Very few Canadian technology stocks have received more attention than OpenText (OTEX), the Waterloo-based analytics and AI intelligence company. Despite being Canada’s largest software company, OpenText is undervalued based on expected per-share earnings. Its strong history of free cash flow generation and revenue growth suggest its brighter days are still ahead.

Summary

- Ticker: OTEX (TSX, NASDAQ)

- Market Cap: $13.7 billion

- Annual Revenue Growth: 22.9% (June 2018)

- Free Cash Flow: $605 million

OpenText: The Business Case

Despite being around for nearly three decades, OpenText was a relatively small player before the financial crisis. In the last ten years, the company’s profile has risen in lockstep with the big data revolution.

As a software company specializing in enterprise information management systems, OpenText has managed to tap into the cloud and data analytics markets while still offering product suites for a variety of industries. The breadth of its products and services is extremely broad, which means its addressable market is very large. Its growing financial position proves it is tapping into the right markets.

OpenText has made the Asia Pacific region a primary target for expansion. The region accounted for 10% of the company’s revenue in fiscal 2018. An emphasis on recurring revenue has given OpenText the ability to achieve its scalability goals and boost profitability. In fiscal 2018, recurring revenues grew 3% to $530 million.

Financial Position and Stock Performance

In the year ending June 2018, OpenText generated $2.815 billion in revenue, an increase of 22.9% over the previous year. Since 2009, the company has increased its annual revenue every year except one, and even that wasn’t a big miss. The company’s cumulative revenue growth over that period is a whopping 258.1%.

Free cash flow is another area of considerable strength. As a recap: free cash flow enables companies to pursue other activities that increase shareholder value. On that basis, OpenText has considerable runway for future growth.

In 2018, the company’s free cash flow was valued at $605 million, an increase of 68.1% over 2017.

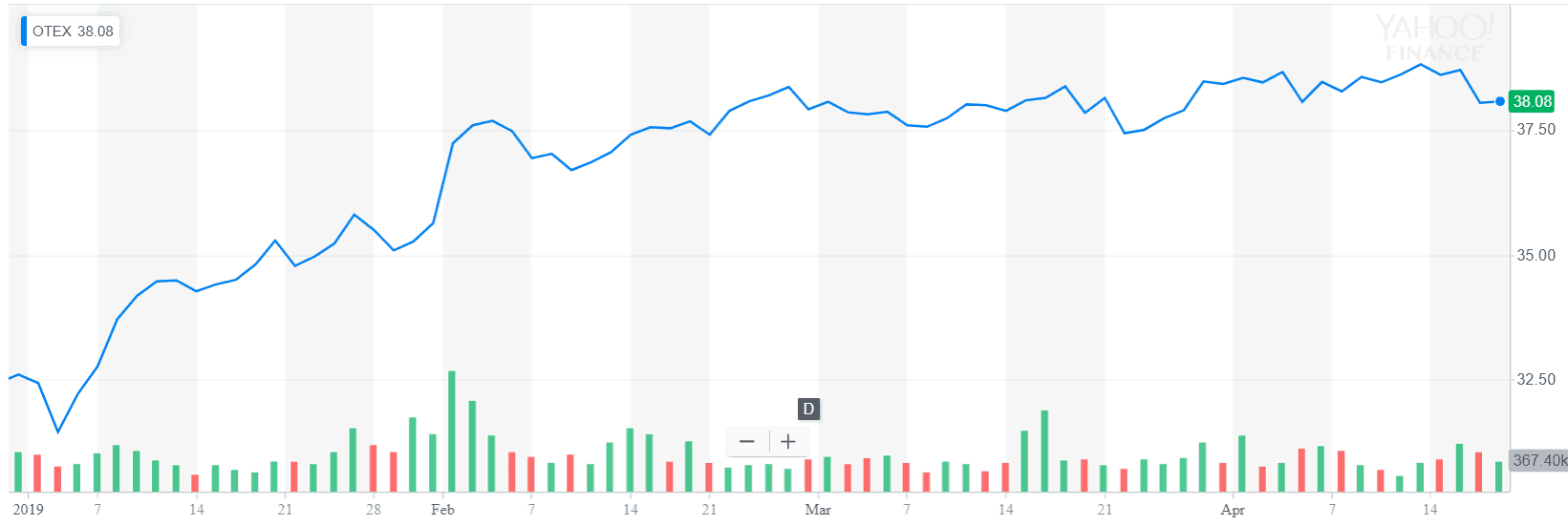

In U.S. dollar terms, OTX shares have appreciated more than 18% year-to-date, but the company is still undervalued based on expected earnings. Its forward P/E of 12.8 is well below its current P/E of more than 39.

OpenText’s expected profitability increases the likelihood of higher dividend payouts in the future. The company’s stock currently yields 1.59%, which is well above the technology-sector average. The company has grown its dividend successfully in each of the last four years, making it a strong contender for income-focused portfolios.

Conclusion

A lot has been written about OpenText in recent years, and for good reason: its value metrics suggest future growth is extremely likely. As a mid-cap Canadian stock, OpenText is well positioned to increase shareholder value, especially if its pivot toward Asia continues as expected.

Disclaimer: Author holds no investment position in OpenText Corporation at the time of writing.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.