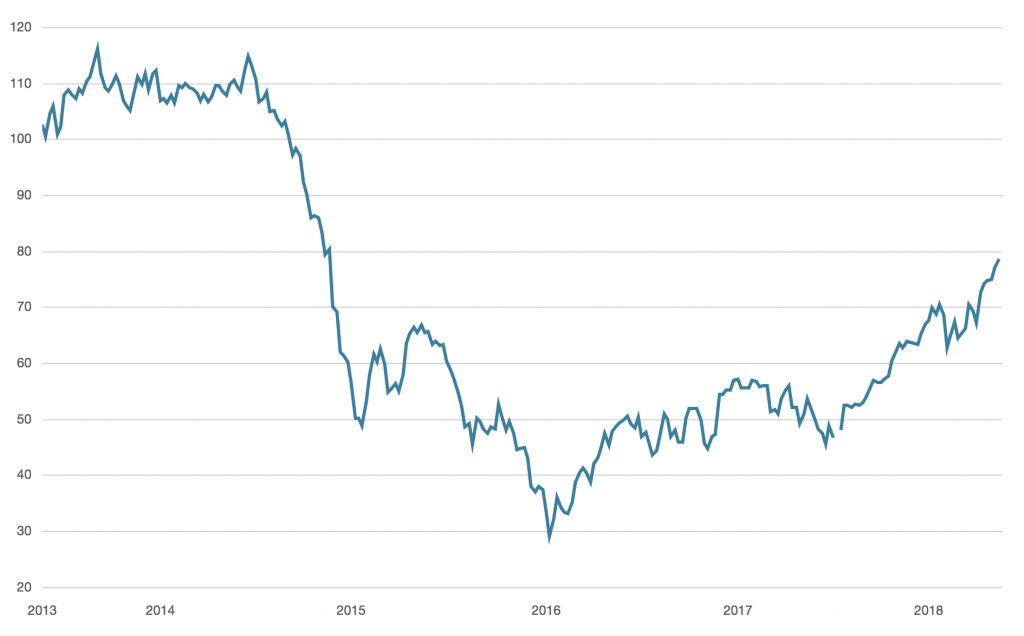

In just over a year oil has seemingly gone from dead end, over supplied commodity (akin to corn), to supply squeezed, one-way hedge fund trade.

Undoubtedly the backdrop has been very constructive, Grizzle’s Chris Wood highlighted the opportunity in mid-March when Brent crude was hovering at $66/barrel — we’re currently sitting at $77/barrel.

Brent Crude Price ($/barrel)

OPEC Proving the Cartel Model Still Works with Help from Venezuela and Strong Oil Demand

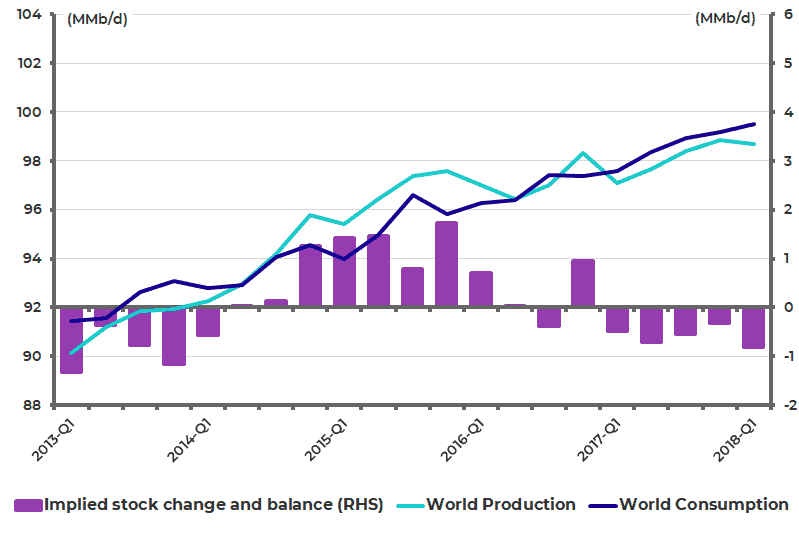

In November of 2016, OPEC countries along with Russia agreed to cap oil production at 32.5 MMb/d in response to oil getting crushed to $29/barrel in January of that year.

Since the supply cut was put in place, global crude oil demand has been outpacing crude oil supply (chart below), putting a meaningful dent into record high inventories along the way. When the global economy is expanding (emerging markets in particular) — oil demand is by definition robust (no exceptions). Oil is the most important lubricant for growing economies.

Global Crude Oil Supply vs Demand

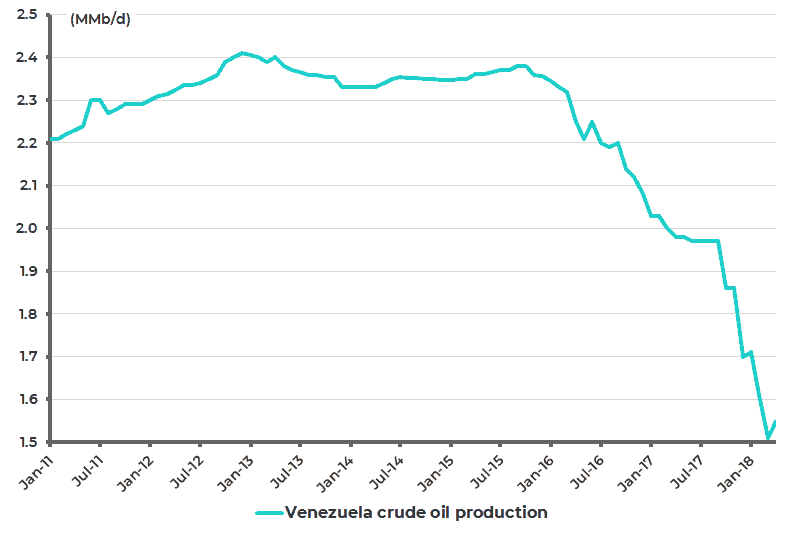

Low oil prices typically have a high correlation with the implosion of shit show banana oil republics. Venezuela was the obvious candidate this time around. Production is off nearly 1 MMb/d from the peak and will be likely off another 1 million in short order with the ‘re-election’ of the socialists.

Socialism in a Graph: Venezuela Crude Oil Production

US Shale Won’t Die — Russia Leery that Oil gets too Hot

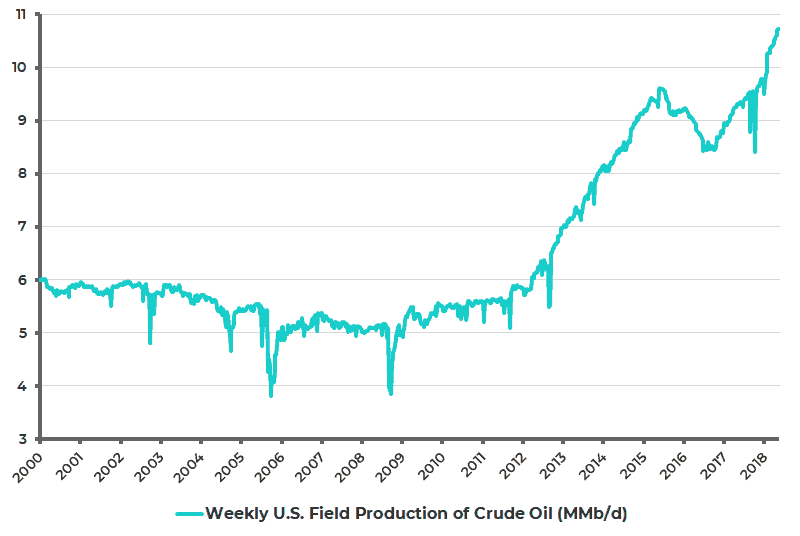

Saudi tried to thread the needle by delaying production cuts as long as possible in an effort to thwart the long-term viability of US shale oil production. The low oil price environment did have a meaningful impact on the economics of shale drilling. US production fell by by over 1 MMb/d from 9.6 MMb/d (July 2015) to 8.5 MMb/d (July 2016).

However, as the oil price has rallied so has US oil production, spiking to an all-time high production rate of 10.7 MMb/d — a level higher than the previous peak set in November 1970 at 10.1 MMb/d.

Drill Baby Drill: US Oil Production (millions of barrels per day)

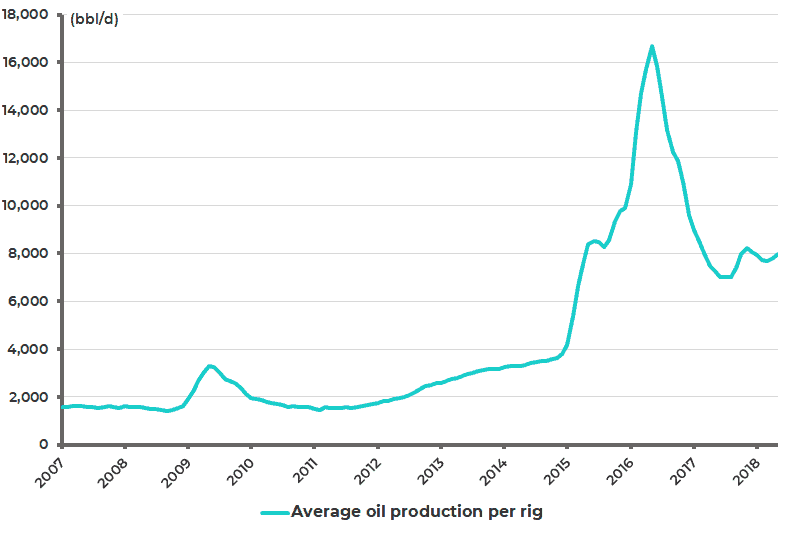

What’s clear is that sub $50/barrel US shale has a hard time earning its cost of capital. Likely some of it works between $40-50/barrel and none of it works below $30/barrel.

While the data certainly suggests that the sweetest acreages have been slurped up by horizontal fracking, the threat is that marginal wells start to make sense again in the current high oil price environment. All things equal, OPEC should have eased off supply cuts at $70/barrel Brent.

Average Oil Production per Rig in the 7 Major US Shale Regions

As we head towards the next OPEC meeting in June, Russia and Saudi Arabia are discussing the possibility of relaxing the production caps. Russia’s oil minister Alexander Novak provided the following assessment of the current price environment:

Can OPEC legitimately defend an $80/barrel Ceiling?

Saudi and Russia can and will certainly talk down the market as they are doing currently, but that strategy is fleeting at best. The two wild cards to the upside for the market are:

- More Venezuelan lost production

- Middle East flare up/Iran conflict

Of the 1.8 million barrels that OPEC could bring back online either of these wild cards would meaningfully nullify the market impact of relaxing production caps.

The ultimate fear for OPEC is that they lose control of the crude oil script as they did in 2014, a renewed sizable surge in US shale oil production could send crude back down to $50/barrel in a matter of months. This would of course be a near-term pricing phenomena as the quality of the shale rocks are diminishing and the hurdle rate for debt-fueled drilling rises with the increase in rates.

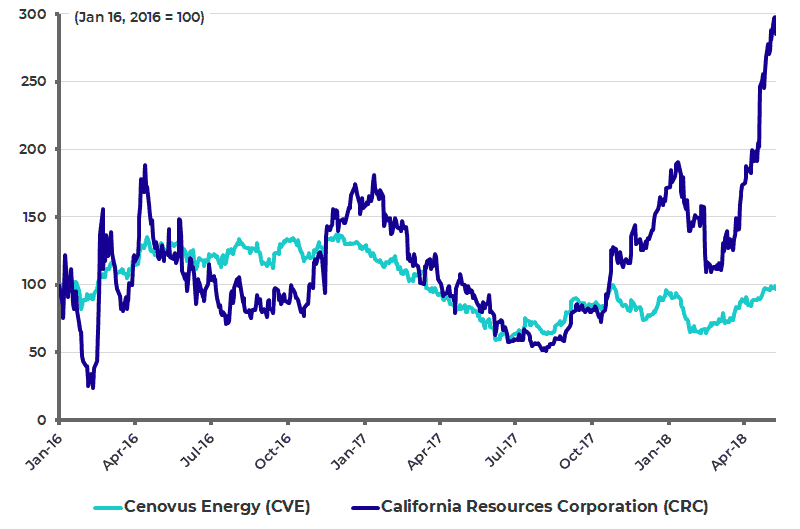

Recommended ‘Trash Can’ Pair Trade: Long Cenovus / Short California Resources

I normally don’t bother with companies that I loathe, other than to short outright. There are times when being long garbage makes sense, only if you can short something of similar stench: the long Cenovus (CVE) and short California Resources (CRC) trade ticks all the boxes. Both are loaded with debt and have high cost structures. CRC just has more.

At this point the oil market likely has a marginal upside skew (long tail of course). By definition, irrespective of the differentials between Canadian heavy crude oil pricing vs West Texas Intermediate — a $90-100/barrel world is one where all barrels (no matter how handicapped) are valuable.

In the oil upside scenario Cenovus will catch a sizable bid no matter how much investors want to keep looking away. The other positive is that Alex Pourbaix (new CEO) isn’t the walking short-thesis that ex-CEO Brian Ferguson was. Brian’s opus was getting fleeced by ConocoPhillips to buy $18 billion of swamp assets.

If oil moves lower, the trade works nicely as the market rewarded CRC during the recent oil rally, while CVE remained firmly in the penalty box. CRC’s production is still in decline at current oil prices because permitting issues in California mean a slow ramp up of drilling to take advantage of higher prices.

Trash Can Pair Trade: Long CVE / Short CRC

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.