Watching inflation expectations remains key for investors even as the Federal Reserve has remained predictably doveish.

The Fed’s continuing easy stance is in spite of mounting evidence of rising input prices, reflecting both restrained supply and pent-up demand.

Still, the American central bank continues to view these price pressures as transitory, driven by the exceptional circumstances created by an economic reopening after a pandemic, rather than as a signal of a fundamental trend change.

In a world where both central bankers and most economists have long since stopped paying attention to money supply growth, the Fed’s view will only be challenged by consensus economists if there is material evidence of the labour market tightening.

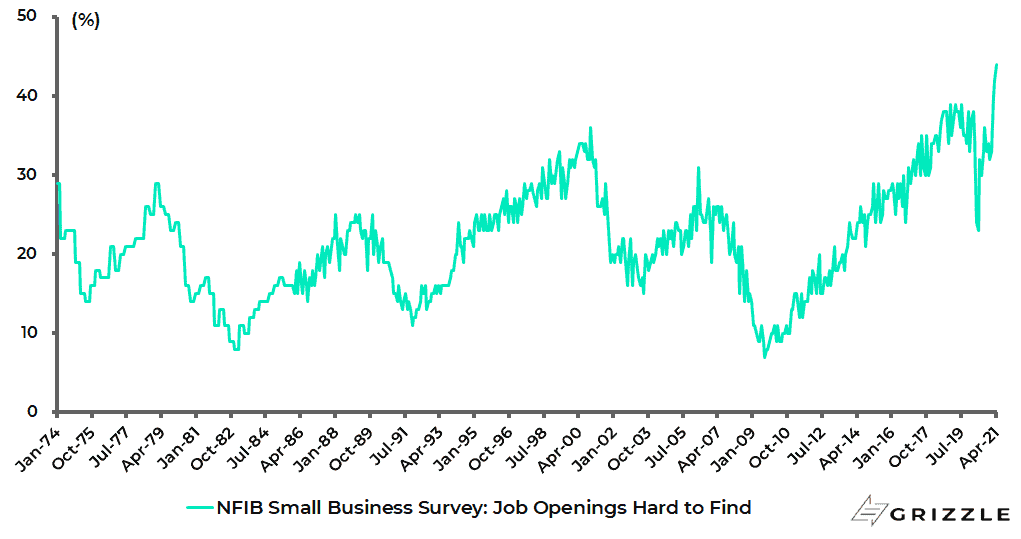

For now, that is not yet really the case, though something to keep an eye on is the rise in US small businesses saying it is hard to find labour.

The National Federation of Independent Business (NFIB) survey released earlier this month found that a record 44% of small business owners reported they could not fill job openings, and this data series goes back to 1974.

NFIB small business survey: Job openings hard to fill

But when it comes to employment it also needs to be remembered that this is a new type of Fed since it is focusing not just on aggregate employment levels but also on so-called ‘inclusive employment’.

This reflects the political reality of a new woke Fed.

And that will remain the case in the probably unlikely event that Jerome Powell, a nominal Republican, is re-appointed as Fed chairman next February.

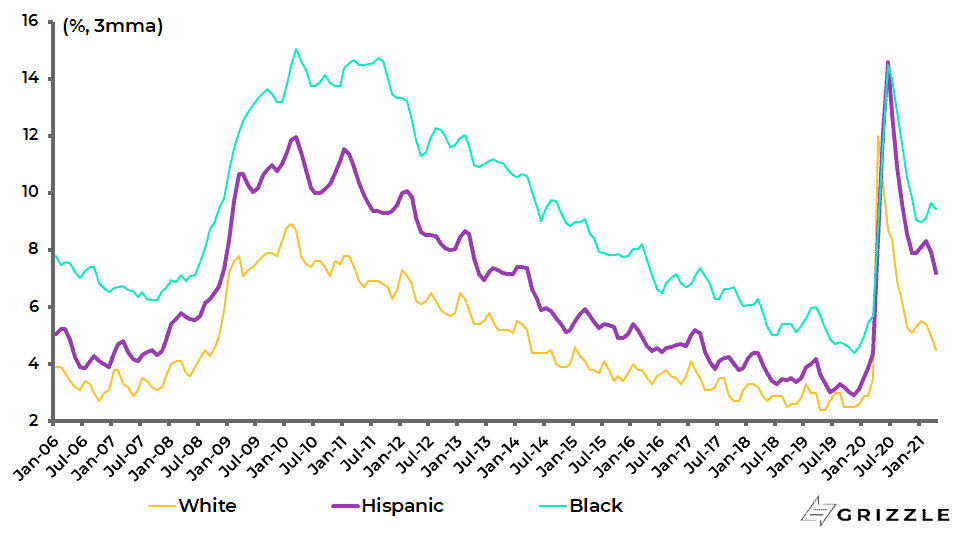

Meanwhile, it is worth noting that, for prime-age (25-54) individuals, the white unemployment rate is roughly four and two percentage points lower respectively than the Black and Hispanic unemployment rates.

US Prime-age (25-54) Unemployment Rates

Price Pressures in the System

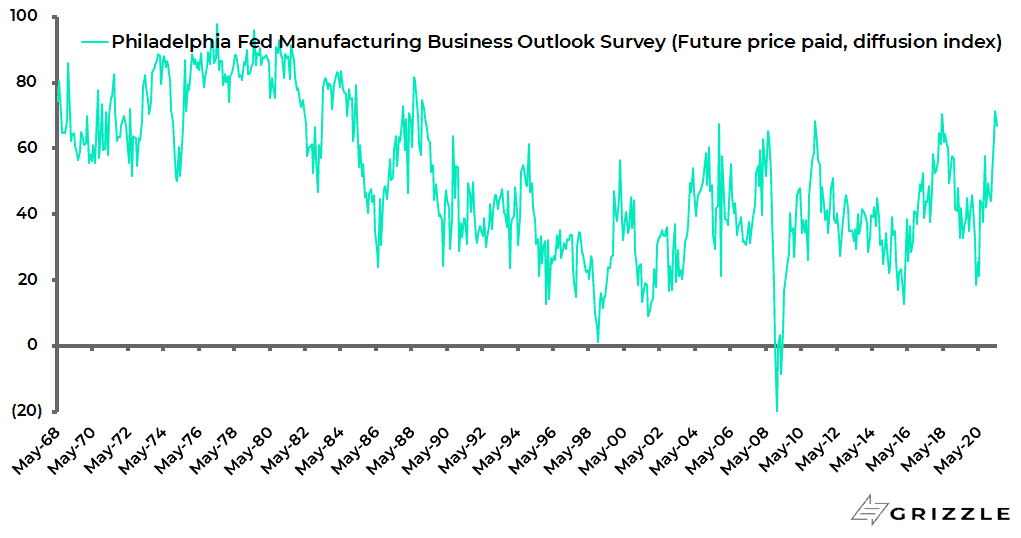

Meanwhile, in terms of the recent evidence of price pressures in the system, one good example is the Philadelphia Fed’s Manufacturing Business outlook survey’s future price paid index which rose to 71.5 in April, the highest level since 1989, and was 66.7 in May.

Philadelphia Fed Manufacturing Survey: Future Price Paid Index

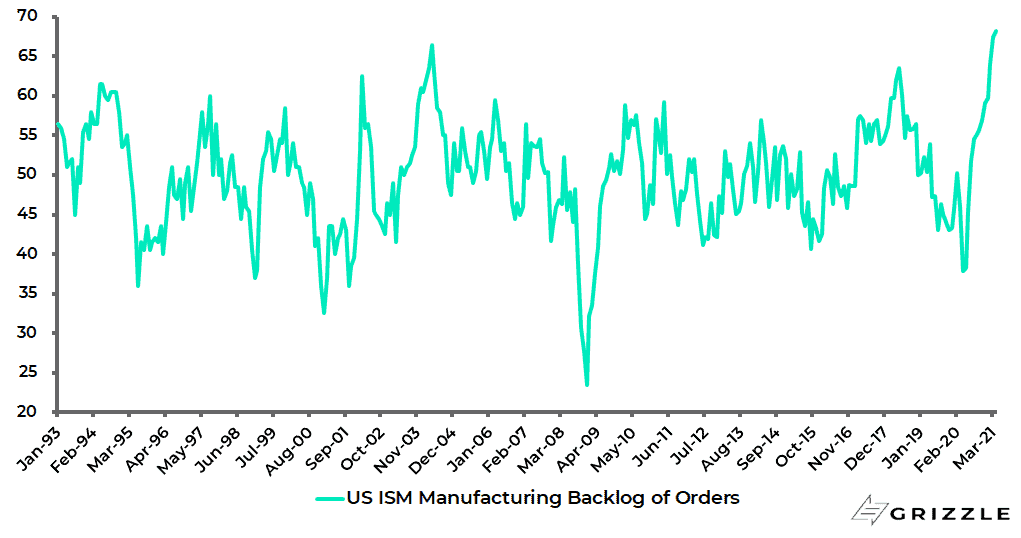

Another is the ISM Manufacturing survey’s backlog of orders index which increased to 68.2 in April, the highest level since the data series began in January 1993.

US ISM Manufacturing Backlog of Orders Index

Cyclical Recovery is Looking Strong

As for the American stock market, the combination of an easy Fed and cyclical recovery continues to be bullish for equities despite the selling pressure triggered by talk of a significant increase in the capital gains tax.

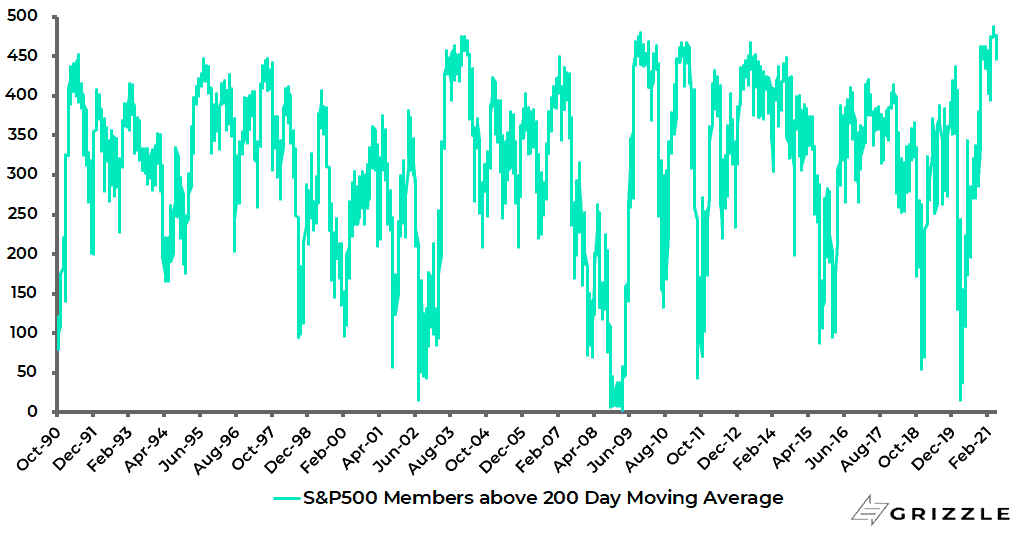

Perhaps the best technical signal for equities is that the number of S&P500 stocks trading above their 200-day moving average rose to 488 on 21 April or 97% of the total, the highest level since at least 1990, and is now 463 or 92% of the total.

Number of S&P500 members trading above 200-day moving average

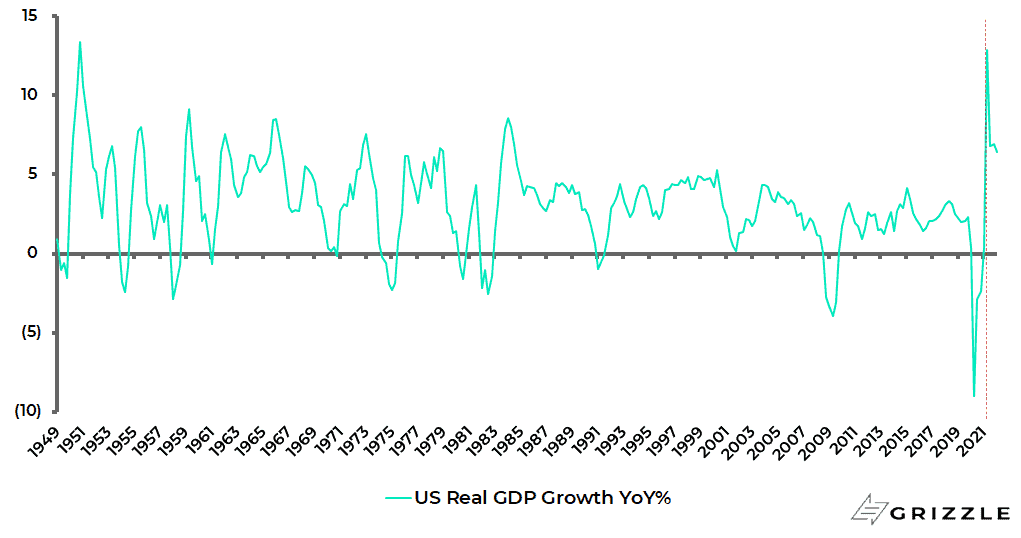

This is certainly not bearish and signals a broadening out of the bull market, which is only to be expected in the context of what is likely to prove the strongest cyclical recovery in America since 1950 with the consensus now forecasting 12.9% YoY real GDP growth in 2Q21.

US real GDP growth and consensus forecasts for 2Q-4Q21

If there is to be a real correction in stocks, it is most likely to be triggered by a tapering scare.

And that is only likely to happen after a further sell-off in the Treasury bond market and a further rally in cyclical stocks.

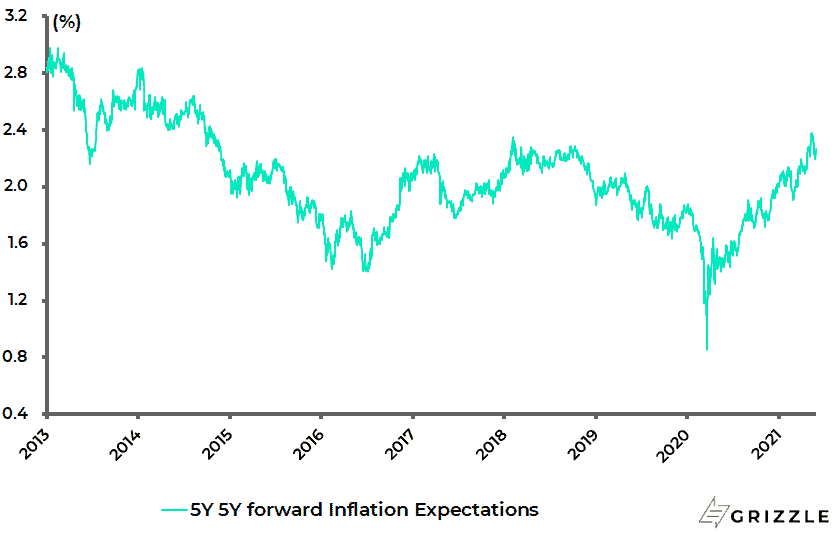

Meanwhile, the best way to monitor the timing of a tapering scare remains watching inflation expectations, most particularly if and when the 5-year 5-year forward inflation expectation rate gets to 2.5% or higher. It is now 2.27%.

US 5-year 5-year forward inflation expectation rate

Will Japan be Prepared for the Olympics in Time?

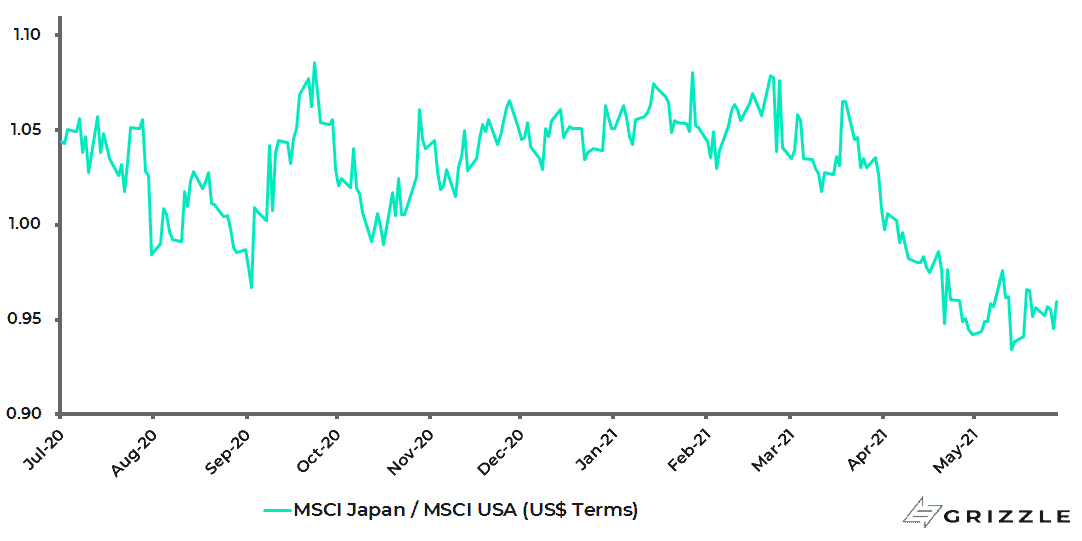

This writer has been an advocate in recent months of owning Japanese equities on the pro-cyclical reopening reflation trade.

The market has done satisfactorily in absolute terms.

The Topix has risen by 62% since bottoming in March 2020. But it has to be admitted that Japan has not been working of late in relative terms with the MSCI Japan underperforming the MSCI USA by 10% since mid-March.

MSCI Japan relative to MSCI USA in US dollar terms

There has been one negative which this writer would not have predicted as regards Japan.

That has been the remarkable lack of progress in implementing a vaccination programme despite the obvious incentive to do so provided by the Olympics which are meant to commence on 23 July.

This is despite the fact that Japan has 60,000 pharmacy stores which would seem ideally suited to administering a vaccine.

With a population of 126m, that implies an average of 1.4m vaccines a day or 23 per pharmacy store for the first dose of a vaccine.

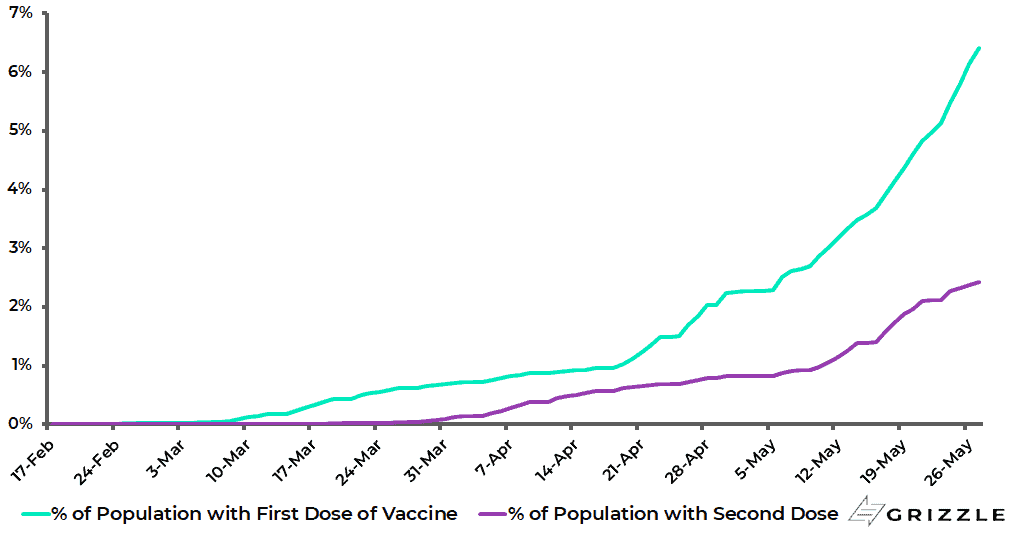

Yet the reality is that only 3.87m vaccines had been administered by the end of April, with only 2.83m or 2.2% of the population having received their first dose of vaccine, and a mere 1.04m or 0.8% having received a second.

Share of Japan population who have received the first/second dose of vaccines

It is also the case that only those over 65 have so far been able to apply.

It should also be noted that vaccinations for the elderly began only on 12 April, while prior to that vaccinations were only for healthcare/medical workers since the rollout began in mid-February.

Why the tortuously slow progress?

It is presumably partly related to the fact that, as a relative ‘winner’ from Covid, there was not the same sense of urgency.

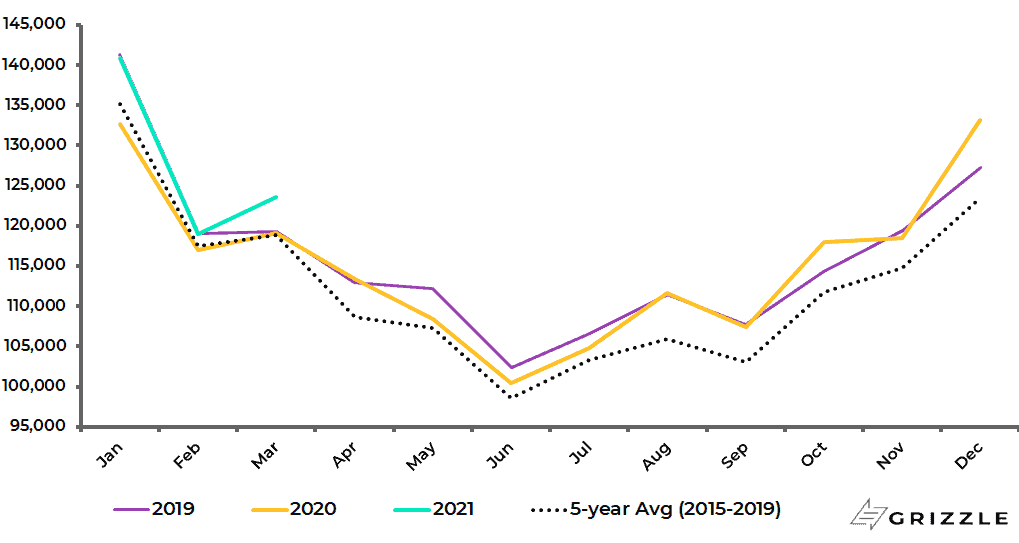

Indeed there were no excess deaths in Japan last year. Total deaths in Japan were 1.38m in 2020, 0.7% below the 2019 level of 1.39m and only 2.7% higher than the five-year average (2015-2019) of 1.35m.

Japan monthly total deaths

That said, the vaccination effort has finally accelerated of late.

The 7-day average daily vaccination rate is now running at 408,000 compared with only 52,000 in early May.

Japan 7-day average daily vaccination rate

While 6.4% of the Japanese population have now been vaccinated with at least one dose, up from 2.2% at the end of April (see previous chart).

This acceleration was prompted by a renewed Covid surge with the government declaring on 23 April a third state of emergency in Tokyo, Osaka and Kyoto on evidence of the arrival of the more infectious new variants.

Meanwhile, the incentive provided by the Olympics would have suggested an expedited vaccination rollout, not least because of the considerable political capital the Japanese government has invested in the project.

The target is now for the entire over 65 age group, which account for some 30% of the total population, to have been vaccinated by the end of July.

The health ministry has also said that the rollout of vaccines for people under 65 may begin in July depending on supply.

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.