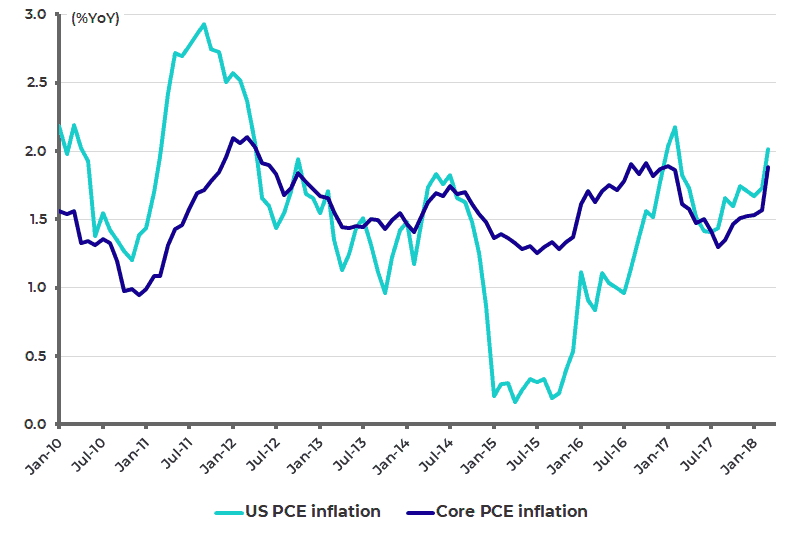

The latest inflation data has seen the Fed’s favourite inflation measure reach the 2% target. Headline PCE inflation and core PCE inflation rose from 1.7% YoY and 1.6% YoY in February to 2.0% YoY and 1.9% YoY in March. While core CPI inflation rose from 1.8%YoY in February to 2.1%YoY in both March and April.

US PCE Inflation

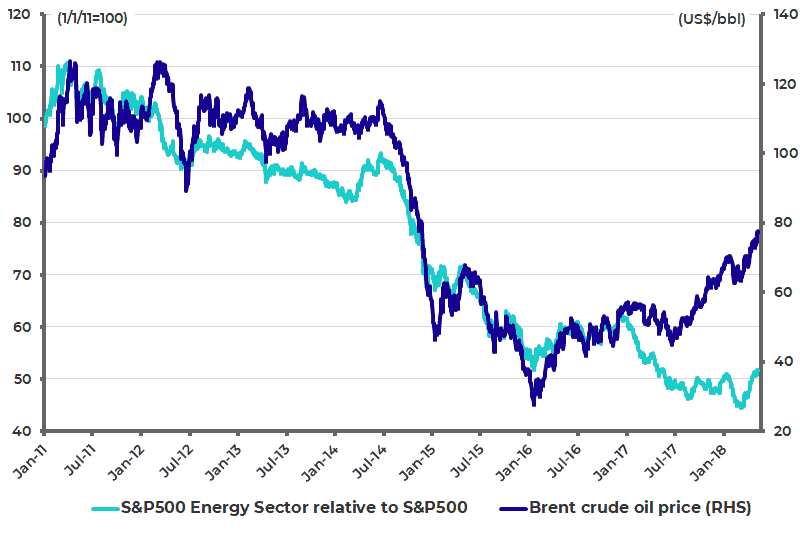

Energy Stocks Beginning to Outperform on the Back of Strength in Crude

The inflation story is also being encouraged by the accelerating strength in the oil price, with the Brent crude oil price up 15.3% so far this year.

Also, one of the emerging stock market trends this year is that energy-related stocks are starting to outperform with the S&P500 Energy Sector Index up 6.0% year-to-date compared with a 2.0% gain in the S&P500. The energy sector index has only really started to outperform since mid-March with the S&P500 Energy Sector Index outperforming the S&P500 by 15.5% since then (see following chart).

This week’s news on the US exiting the Iran nuclear agreement has added further impetus to the oil price.

S&P500 Energy Sector Relative to S&P500 and Brent Crude Oil Price

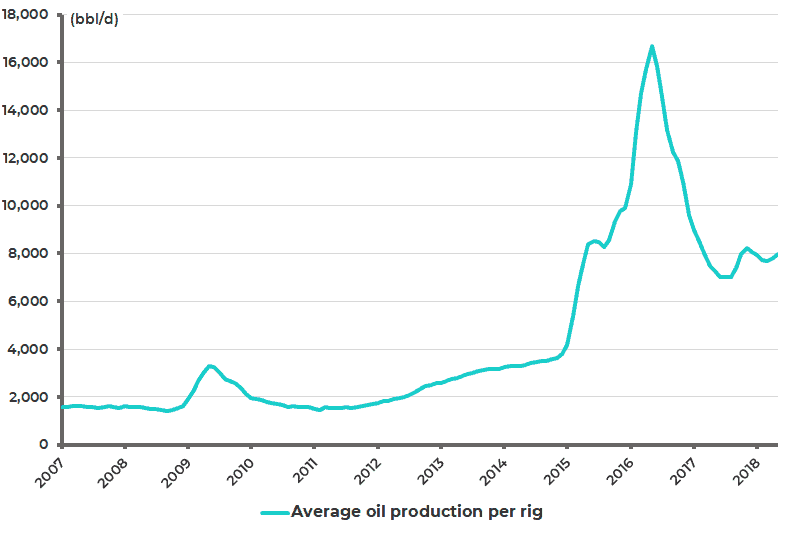

Outlook Remains Constructive: Diminishing Productivity in Shale and Strong Consumption

As previously discussed in Macro Battleship, it used to be this columnist’s view that oil was capped on the upside because US shale production would come roaring back on any oil rally above the US$60/bbl level and that would create the incentive for Russia to exit the OPEC production deal which has proved so effective. But that view was revised earlier this year for two reasons.

First, there is growing evidence that some of the best shale fields already have seen peak production. Second, there continues to be a remarkable divergence between the collapse in exploration activity and the ongoing increase in oil demand, mostly driven by rising demand in emerging markets.

Thus, average oil production per rig from seven major US shale regions peaked at 16,695 barrels/day in May 2016 and has since declined to an estimated 7,959 barrels/day in May, according to the US Energy Information Administration (see following chart).

While global proven oil reserves increased by only an annualized 0.1% in the three years to 2016, down from an annualized 4.9% in the three years to 2010, according to BP. By contrast, global oil consumption rose by an annualiszed 1.6% in the three years to 2016.

Average Oil Production per Rig in the 7 Major US Shale Regions

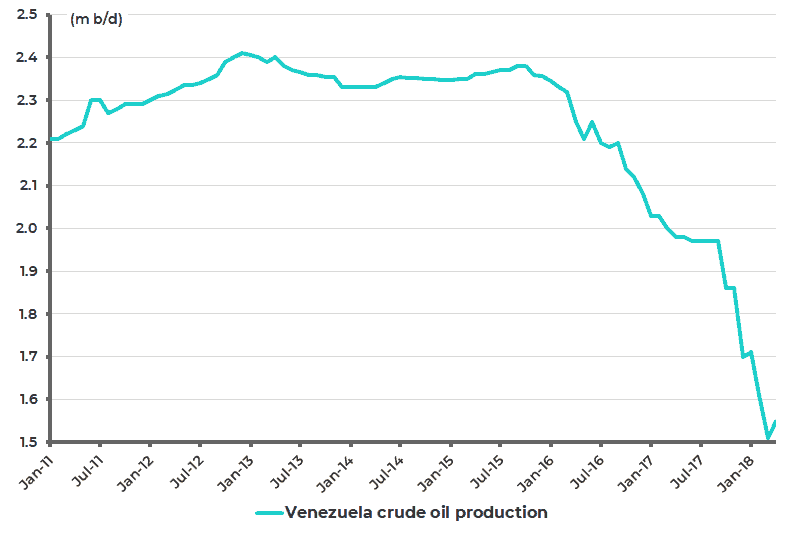

The International Energy Agency (IEA) expects world oil consumption to rise by 1.5m barrels a day this year to 99.3mb/d, up by 14mb/d or 16% since 2009. Still, this organization has a history of significant revisions. In fact, since 2003, the IEA has revised up Chinese oil demand estimates on average each year by 300,000 barrels per day.

There is also the potential for supply shocks. Venezuela production is apparently in free fall, declining from 2.38m bbl/day in October 2015 to 1.55m bbl/day in April (see Figure 12). There is also now the Iran issue.

Venezuela Crude Oil Production

Peak Electric Vehicle Hype

The dramatic collapse in oil exploration clearly in part reflects the hangover from the 2016 oil bust when Brent crude oil price bottomed at US$27/bbl in January 2016, down from a peak of US$128 reached in March 2012. But it also reflects the taxpayer-subsidized alternative energy and related electric vehicle hype which has generated so much attention in recent years.

The reality remains that cars are going to be powered in the conventional manner for many years yet, most particularly in the developing world which is where energy demand is really rising. Yet the stock market has been rewarding those energy majors who announce share buybacks rather than capital spending increases.

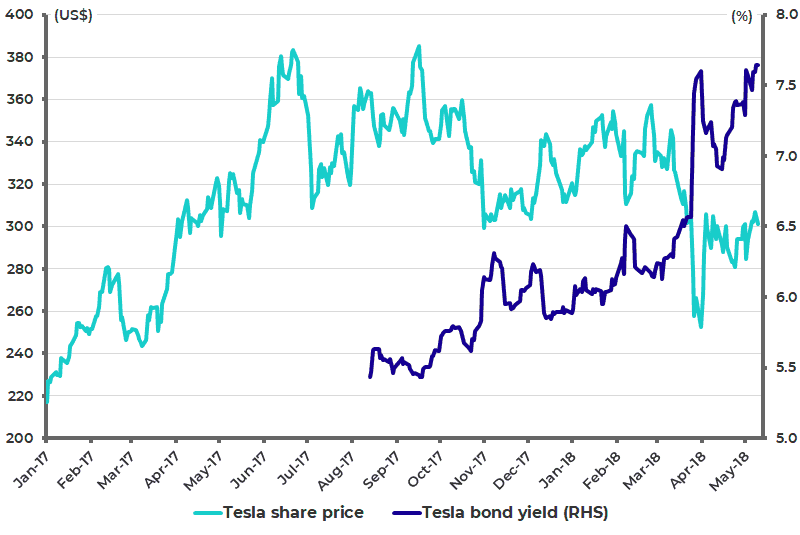

The electric vehicle hype looks like it might have peaked for now with Tesla’s share price down 22% from its high reached in September 2017 (see following chart) while its bond maturing 2025 is trading 472bps above Treasury bonds with the same maturity.

Tesla Share Price and Bond Yields

Rising Gasoline Prices will Ultimately Weaken the US Consumer

If the rising oil price adds to the inflation noise in a headline sense, even if the Fed’s formal target is core inflation measures, it is also the case that higher oil prices could ultimately prove deflationary in the developed world because they will eat into the disposable income of non-affluent consumers.

Thus it was reported by the Financial Times recently that for Americans in the bottom 40% of income distribution, the loss from higher fuel costs since 2016 has already exceeded the benefit from the tax cuts passed at the end of last year. What would be the impact of US$100 oil, a price target which is no longer unrealistic?

In this sense, a continuing rise in the oil price could become a catalyst for an economic downturn in the developed world which would be ironic given how quick the consensus was to write off fossil fuels a few years ago.

Russian Equities a High Risk/ Reward Play on Crude

If rising oil adds to the inflation noise in the short term, but increases deflationary risks longer term given the overwhelming probability in the developed world that income growth will not rise sufficiently to compensate for this, it is a different macro story for oil producers in the emerging markets.

This is why it makes sense to have bigger equity holdings in the emerging markets outside Asia than last year with Russia remaining the best, even if controversial, option for hedging exposure to countries in Asia vulnerable to a rising oil price, of which India is the best but certainly not the only example.

Strong Crude Oil Prices and Weak USD could Lift US 10-Year Above 3%

Meanwhile, a positive consequence of the continued strength in oil, and for that matter the rest of the commodity complex, is that it increases the likelihood that, in spite of the US dollar’s rally in recent weeks, that the US dollar will remain in a weakening trend given the longstanding negative correlation between oil and the US dollar.

The correlation between the US dollar index and Brent crude oil price is a negative 0.80 since 2000. A weak US dollar is good for emerging markets.

The ironic conclusion then is that alternative energy and electric vehicle hype has given a new lease of life to the fossil fuel industry by depressing supply dramatically. But if a rising oil price represents a risk to the current recovery in the medium term, in the short term it increases the risk of the current inflation scare getting worse, thereby increasing the risk of a break of the 10-year Treasury bond yield above the 3% level, even if it turns out to be a false break out.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.