Bottom Line

Organigram put up a second straight quarter of solid results, reporting $27 million of net revenue that beat street estimates by 13%.

Most importantly the company is selling cannabis the consumer wants to buy, demonstrated by a 90% increase in revenue in the company’s second quarter with legal sales.

Peers who report in the coming two months will likely show they struggled to grow revenue as the legal market gets off to a slow start.

We are concerned, however, with an apparent decrease in selling prices. Across the board, Organigram saw flower and oil price declines of between 5%-17% quarter over quarter.

If the industry is facing an acute supply crunch as many producers allege, why are legal cannabis prices falling?

| Rev/Gram, Rev/mL | 1Q 2019 | 2Q 2019 | QoQ Change |

| Rec Flower | $5.09 | $4.91 | -4% |

| Medical Flower | $6.87 | $5.71 | -17% |

| Rec Oil | $0.96 | $0.91 | -5% |

| Medical Oil | $1.72 | $ 1.58 | -8% |

Regardless of prices, Organigram continues to be the lowest cost producer in Canada and is the only producer to generate positive EBITDA post-legalization.

EBITDA per Gram Run Rate

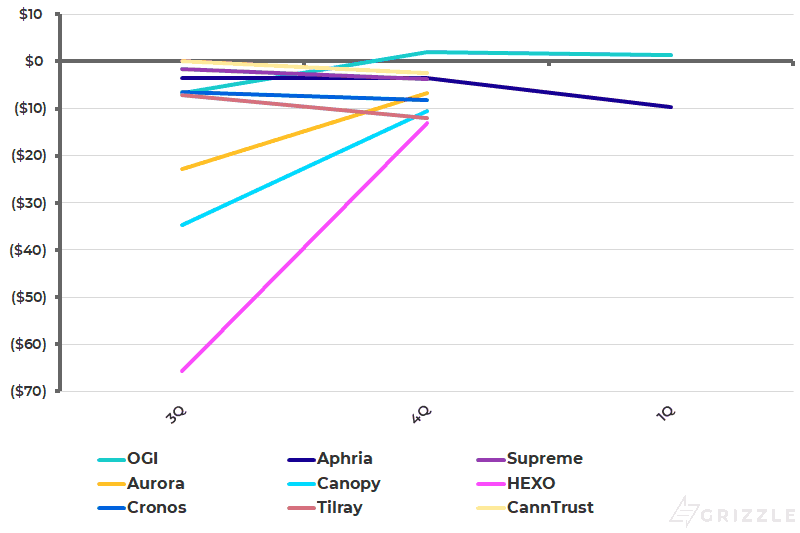

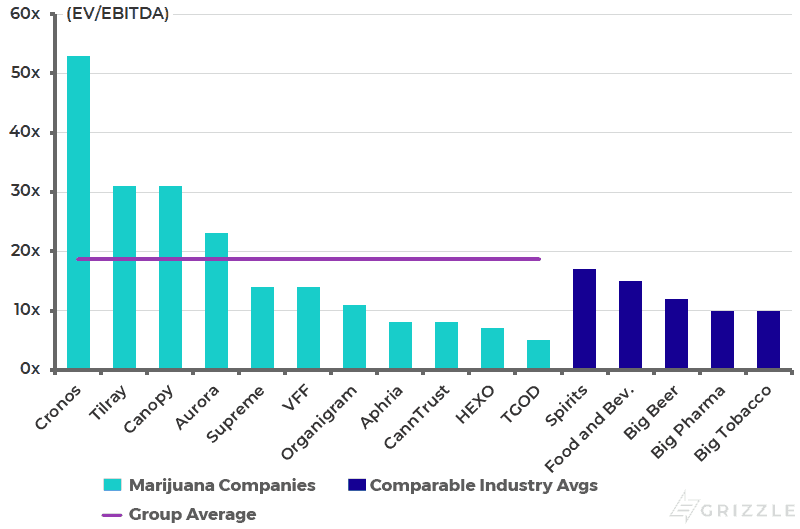

The stock trades at a 50% discount to its largest peers, which we think is unwarranted.

If Organigram keeps generating industry-leading profitability, it will either re-rate closer to peers or become a takeout candidate, both positive outcomes for shareholders.

Operational Review – OGI’s Product is in Demand

Organigram’s revenue increased ~90% from $12.4 million to $23.8 million on the back of a ~140% increase in sales of cannabis flower and equivalent, which doubled from 2,100 kg to 4,987 kg. This is positive news for Organigram as it shows they have quality products that are in high demand by consumers.

The discrepancy between the increase in revenue compared to sales (90% increase compared to 140%) can be in part attributed to their lower sales prices across all products (recreation and medical cannabis oil and flowers).

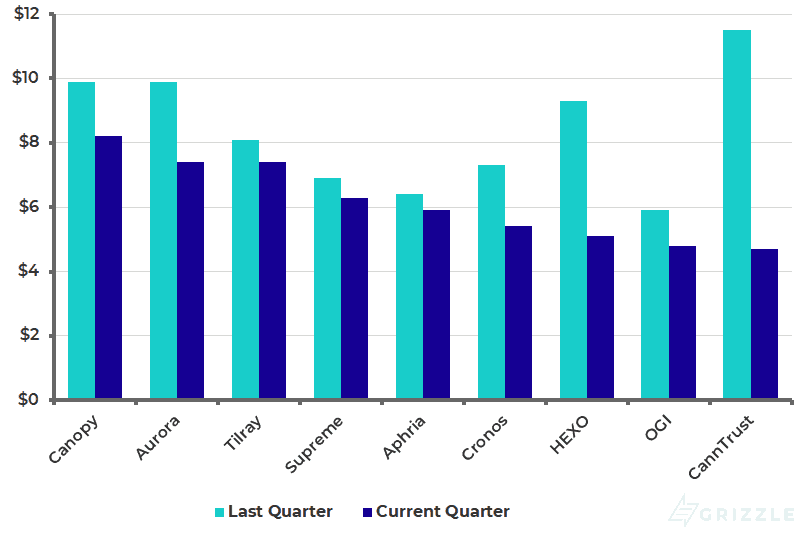

Their revenue per gram of $4.8 for the quarter left them near the bottom of the industry.

QoQ Revenue Per Gram of Cannabis Produced

Organigram’s cannabis production was achieved on costs of $10.9 million, a quarter over quarter increase of 250%. Their gross margin of $12.9 million represented a quarter over quarter increase of 46% from $8.8 million. This significant spike in production cost (when compared to gross margin increase) likely stems from the higher costs associated with growing cannabis in the Canadian winters. For the upcoming warmer quarters, we expect to see a seasonal decrease in growing costs.

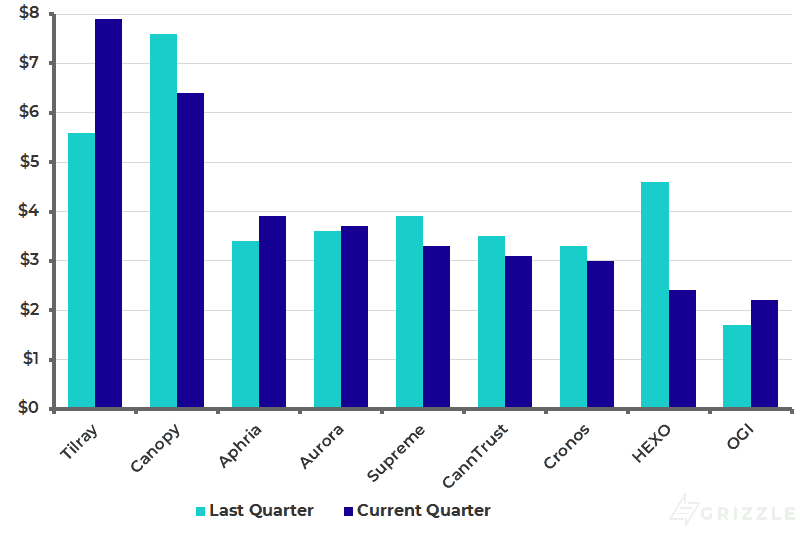

Even with the jump, Organigram’s production costs per gram of $2.2 leave them as the cheapest producer compared to peers.

Production Costs Per Gram for Canadian Producers

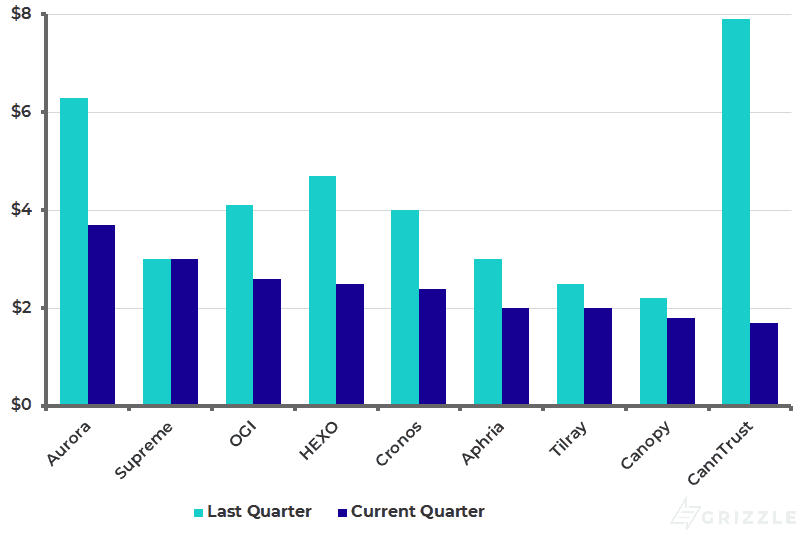

In comparison, their gross margin per gram of $2.6 was average compared to peers. Their industry leading production costs and average gross margin indicates they have lots of room to improve operating expenses and drive up profitability.

Gross Margin Per Gram

Overall, Organigram has a quarterly cash burn of $59 million compared to their total cash and equivalents of $208 million. This leaves them in the middle of the pack compared to peers, with only three companies holding more than 1.5 years of cash. However, as they are the only Canadian producer generating positive EBITDA, they are certainly in a much stronger position than most of their peers.

Organigram Continues to Improve Cannabis Production and Processing

In other developments, the phase 4 expansion of their Moncton facility is progressing, where they will be adding 92 incremental grow rooms by the end of 2019, which are expected to triple capacity to 113,000 kg per year.

The company also announced another 56,000 square feet became available in one of their facilities in March and is being refurbished and designed for additional extraction capacity.

This supports their push to improve extraction and processing capabilities for their focus area of vaporizers and edible products.

Organigram also announced a new nano-emulsion for use in infused beverages that works on the body in only 10-15 minutes. The company is seeking an experienced partner to help them roll out an infused beverage brand later in 2019.

Organigram Remains Undervalued

Organigram is putting up results that put all the other licensed producers to shame.

As the company continues to execute there is no doubt the valuation discount to peers will shrink.

Year-to-date performance has already matched much larger well-followed peers, showing that strong results are rewarded.

Organigram remains one of the bright spots in a Canadian cannabis industry struggling to justify lofty valuations.

2020 Estimated EV/EBITDA

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.