Nike (NYSE:NKE) posted their earnings report today for Q3 2020.

Revenue came in at $10.1 billion which beat analysts’ estimates of $9.57 billion.

EPS was $0.53 which missed analysts’ estimates of $0.56, but this includes a $0.25 per share non-cash and non-recurring expense related to the transition to a strategic distributor model in South America.

During a crisis like this, entertainment and travel industries tend to be hit the hardest. You may not immediately think of Nike as being in the entertainment industry, but the company’s operations in sports sponsorships and sports marketing is a core area of the business as well as their direct-to-consumer sales of products.

With retail stores shut down and all major sports games cancelled, it’s a bad time to be a Nike shareholder.

Nike vs. COVID-19

Although the true impact of the COVID-19 coronavirus in North America will not be reflected on this report, we can already get an indication of how much negative impact it has had on Nike’s business in China.

The consensus EPS estimate for Nike for this quarter has seen 19 downward revisions and 0 upward revisions throughout the past 3 months and represents a 19% year-over-year decline.

However, perhaps it’s not all doom and gloom, due to Nike’s powerful brand and reach, the company may have a significant advantage on online sales compared to many other competitors. In a bid to boost sales, the company has already given a 25% price cut on many of its products like footwear.

Analysts have not totally given up on Nike, in an interview with Yahoo Finance, Raymond James analyst Matthew McClintock stated that:

Taking a look at the balance sheet, Nike has plenty of cash on hand and should be able to weather the storm if we were to sink into a long term recession. Currently the company has about $3.5 billion in cash which is more than half their total debts, with a current ratio almost 2.

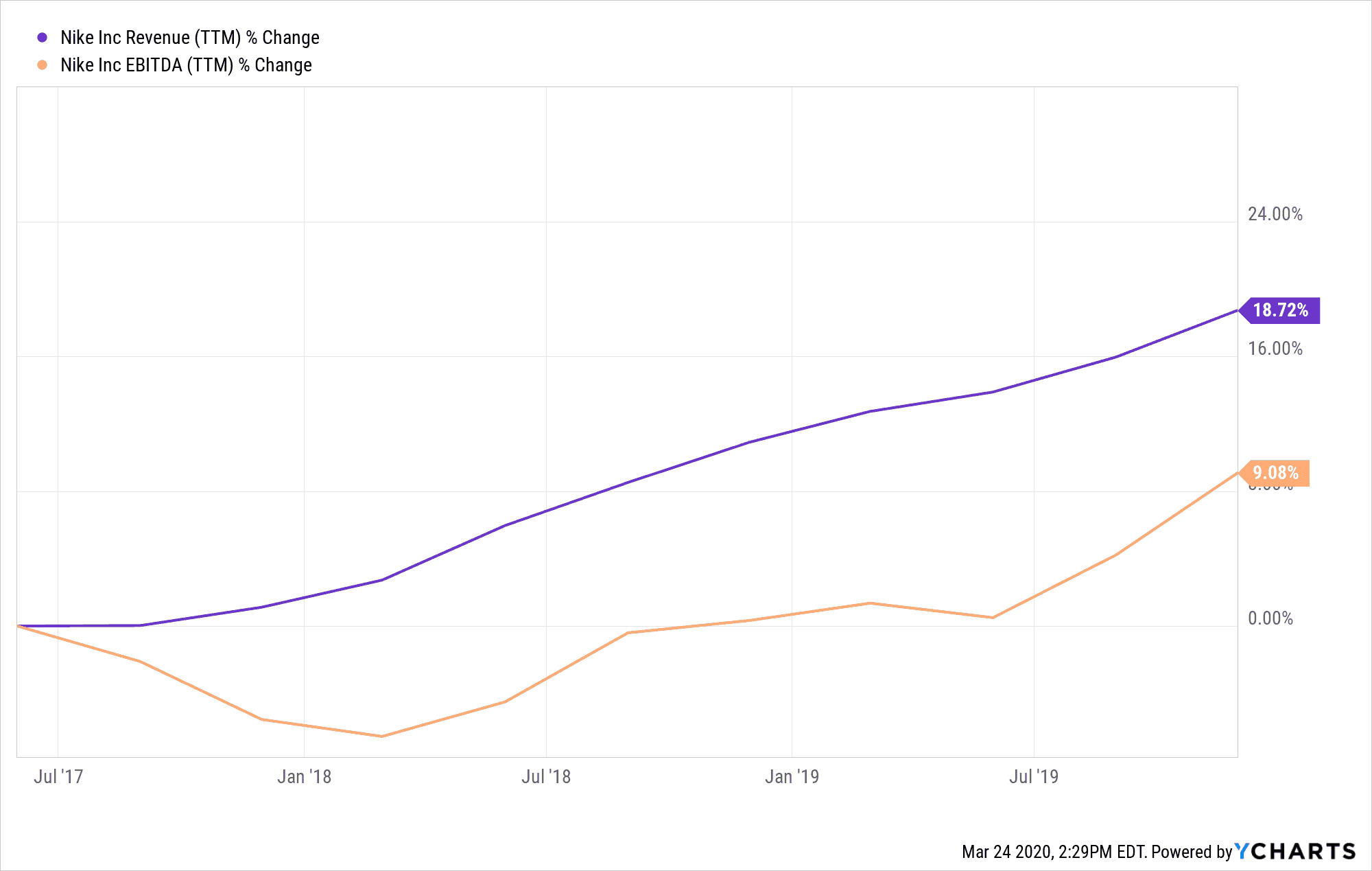

Taking a look at Nike’s past fundamentals, on a trailing 12-month basis, Nike’s revenue and EBITDA growth rates have been pretty impressive. Although in the near term they will surely drop due to the virus, it is very likely that once the outbreak is over that Nike will be able to quickly return to their trajectory of growth.

Bottom Line

From a long-term perspective Nike seems like a good bet for prospective investors who want to buy into this recent stock market crash.

The brand remains strong and Nike’s dominance and reach are still largely unaffected by the virus. The company has a good balance sheet and should be able to weather the storm of the upcoming recession.

In the short term though, investors who pour money into this stock should not expect for it to perform well since sports games and retail stores all across Europe and North America will remain closed for the foreseeable future, which heavily impacts Nike’s business.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.