Organigram Holdings (TSE:OGI, NASDAQ:OGI) posted disappointing financial results for Q2 2020.

More important than earnings is the company’s rapidly deteriorating financial position which is a surprise for what was once the most profitable Canadian licensed producer.

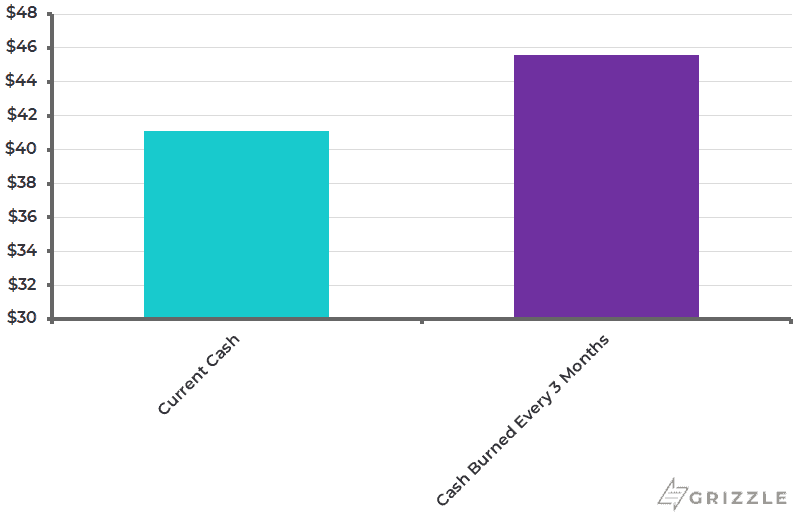

The company burned $46 million of cash for the second quarter in a row and now only has $41 million remaining in its bank account.

Most importantly, the company violated a covenant on its debt this quarter.

[su_panel]A covenant is basically a rule bankers put in place to protect themselves from the company not paying them back.[/su_panel]Organigram previously had C$50 million left to borrow on this facility from BMO, but now that the company is in violation of its covenants, we think it’s unlikely the bank will let them draw down that money.

If OGI can’t borrow another C$50 million they are on track to run out of money by the end of May 2020.

The Cash Situation is Pretty Bad

Yes the company laid off 45% of the workforce on April 7th, but they paid out two weeks of pay as an act of goodwill and will be on the hook for at least another two weeks of severance pay if those employees aren’t rehired.

[su_panel]Yes there are a lot of moving parts here, but all investors need to understand is OGI will likely be raising more money and diluting current shareholders in the near future. [/su_panel]The stock price is going lower for now.

A Review of Results

Revenue came in at $23.2M which missed analysts’ estimates of $25.07M

The company cited the following reasons for lower than expected revenues:

- Lower recreational flower and oil sales volumes compared to Q2 2019 when the timing of large pipeline fill orders to Alberta and Ontario occurred to fulfill supply shortages following the legalization of adult-use recreational cannabis sales;

- Lower average net selling price from increased competition;

- Evolving consumer preferences, for which a provision for returns and price adjustments was recorded in Q2 2020, mostly related to cannabis oil.

EBITDA came in at -$6.6M which significantly missed analysts’ estimates of $3.074M

The much larger EBITDA loss than last quarter was due to a 50% increase in both operating and cost of goods sold as the company dealt with the launch of edibles and vapes.

| Q1 2019 | Q1 2020 | YoY % Change | |

| Revenue | $26,934 | $23,221 | -14% |

| Costs of Goods Sold | $10,890 | $15,811 | 45% |

| Gross Margin | 60% | 32% | -46% |

| Op Costs | $10,890 | $15,811 | 45% |

The company cited that the higher cost of sales was due to “higher post-harvest costs, initial production inefficiencies resulting from the launch of vapes and chocolates” aka ramp-up costs from the rollout of Cannabis 2.0.

One interesting thing to note is that the company was forced to reclassify its $76.4M loan from BMO as a current liability as opposed to a long term debt considering that the company is in violation of a covenant on the loan.

The fact that the company’s long term debt went down 99% and their current liabilities went up 154% quarter-over-quarter, was due to this reclassification.

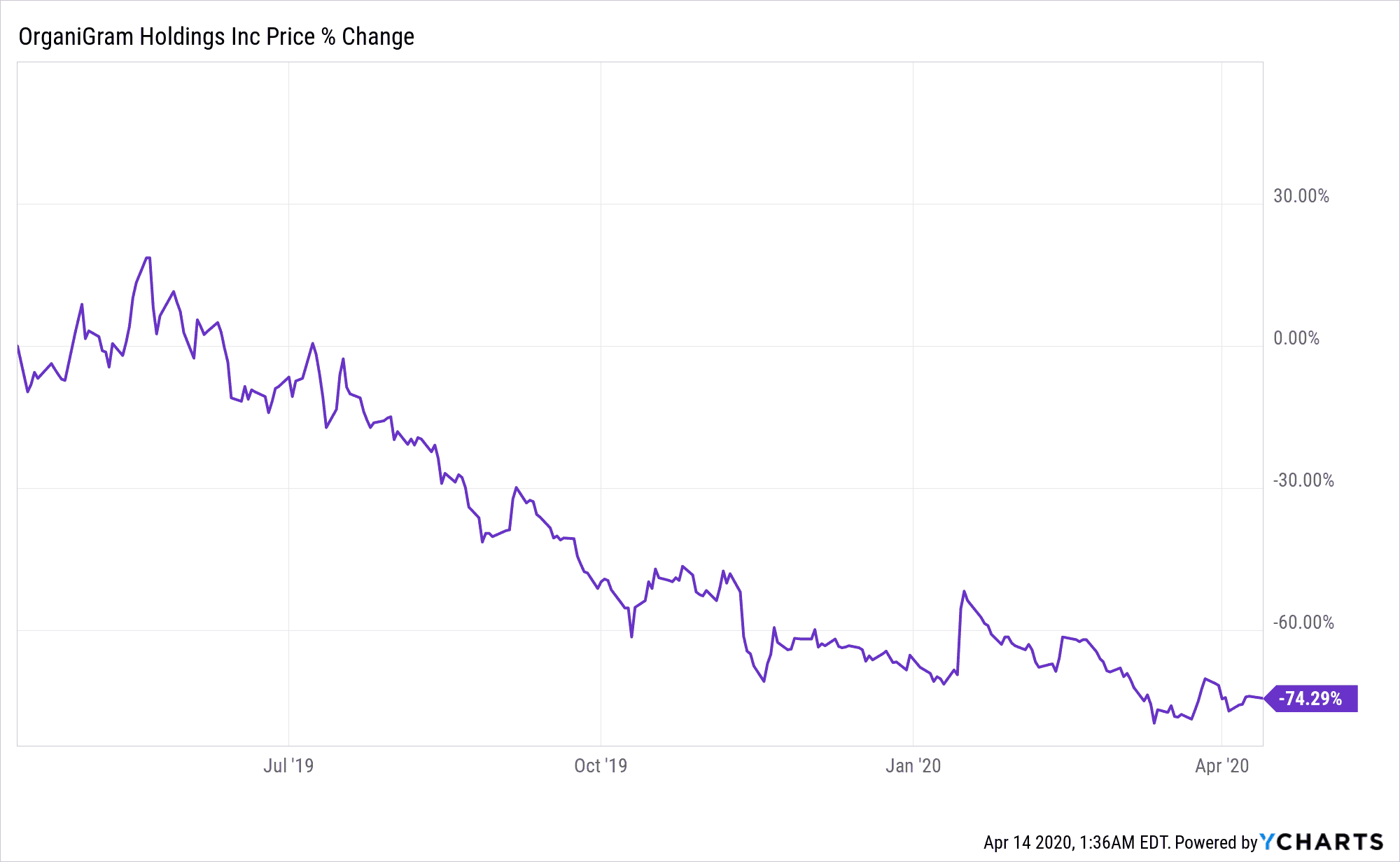

Although the stock has recovered slightly from its all time lows back in mid-march, it is still trading at levels very close to the all-time lows, coming in at just under $2 per share, which is a decline of over 70% from the same time last year.

OGI 1-Yr Price Change

Overall it’s a tough time for cannabis companies all around, but Organigram is clearly banking on its assortment of new products to play out well for them in the long run, although it may be too early to tell now.

The company ended the quarter with $41.2 million in cash and short-term investments.

Last quarter we reported on some potential issues that OGI could face including the falling price of cannabis and the company’s decision back in 2019 to issue 7 million new shares which diluted shareholders.

An analyst from Cantor Fitzgerald, Pablo Zuanic, has stated that he expects OGI’s margins to be under pressure in the near term due to higher marketing spend and start-up costs related to its new product lines.

This is clearly proven true as the company has increased operating costs by 49% quarter-over-quarter, coming in at over $15.8M which represented 60% of net revenue compared to 37% in Q2 2019.

The recent crisis surrounding the COVID-19 pandemic has also impacted OGI’s business.

Last week, the company announced that it has temporarily laid off 400 of its employees, representing 45% of its workforce, as part of COVID-19 containment efforts.

This may turn out to actually help profitability for now as cannabis sales are actually up in Canada, while OGI will have lower costs if only for a quarter or two.

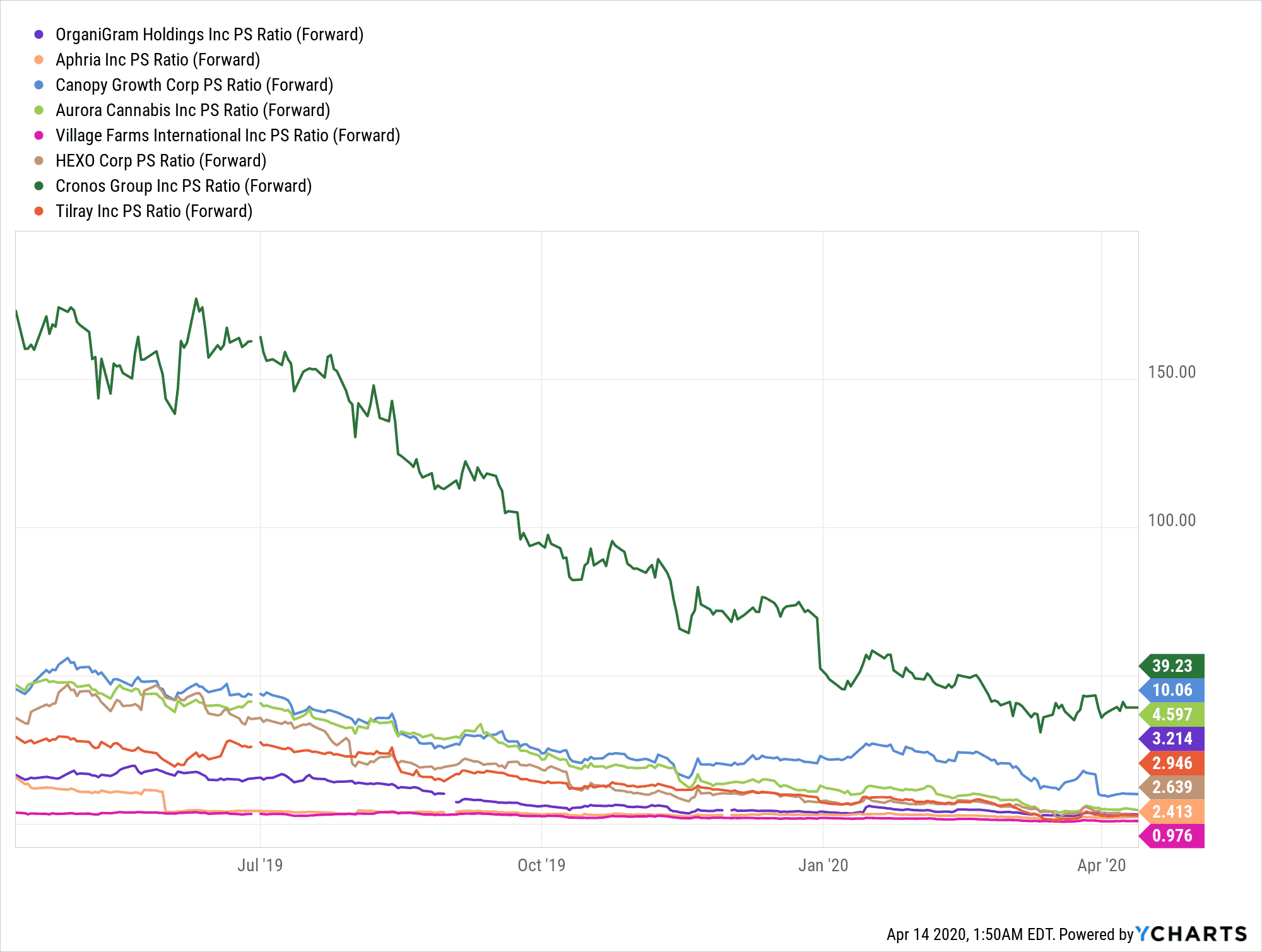

Even close to all-time lows, the stock is not particularly cheap, trading at 3.2x forward sales, 33% more expensive than peers like Aphria who do not have any cash problems.

Owning OGI here does not provide investors with any bargains.

Forward P/S Ratio Vs. Peers

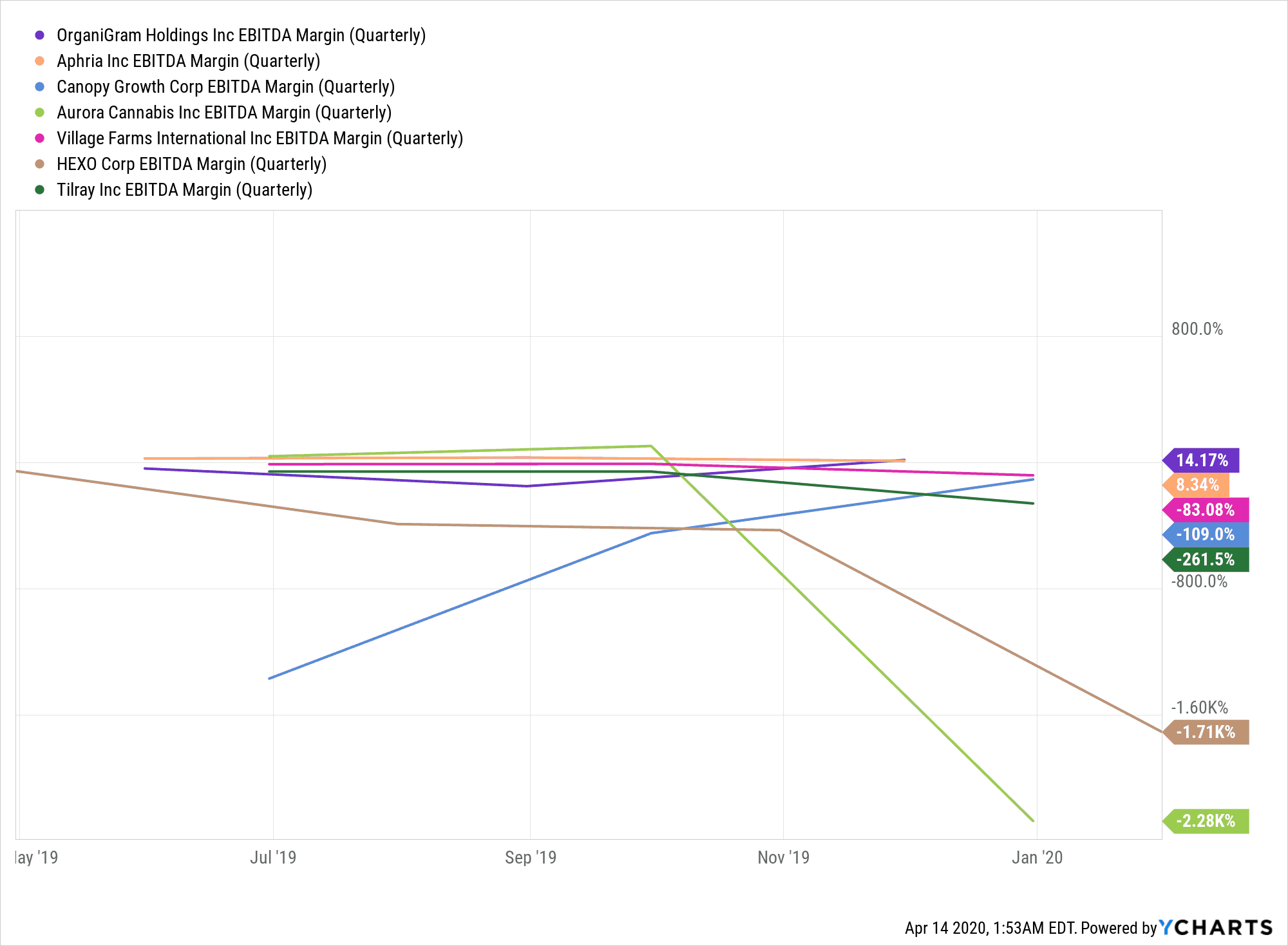

OGI’s EBITDA margin has been performing well against its peers for the past few quarters, although it has been going in the wrong direction for six months now.

The EBITDA margin was 40% a year ago, but due to startup costs and weak sales around cannabis 2.0, the EBITDA margin is now negative 28%.

EBITDA Margin VS. Peers

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.