Netflix Inc. (NASDAQ: NFLX) has posted their earnings for Q1 2020.

Revenue came in at $6.05B which beat analysts’ estimates of $5.746B

EPS was $1.81 beating analysts’ estimates of $1.64 by 10%.

[su_panel background=”#d1cef4″ radius=”7″]The strong subscriber growth will likely push the stock higher tomorrow as Netflix remains the king of streaming.[/su_panel]

Netflix is known as the king of the “stay at home” economy. Even before the crisis, Netflix was already an existential threat to the movie theater industry and this crisis has only extended Netflix’s advantage as movie theaters are completely shutdown and literally bringing in zero revenue.

As a result, in contrast to most other companies that are seeing their stock decline due to deteriorating fundamentals and fears of a recession, Netflix has none of those problems and the stock is now at all time highs of over $430/share at the time of this writing.

Subscriber Growth Is The Name Of the Game

Last quarter we saw that US domestic growth of new subscribers were almost completely flat, coming in at only 0.7% increase over the previous period, ending the quarter at about 67M US domestic subscribers.

The number for international subscriber growth was far more impressive last quarter, coming in at 106M or 8.4% growth over the previous quarter.

If Netflix can continue to grow subscribers at high rates, then perhaps it can justify some of its incredibly high valuation, but Netflix does have its fair share of competition coming in hard and fast.

The Rise of Disney+, Amazon Prime Video, And Apple TV+

Although so far it seems like Disney+ and Apple TV+ pale in comparison to Netflix, the competition does appear to be catching up.

Disney+ announced earlier this month that it has exceeded 50M subscribers. Although the entirety of Disney+ subscribers base is still smaller than just the US domestic segment of Netflix, the growth rate of Disney+ has been rather impressive.

Back on February 4, 2020, Disney had only reported 26.5M subscribers in its earnings report. So, Disney has almost doubled their subscriber count in less than one quarter.

Although of course this mostly had to do with the coronavirus situation forcing people to stay home, but it would be interesting to see if after the lockdown is lifted if people will cancel their subscriptions or decide to keep it.

At the same time, Apple and Amazon are also pushing hard into the streaming space as well with the launch of their Apple TV+ service and Prime Video service respectively, which both feature exclusive shows.

According to a report this past January, Apple TV+ and Amazon Prime Video subscribers come in at around 33.6M and 42.2M subscribers respectively.

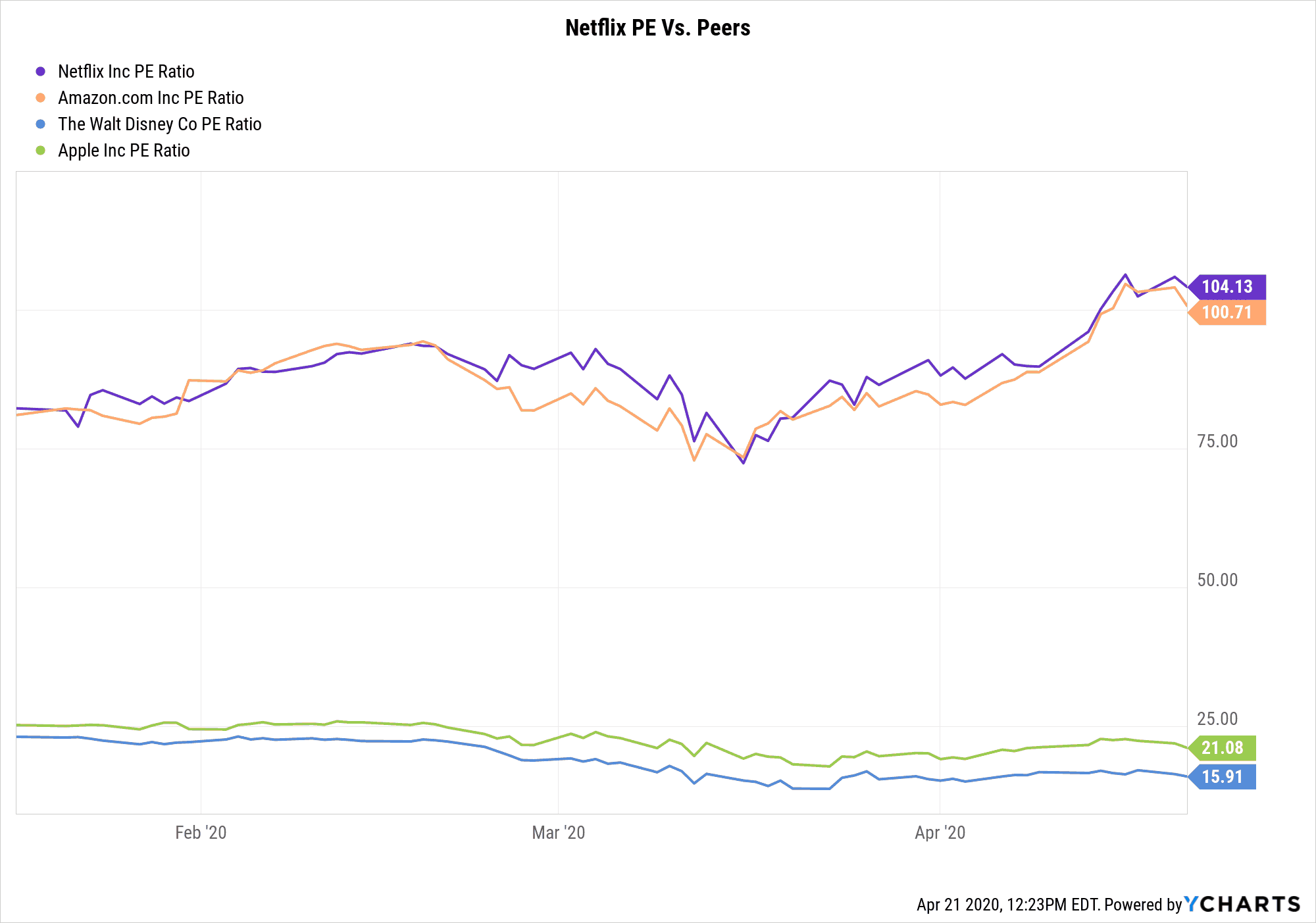

Valuation

Comparing valuation to other companies, we see that Netflix is not cheap, the recent huge surge in stock price has put its trailing PE at over 104, just a hair over that of Amazon which also recently hit all time highs.

However, investors should keep in mind that Amazon only dabbles in video streaming and its bread and butter still comes from its Amazon Web Services and online e-commerce operations.

So holding Amazon stock is a play on its myriad of different business segments while if one were to buy NFLX, it would be more of a pure play on streaming.

What might be slightly concerning for Netflix from a longer term perspective is the fact that Netflix remains a one trick pony.

Competitors like Apple, Disney, and Amazon all have their other areas of the business which they can leverage to create an ecosystem which locks in the customer.

For example, Amazon has their Prime service which includes Prime Video but also bundles in other benefits.

Apple has their own software ecosystem that is notoriously sticky in the minds of consumers many of whom are already using Apple devices.

And Disney with their acquisition of LucasFilms and Marvel now has a treasure trove of intellectual property that would be hard for Netflix to supplant.

Although Netflix’s growth and business is impressive, and one should definitely avoid betting against the stock since it may very well roar higher, it hardly puts out a compelling case why anyone should rush in to buy this stock at these levels.

But Netflix definitely would be an interesting stock to watch in the near future and (for now) remains the King of Streaming.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.