the Bank of Japan’s so-called yield curve control where the central bank targets yields at longer-term maturities, as the Fed also did during World War II.

Other options include renewed quanto-easing in the form of the Fed’s purchase of mortgage-backed securities where yields, unlike Treasuries, are still substantially above zero, with average agency MBS yields running at 2.28%. And the Fed has duly made such an announcement.

Thus, the Fed announced on March 15 that it will increase its holdings of Treasury securities by at least US$500 billion and its holdings of agency mortgage-backed securities by at least US$200 billion over the coming months.

On this point, the Fed is limited in terms of the sort of securities it can buy since it is, from a legal perspective, not meant to buy risky assets such as corporate bonds.

But that can always be changed by legislation if the market panic continues, which is quite likely so long as the number of infections keeps rising.

Will Fiscal and Monetary Policy Combine?

The Coronavirus is also likely to prove the catalyst for more central banking direct financing of government where fiscal policy and monetary policy are effectively combined.

I have been arguing over the past year and more that, with America likely to eschew negative rates, the direction of travel is towards some version of Modern Monetary Theory (MMT) when America next enters a downturn.

Now the Coronavirus has caused the downturn to become reality with the only issue how long it lasts.

The problem is that MMT, advocated as it has been by people on the political left such as Bernie Sanders’ economic adviser Stephanie Kelton, looks scary to investors since its supporters are essentially arguing that the authorities can print as much money as they like so long as there is no inflation, thereby justifying unlimited government spending on social programs and the like.

This is why there is a need to fashion a policy approach that would amount to a more acceptable form of MMT which is less likely to scare markets.

The most imaginative effort I have seen so far to come up with a more respectable framework for central banks to finance government directly, without the process degenerating into crude MMT, was contained in a paper published by the BlackRock Investment Institute last August (“Dealing with the next downturn: From unconventional monetary policy to unprecedented policy coordination”, Aug. 15, 2019).

The paper proposes a so-called “monetary-financed fiscal facility”.

What does this mean?

To quote from the paper directly: “Activated, funded and closed by the central bank to achieve an explicit inflation objective, the facility would be deployed by the fiscal authority.”

The paper’s authors, whom it should be noted include former Fed Vice Chairman Stanley Fischer and former Swiss National Bank head Philipp Hildebrand, argue that such an approach will likely involve “going direct” in the sense that it will put central bank money directly in the hands of public and private sector spenders.

The paper also proposes that the “standing emergency fiscal facility” would be permanent and would be activated whenever monetary policy is tapped out, as is effectively the case now, and when inflation is expected to undershoot, and clearly inflation expectations have collapsed again relative to the Fed’s target.

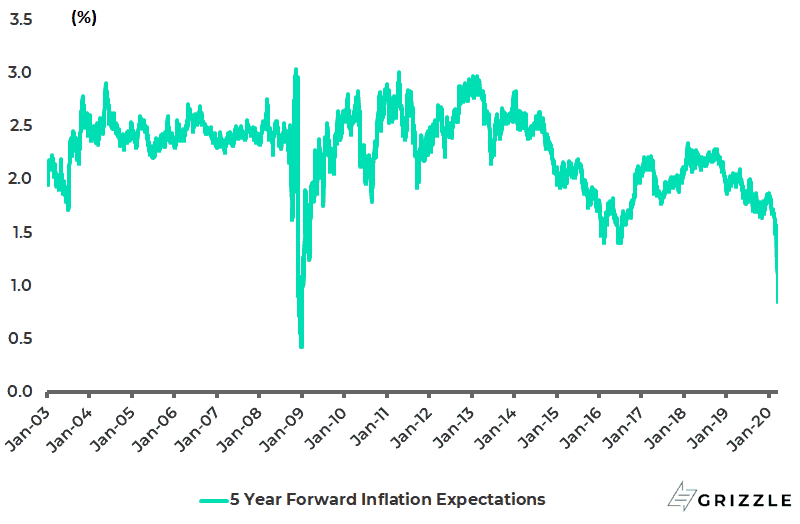

The five-year forward inflation expectation rate has declined from 1.86% at the end of 2019 to 0.86% on March 19, the lowest level since January 2009, and is now 1.19%.

U.S. 5-year Future Inflation Expectations (5 Years Forward)

The BlackRock paper seeks to distinguish such an approach with more extreme forms of “going direct”, by which it means permanent monetary financing of fiscal expansion which is essentially what MMT recommends.

Remember that MMT amounts to an effective merging of monetary and fiscal policy.

[su_panel]The authors note that “without explicit boundaries” a merging of monetary and fiscal policy would undermine institutional credibility and could lead to uncontrolled fiscal spending.[/su_panel]I agree.

This is why the formal adoption of MMT would probably mark the beginning of the end of the bull market in Treasury bonds which has been in place since 1981.

In this sense, the authors of the BlackRock paper are at pains to stress that their proposal is “in sharp contrast” to the case argued by proponents of MMT since it is “limited to an unusual situation – a liquidity trap – with a predefined exit point and explicit inflation objective”.

While this would certainly be formally the case a skeptic would argue that the exit point might never be achieved nor the inflation target, which could mean that the policy might end up being permanent and therefore in practical terms the same as MMT.

Still there is no denying that the BlackRock paper amounts to a clever effort to make central bank direct financing of government more intellectually respectable.

For that reason, and also for the impeccable establishment connections of its authors, it could well be the direction in which Fed policy ends up going.

Still, it should also be noted that the authors argue that the effectiveness of such a policy framework would depend on whether it is implemented well in advance of the next downturn.

For this would increase the chances of the framework being understood and accepted by markets.

The problem here of course is that the Coronavirus may not allow the luxury of such advance timing given its already proven propensity to trigger panic selling.

Looking Forward

In this respect, the best hope for the virus remains that it is seasonal, like the flu, in which case the markets are facing probably only two more months of panic selling before the weather turns warmer in the northern hemisphere.

Even on the former more sanguine assumption, the base case is also more panic selling because the evidence to date points, unfortunately, to the fact that Western democracies are really not equipped to deal with this sort of thing.

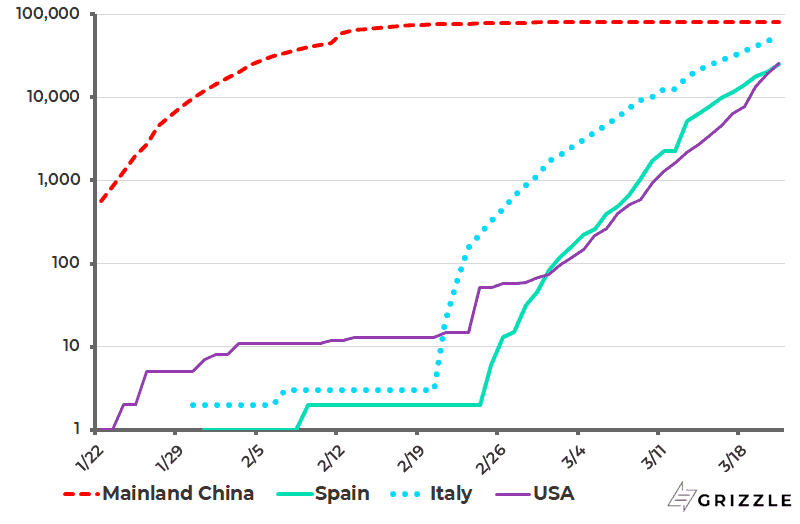

The case of Italy, which is increasingly looking like a healthcare disaster almost as bad as Wuhan in China, has clearly raised the issue of whether Western healthcare systems can cope.

The total number of confirmed cases in Italy is now 53,578 cases, compared with 81,054 cases in mainland China but the number of deaths in Italy is higher.

While there are 4,825 deaths in Italy, compared with 3,261 in mainland China.

In this respect, it increasingly appears that the virus itself is less of an issue than the adequacy, or lack of it, of the healthcare infrastructure.

This is why epidemiologists argue that the key goal is to try and slow the speed of infection out over time both to give healthcare systems more time to cope and also, hopefully, to come up with a vaccine.

While the total number of infections should also end up lower. This is what is called “flattening the curve”, giving a new meaning to that term.

Cumulative number of Coronavirus Cases in mainland China, Spain, Italy and the U.S. (log scale)

Meanwhile, China’s success in controlling the spread of the virus was the result of drastic measures where public health was put before economic activity.

Such drastic measures have now been introduced in Western Europe over the past week and more are now being implemented in America.

Still, the problem right now is that the Western world lost precious time not preparing, in terms of not learning the lessons from China on how to deal with the Coronavirus.

This means that the next few weeks will likely see a continuing scary rise in infection rates.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.