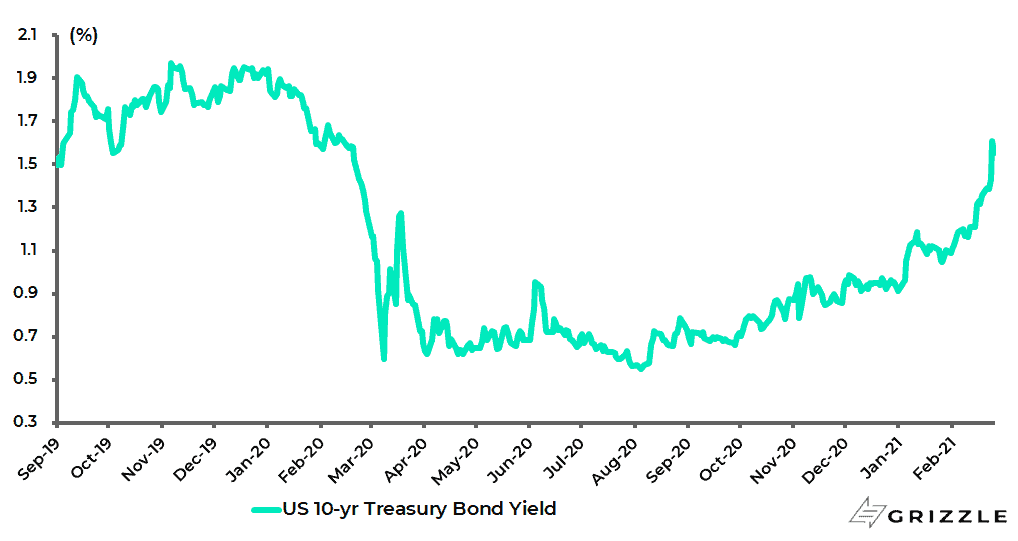

The benefit of the doubt continues to be given to the cyclical trade, which also continues to be confirmed by the continuing sell-off in the Treasury bond market with the 10-year Treasury bond yield now at 1.72%, the highest level since January 2020.

US 10-year Treasury Bond Yield

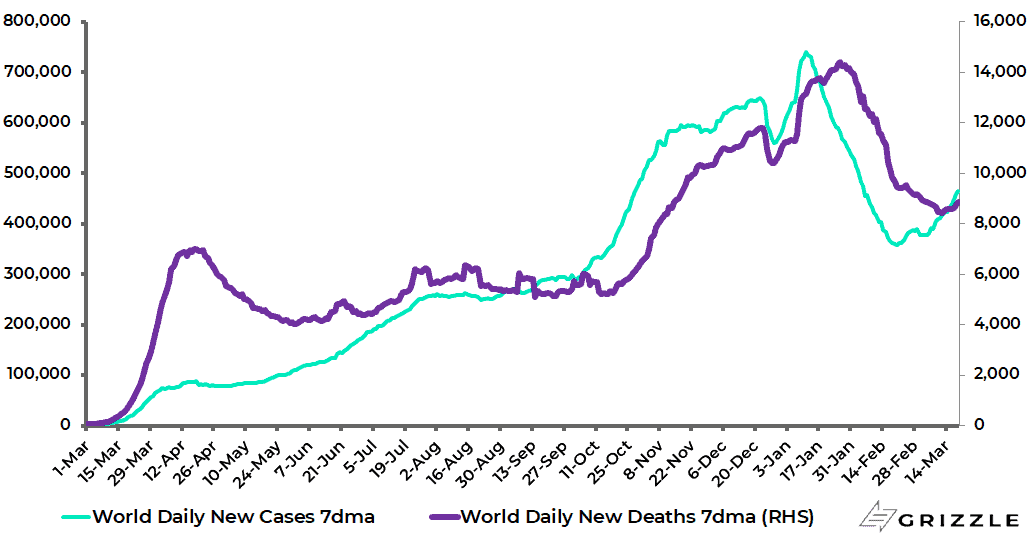

Meanwhile, with global Covid cases having declined significantly from the peak amid the ongoing vaccine rollout, the biggest risk to that trade remains the efficacy of vaccines against new variants.

The 7-day average daily new Covid case count globally has declined by 37% from the peak of 739,564 reached on 11 January to 465,025. While the 7-day average daily Covid death count globally is down 39% from the peak reached in late January.

World 7-day Average Daily New Covid Cases and Deaths

Dovish Fed Comments Keeping the Market Happy…For Now

In the context of the continuing yield curve steepening, the US stock market has been relieved to hear this week continuing doveish noises coming out of the Federal Reserve.

This is in the face of economists in recent months competing to upgrade their forecasts for 2021 US real GDP growth.

Consensus forecasts for US 4Q21 real GDP growth have already been upgraded from 3.5% YoY in December to 6% YoY with more upgrades on the way.

The Fed has itself got in on this act raising its 4Q21 real GDP forecast on Wednesday from 4.2% YoY in December to 6.5% YoY.

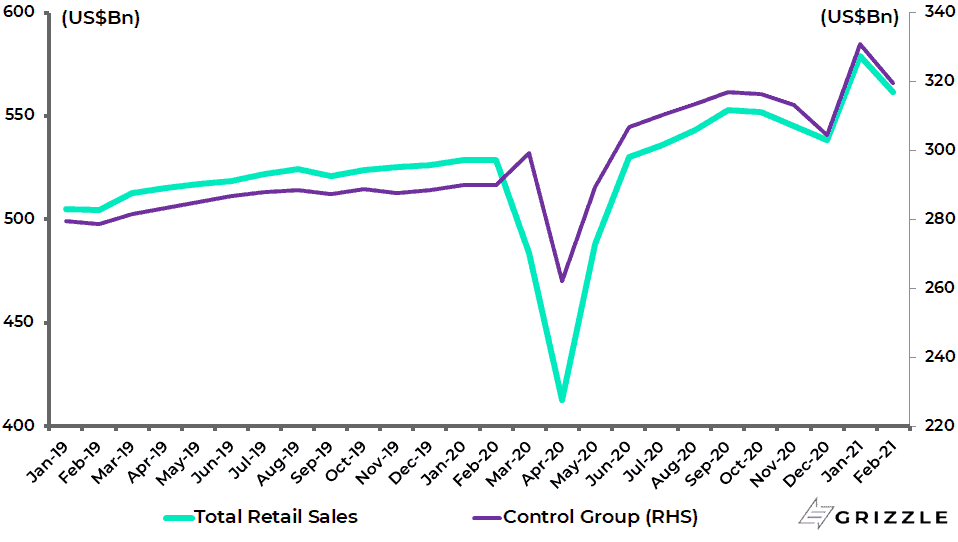

Reasons for the upgrades cited have been growing expectations of speedy implementation of the Biden administration’s US$1.9tn Covid relief stimulus, as well as very strong US retail sales data in January even though it weakened somewhat in February due to inclement weather.

US retail sales rose by 7.6% MoM and 9.5% YoY in January with so-called “control group” sales, which exclude food services, gas stations, auto dealers and building materials, surging by 8.7% MoM and 14.1% YoY.

US Retail Sales

This is the sub-set of retail sales that feeds directly into the GDP and personal consumption data.

Indeed the US Treasury Department reported last week that the first tranche of about 90m stimulus cheques have already been disbursed as of 17 March.

The strong retail sales data has served as a reminder of the pent up demand potential coming out of the pandemic which, as already noted, will only be further stimulated by the additional US$1,400 stimulus cheques now being sent in tranches to American households as part of the US$1.9tn Covid relief stimulus signed into law by Joe Biden on 11 March.

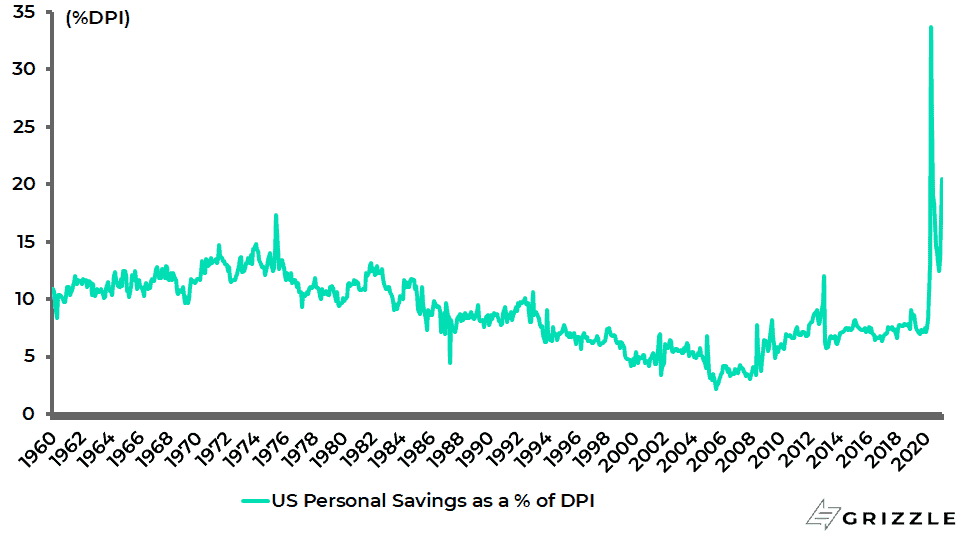

The US household savings rate was already at an elevated 20.5% in January, based on the latest data, thanks to lockdowns and increased transfer payments.

US Personal Savings as % of Disposable Income

Despite all of the above, the Fed is for now sticking with its mantra that the near-term pickup in inflationary pressures will prove to be transitory.

That said if Fed Chairman Jerome Powell is looking for an excuse to engage in another pivot, which at present he clearly is not, the Biden administration’s US$1.9tn fiscal package, on top of the anticipated up to US$2tn infrastructure package later in the year, gives him a seemingly plausible way out.

For he can argue that fiscal policy is now doing the “heavy lifting”.

Still there is, for now, no sign of a change in language or approach from Powell.

Rather the current US policy regime, labelled by one wag as the Jay and Janet show, remains super easy in terms of both monetary and fiscal policy.

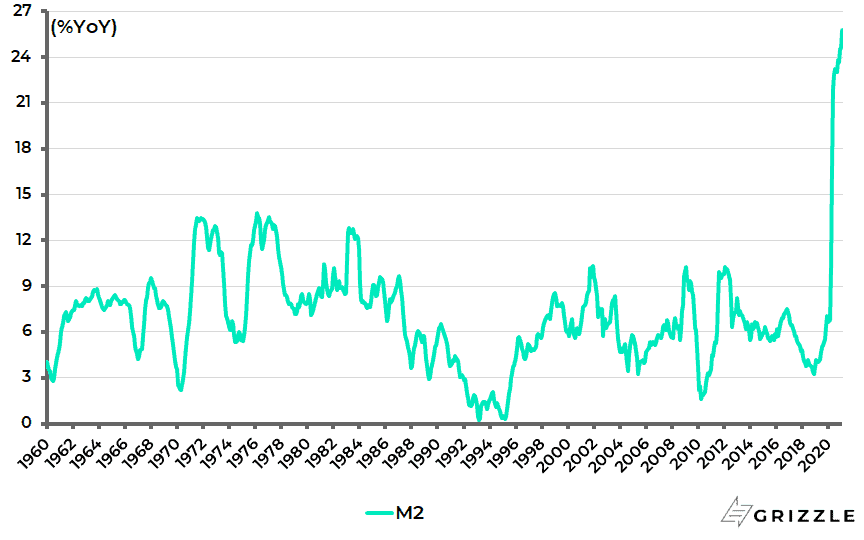

In this respect, it is not necessary to be a hardline monetarist to be astonished by Powell’s statement to Congress last month that “the growth of M2 … doesn’t really have important implications for the economic outlook”.

This is a statement he may well come to regret.

Remember that US M2 growth surged to 25.8% YoY in January, the highest YoY growth rate since the data series began in 1959.

February data is due to be released on Tuesday. Back in the late 1970s/early 1980s, markets and the Fed obsessed about money supply data.

Now economists do not even have forecasts for money supply growth. Nor does the Fed.

US M2 growth

Source: Federal Reserve

Consensus Believes No Taper Until Early 2023

Maybe it will work out that way.

Still, the real issue for this writer is less the economic data than the market action, most particularly in terms of Treasury bond yields and market-driven inflation expectations.

For experience has long since demonstrated that the Fed is moved by markets, and not the other way around.

This is why the more cyclical stocks rally, and the more the Treasury bond market sells off, the more pressure will build on the Fed to acknowledge the reality that policy is way too easy.

The other critical point, of course, remains whether the doves on the Fed will seek to short circuit this process by pegging bond yields via yield curve control.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.