The Organization of the Petroleum Exporting Countries (OPEC) concluded its biannual meeting of despot dictators on Friday in Vienna.

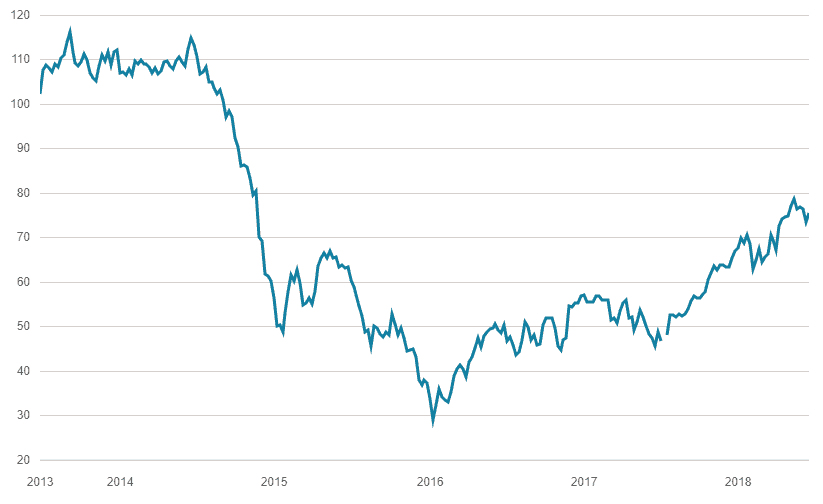

As Grizzle expected, OPEC has drawn a line in the sand at $80/barrel — agreeing in principle to bring anywhere between 700k to 1 million barrels per day back on the market.

Without a doubt this production increase creates a near-term psychological headwind that would prevent crude from pushing meaningfully above $80/barrel for a sustained period.

Brent Crude Price ($/Barrel)

Production Wild Cards: Iran and Venezuela

As highlighted last month, the wild cards to the upside for the oil market are Iran and Venezuela. A worst case scenario could wipe off between 1.6 – 2.5 million barrels per day of production from the market.

Chris Wood provided an excellent analysis of the current political loggerheads between the US and Europe over Iranian sanctions.

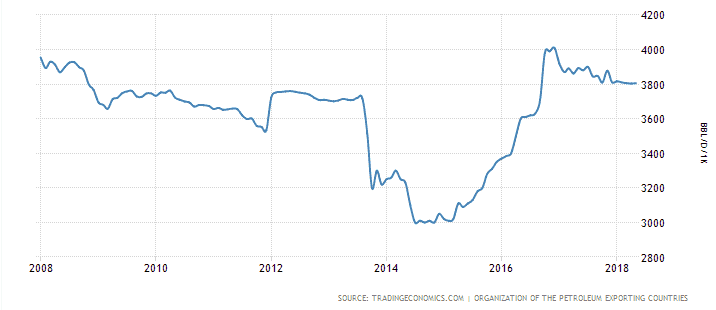

This tension should enable Iran to continue to unload barrels onto the global market as usual (3.8 million barrels per day) over the near-term. Our base case is that Iranian production doesn’t fall to pre-nuclear deal levels (3 million barrels per day).

Iran Crude Oil Production (thousand barrels per day)

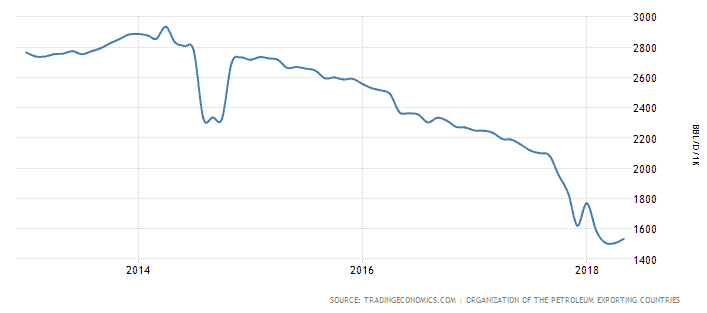

However, the situation is far more precarious for Venezuela where rule of law and oil production are both in free fall. The country currently produces 1.5 million barrels of oil per day, 700 thousand barrels per day lower than a year earlier.

It’s really anyone’s guess what production looks like a year from now. A reasonable base case would be down another 700 thousand barrels per day, however a complete halt of production is certainly within the realm of possible.

Venezuela Crude Oil Production (thousand barrels per day)

US Shale: Can OPEC Put the Monster Back in the Bottle Again

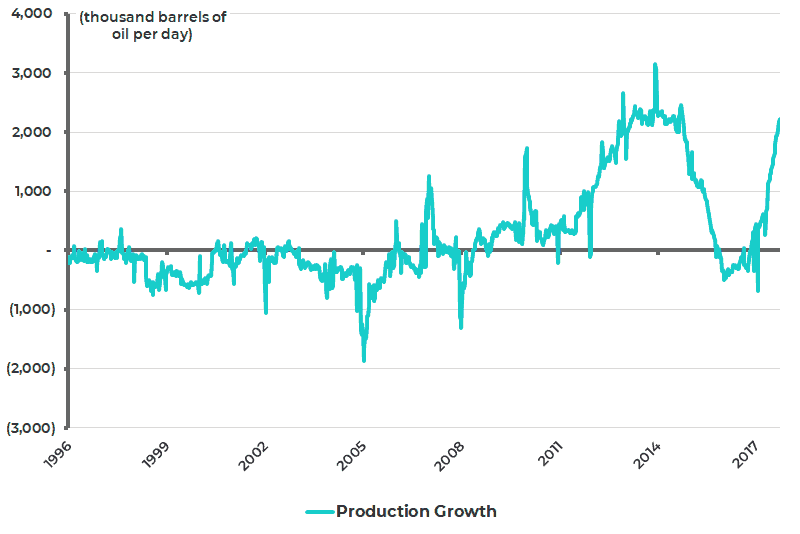

An unintended consequence of OPEC artificially tightening the global oil market was allowing US shale producers back in the game. The production monster is back with a vengeance, growing at a clip of 2 million barrels per day on rolling 2-year basis, this is inline with growth levels that ultimately lead to the oil price collapse in 2014.

OPEC’s 700 thousand to 1 million barrel per day loosening of the market will ultimately prove too little to arrest the current growth spurt in shale — prices above $60/barrel shale will continue to produce adequate returns over the near-term.

Undoubtedly, over a longer term basis the quality of the rocks will continue to deteriorate along with the economic break-evens.

US Crude Oil Production Growth – Rolling 2 Year

The Read Through for Oil Stocks

At this juncture it makes little sense to take an extremely bullish tilt on either oil or the stocks of oil producers. The combination of OPEC’s increased production and established US shale growth more than offsets a worse case geopolitical scenario.

Exploration and production stocks are likely range bound at best and institutional investor interest has waned significantly for both Canadian and US names.

Global integrated oil stocks likely offer the best risk reward for an investor that feels compelled to have a big toe in oil market. Dividend yields in the group remain attractive and provide a level of inherent inflation protection that other high yielding equities (utilities) simply do not.

| Company | NYSE Ticker | Dividend Yield | Forward P/E |

| Shell | RDS-A | 5.5% | 10.7x |

| BP | BP | 5.3% | 13.2x |

| Total | TOT | 4.6% | 10.1x |

| Exxon | XOM | 4.1% | 15.2x |

| Chevron | CVX | 3.6% | 14.9x |

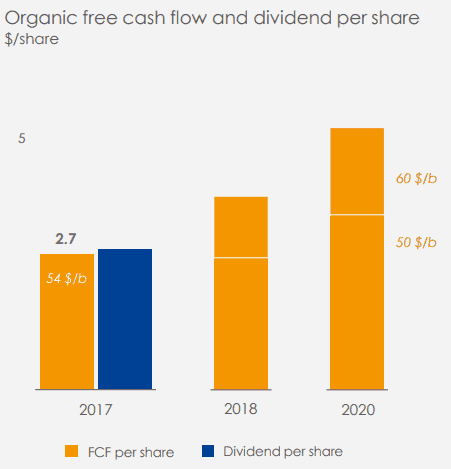

Total (Ticker: TOT) would be our preferred name within the integrated sector. The stock trades at a 30% discount to the peer group average on a price-to-earnings basis with an attractive 4.6% dividend yield that is inline with peers.

Additionally, the company is committed to growing its dividend per share 10% by 2020, free cash flow growth will enable the company to cover that dividend fully at an oil price as low as $50/barrel.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.