After bracing shareholders for disappointment last month, Nvidia (NASDAQ: NVDA) released their fiscal Q4 2019 earnings this evening and they were in line with the lowered expectations. Revenues for the chip maker were down almost 31% over the previous quarter and 24% year over year but aligned closely with the guidance provided in January. The company did, however, record earnings per share in Q4 FY19 of $0.80 compared to consensus estimates of $0.77 pre-earnings.

With Nvidia stock closing at $154.53 today but up to $163.00 in after-hours trading as of the time of publishing, the company’s stock appears to have weathered the storm of their poor quarterly results. Some analysts cut their price target for the company based on the company guidance provided in January but with the company slightly beating expectations price targets are likely to creep slightly higher over the short term.

Primary Factors in the Nvidia Q4 2019 Earnings

The Nvidia Q4 2019 earnings showed losses in revenue across all of the companies markets with their largest market, gaming, taking the biggest hit in revenues down 46% over the previous quarter. Nvidia recently released a new generation of gaming cards incorporating ray-tracing technology to make games more realistic.

However, sales of the new cards have lagged expectations due to a lack of games that support the technology and higher retail prices for the high-end equipment. According to the company, the gaming market was also hurt by the macro issues facing the Chinese economy, which is a prime region for gaming.

Nvidia also blamed macro issues for the decline in data centre revenues as it said several potential deals did not close due to caution from customers over economic uncertainty.

While the company had already discounted cryptocurrency-related revenue to be “no longer meaningful” in its Q2 2019 results, it is still feeling the after-effects of the collapse of that market. Excess channel inventories of GPUs still left over from the crypto boom have caused the company to delay production to allow the excess inventory to be sold.

The poor quarterly numbers did dampen what has overall been a very productive year for the company. Revenues across almost all markets were up significantly year over year with growth in data centre and auto revenues being particularly impressive given the continuing trends of computing moving towards cloud-based applications and autonomous vehicles. Data centre revenue accounted for 25% of FY19 revenues for the company compared to 20% the previous year.

Nvidia Quarter over Quarter and Year over Year Revenues by Market

| Q4 FY19 / Q3 FY19 | FY19 / FY18 | |

| Gaming | -46% | +13% |

| Professional Visualization | -4% | +21% |

| Data centre | -14% | +52% |

| Auto | -5% | +15% |

| OEM & IP | -21.6% | -1% |

| TOTAL | -31% | +21% |

Nvidia’s Competitive Landscape

Given the slowdown in gaming revenues for its Q4 2019 earnings, it appears as though AMD is beginning to eat into the estimated 74% market share enjoyed by Nvidia. Latest technology of GPUs are priced high (ray tracing) and AMD may be eating into Nvidia’s estimated 74% market share. Whether or not Nvidia can regain some of those losses depends on two factors:

- Can the high-end ray-tracing technology gain market traction as more content is released to support it?

- Will mid-tier products released in January whose entry to market was delayed to clear the excess crypto inventory fill a market need without price cuts.

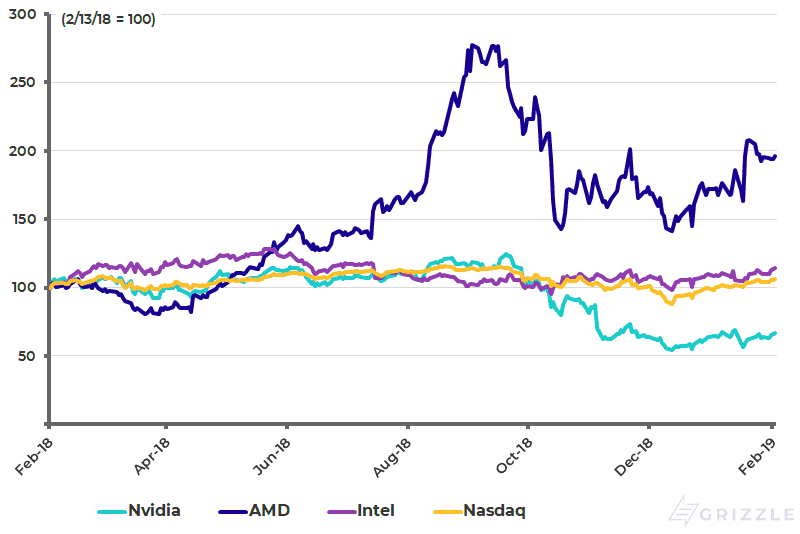

Nvidia stock is down 46% since its peak at the beginning of October 2018, whereas its primary competitor AMD has surged this year and is up 100% over the past year. Compared to more general chip manufacturer, Intel, and the the overall Nasdaq composite which have been primarily flat over the past year, Nvidia has also underperformed.

Nvidia Performance Comparison over the Past Year

What’s in Store for Nvidia in the coming year?

While Nvidia Q4 2019 earnings were disappointing, there are still growth opportunities for the company. Artificial intelligence (AI) is increasingly an area of computing needing intensive processing power and Nvidia has found traction in data centre GPUs. The automotive segment also continues to be a growth opportunity as more and more Tier 1 automotive suppliers such as Bosch and Continental incorporate Nvidia products into systems for autonomous vehicles. Finally, Nvidia’s mid and high-tier gaming products offer ray-tracing, a market expected to grow 54% a year over the next 5 years.

Nvidia’s forecast for 2020 is decidedly conservative with the company predicting FY20 revenues to be flat to down slightly. One wonders if the management is once again setting lower expectations in order to outperform their forecasts over the coming year.

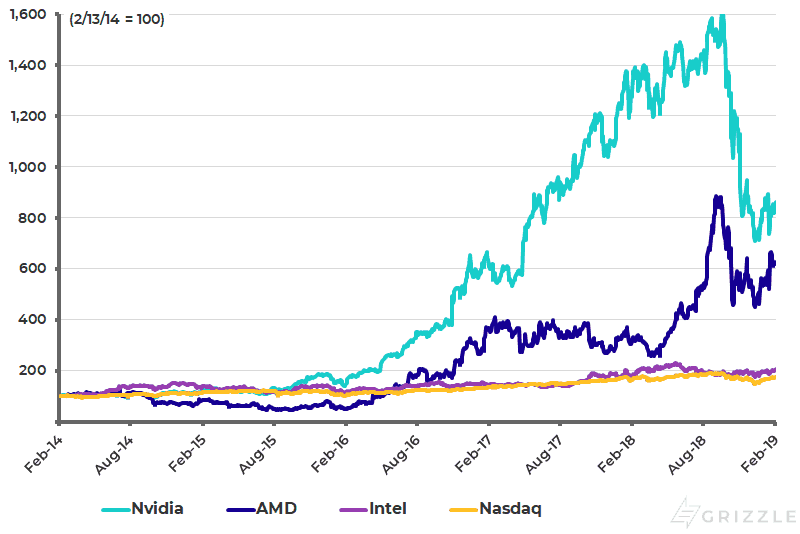

Given the incredible run the stock has seen over the past 5 years up until it’s peak in October 2018, there could be plenty of room to run for a stock which is currently trading at a 23x PE ratio compared to its biggest competitor AMD at a 72x PE ratio.

Nvidia Performance Comparison over the Past 5 Years

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.