Nike reported its fourth quarter fiscal 2020 results ended in May post market on June 25th that disappointed Wall Street’s expectations, causing shares to trade lower after hours.

The company generated $6.31B of revenue, below analyst estimate of $7.3B by 13%, and was down by 38% year over year.

Nike reported a net loss of $754M, which was lower by 180% year over year.

As a result, loss per share was $0.51 which missed consensus estimate of $0.14 by a whopping 64%.

The company disclosed its EBITDA loss of $754M, which was also lower than the street estimate by 403%, and down by 160% year over year.

The company also reported that at May 31st they had $12.5 billion in total liquidity including $8.8 billion in cash, and short term investments, thanks to the issuance of a $6 billion corporate bond.

Since then, Nike has also secured a new $2 billion credit facility its addition to its existing facility of $2 billion to enhance its durability in the midst of the pandemic.

COVID-19 Impact

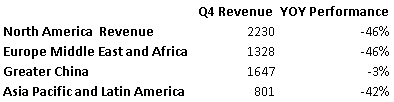

Due to the pandemic related store closures globally, revenue segments in each international markets excluding Greater China, were impacted significantly as shown below.

Greater China revenue was mostly immune to the virus setbacks since nearly most of its stores still remained open.

However, Nike management stated that the company experienced a 75% increase in its digital sales, which roughly contributed 30% to the total revenue in the fourth quarter.

Yet inventory increased by 31% year over year as widely expected.

As stated by Nike CEO John Donhoe, “During the widespread physical store closures, we accelerated our connection and engagement with our consumers leveraging the strengths of our digital ecosystems”.

This could perhaps indicate the beginning of a new trend where the sector like most others are now investing more into their online infrastructure which would ultimately lead to many brick and mortar stores being downsized.

In the meantime, the company’s management stated that they have now reopened approximately 90% of the stores across the globe with reduced hours, and retail activity is picking up week over week with higher conversion rates year over year.

Regardless of the negative impact on the company’s financials, store reopening operations by the company like most of its peers in the sector have restored optimism amongst investors.

Additionally, the company has largely maintained its share repurchase activity, and cash dividend payments too, which further contributed to the recovery of its share price back to its pre pandemic levels.

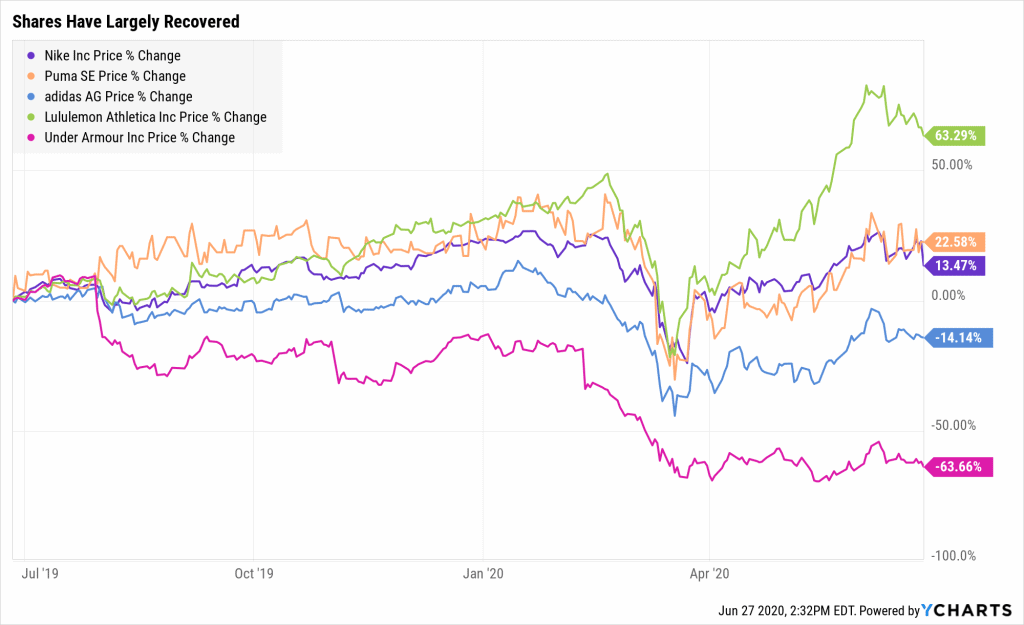

As shown, Lululemon has recovered much more than Nike since the March bottom, even though it does not pay any shareholder dividends. This is primarily due to the fact that the company has a more favorable EBITDA margin than its peer.

LULU’s debt to EBITDA margin is better as well.

According to Lululemon’s recent earnings report for the quarter ended on April 30th, it earned a positive EBITDA of $76 million which meant the company had a margin of 11.7%.

The company also has a much tighter float of 124.8 million shares too, which is around a billion shares less than Nike.

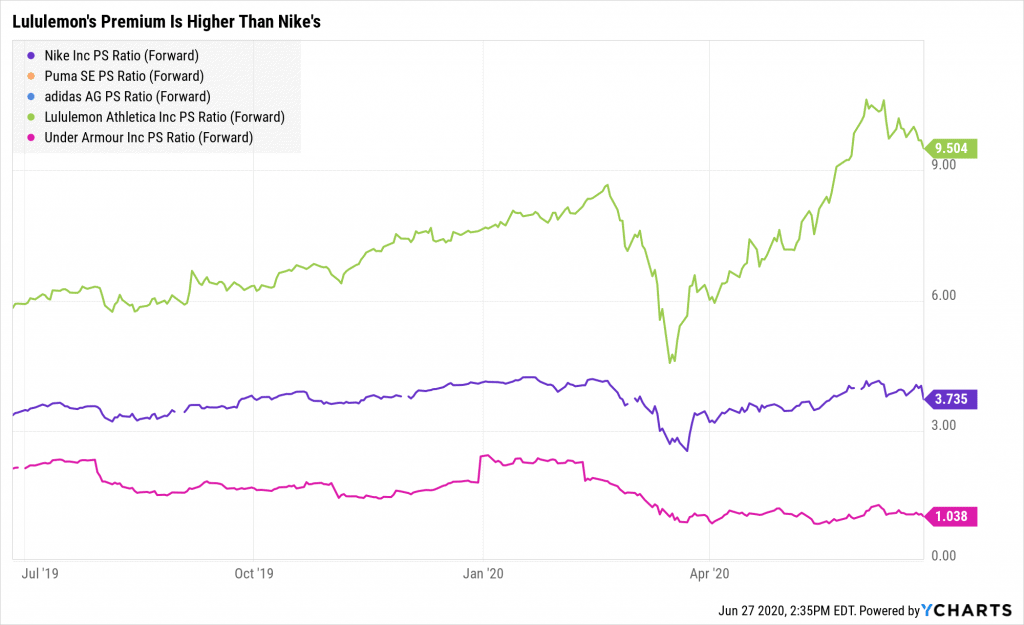

These factors are reflected on the following chart where Lululemon’s PS ratio is much higher than Nike’s.

However, one should keep in mind that Lululemon’s recent earnings does not include the month of May, and it consist of sales incurred in the month of February which was a month before the pandemic lockdown kicked into full gear.

As a result, the company’s share price should be viewed with caution till the next quarter performance provides a clearer view of its impact by the virus.

Final Remarks

Although Nike experienced heavy setbacks, it managed to salvage some of its revenue thanks to online sales.

However as more stores have begun reopening, some may be downsized as the company continues to rely and invest on its online infrastructure more than ever before.

The company also has ample liquidity to survive the pandemic, but its negative cash flow as suggested by its negative EBITDA certainly presents a daunting challenge for the company to pay back its debt in the here and now.

Where the stock goes from here will all depend on if the U.S. has to shut retail stores due to a second wave and also how quickly management can ramp up online sales to make up for the huge loss in in-store purchases.

Given the price/sales multiple is close to pre-pandemic levels, we think the stock will struggle while the virus continues to float around the developed world.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.