Organigram Inc.(NASDAQ: OGI) (TSX: OGI), released their third quarter fiscal 2020 earnings and there was very little to like.

The company saw revenue decline in a growing market, wrote off tons of inventory and has to rebrand the value product most important to their future.

The license producer generated $18M of revenue, above analyst estimate of $15M by 20%, but lower by 27% year-over-year.

The company’s EBITDA however came in at a negative $5M after adjusting out the one time write-offs , which was much lower than analyst expectations of almost zero EBITDA.

Organigram had a huge writedown of inventory showing that the industry is wildly oversupplied and not every gram grown can currently be sold.

The company cut headcount by 25% which is needed to match falling revenues with costs, but they had to take an additional charge for the reduced headcount which hurt earnings.

While the staff reduction led to lower revenues, their increased focus on higher margin edibles sales and the introduction of their new value brand, Trailer Park Buds helped offset some of the losses as discussed below.

Price Valuation and Revenue Woes

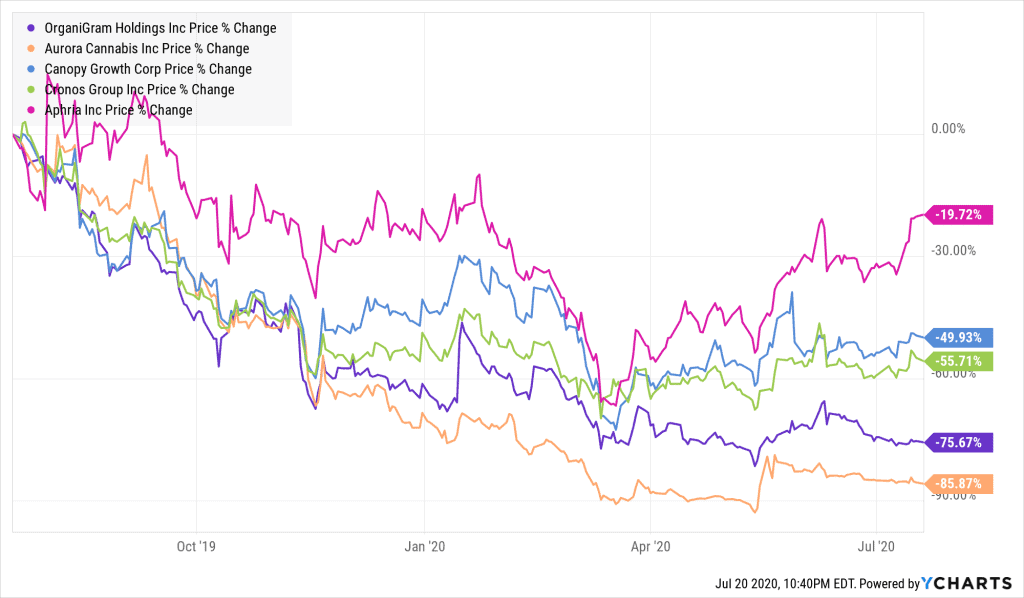

As is the case with other pot stocks, Organigram has dropped by 75.67% year to date.

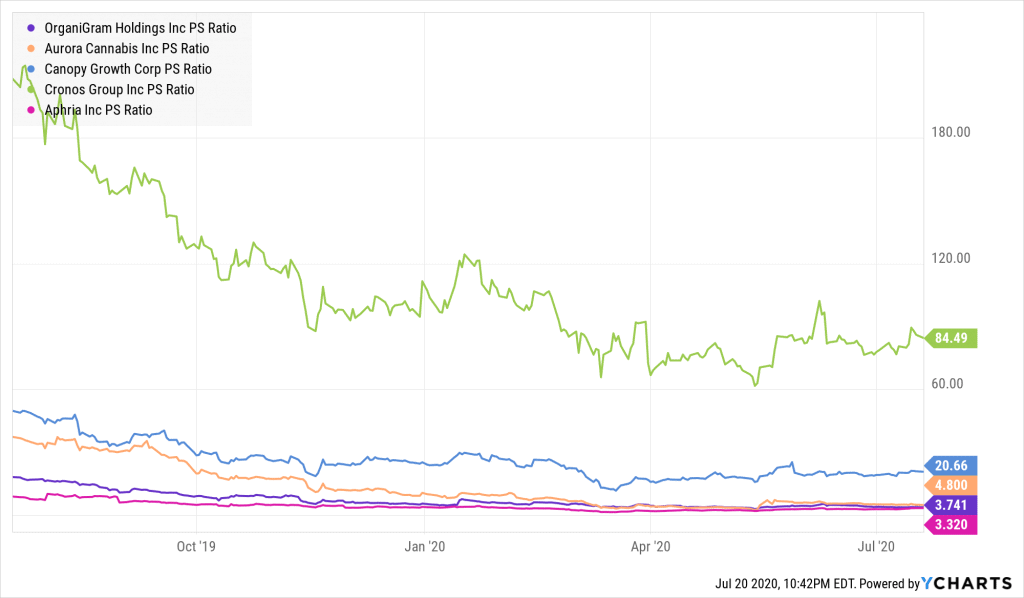

The company’s price to sales multiple is also amongst the lowest since it faces several operational setbacks, particularly its decline in revenue growth.

According to management’s commentary in the prior quarter, Organigram faced lower average net selling price due to increased competition and the rising wave of value brands. This in turn led the company to see its revenue growth turn for the worse.

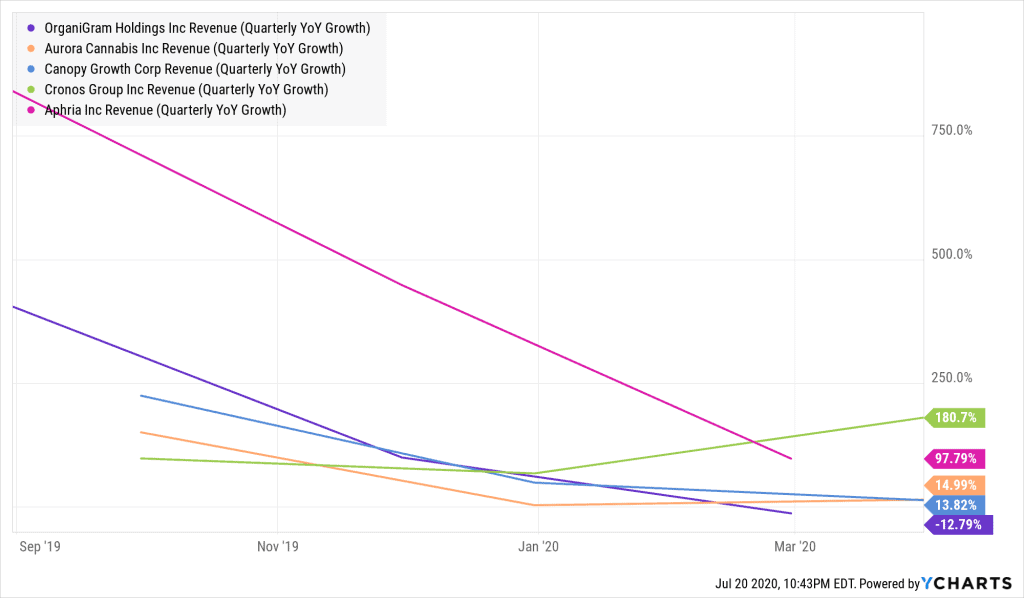

As shown by the following chart, the company’s revenue growth compared to its peers is quite embarrassing.

To make matters worse, the current pandemic forced the company to lay off 25% of its staff in order to prevent the spread of the virus. The lower workforce naturally caused cultivation, harvesting, and packaging operations to be drastically reduced.

As a result, this reduction in productivity was the primary reason as to why revenue declined by 22% since the prior quarter.

However thanks to the company’s priority on higher marginal products, such as edibles and their new value brand Trailer Park Buds, it managed to maintain its revenue per gram value of $5.7 compared to prior quarter’s $5.70.

Since the launch of cannabis 2.0 products, the company has also been benefitedby a higher revenue per gram than last year’s same period value of $5.40.

Points to Consider

Organigram’s disappointing revenue growth and failure to maintain the profitability it showed for a brief time in 2019 explain why the stock trades at such a discount to other producers.

The discount will not close any time soon while the company is struggling to remain relevant in an industry flooded with new products and brands every few months.

To their credit however as an early mover in the edibles market, Organigram has benefitted to some extent from a renewed interest in its business as it introduced a portfolio of products under its Trailblazer, and Edison brands.

These new revenue segments have helped the company maintain its revenue per gram even though its production operations slowed down due to high layoffs.

Their new value brand, Trailer Park Buds has also enabled them to retain and acquire some customers, who prefer cheaper cannabis flower over their other premium products.

However the lower sales price is hurting margins right when the company needs profits badly.

Just like most of the other Canadian licensed producers, Organigram should be kept out of your portfolio until they can reignite revenue growth (10%+ a quarter) or begin generating profits.

Until then your money and time is much better spent elsewhere.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.