Summary

Grizzle has produced the first truly balanced deep dive analysis of the Canadian marijuana sector. We lay bare all the inconvenient truths of this highly overvalued sector.

Euphoric retail and institutional investors have stratospherically bid up the sector, diving head first into rich equity offerings that will in aggregate allow licensed producers (LPs) to grow 2x the peak amount of marijuana this country will ever need.

We confront three inconvenient truths head-on:

1. Legalization of marijuana always equals price deflation

2. Black Market Inc. The biggest competitor no one wants to talk about

3. Extreme valuations are reminiscent of the 2010 rare earth bubble.

READ THE FULL REPORT BELOW OR DOWNLOAD THE PDF BY SIGNING UP HERE:

UP IN SMOKE – FULL REPORT

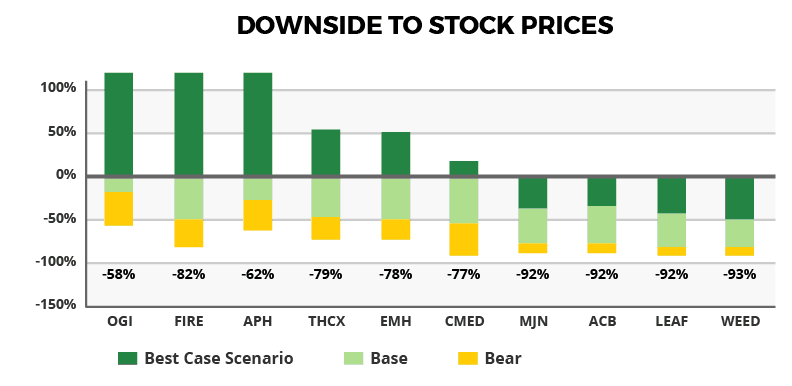

Downside of 65-90% for Canadian Licensed Producers

1. Legalization Equals Price Deflation

The marijuana oversupply is going to push retail and wholesale prices down by as much as 50% within 12 months of legalization. In every legal market, retail and wholesale prices peak near the date of legalization due to a lack of supply and then quickly begin to fall, driven down by new entrants into the market and a rapidly expanding production base. The ability to grow plants at home along with significant grey and black-market supplies puts a ceiling on prices even if Canada severely restricts production licenses.

2. Black Market Inc. the Biggest Competitor No One Wants to Talk About

The marijuana market is mature with black-market supply already exceeding demand (Canada exported 20% of marijuana production in 2017). Legal supply will have to successfully compete on price to take away market share. Stock prices are implying the impossible: that both stable pricing and exploding volumes can occur at the same time. You can’t have both in a mature commodity market.

3. Valuations Remind Us of the Rare Earth Bubble of 2010

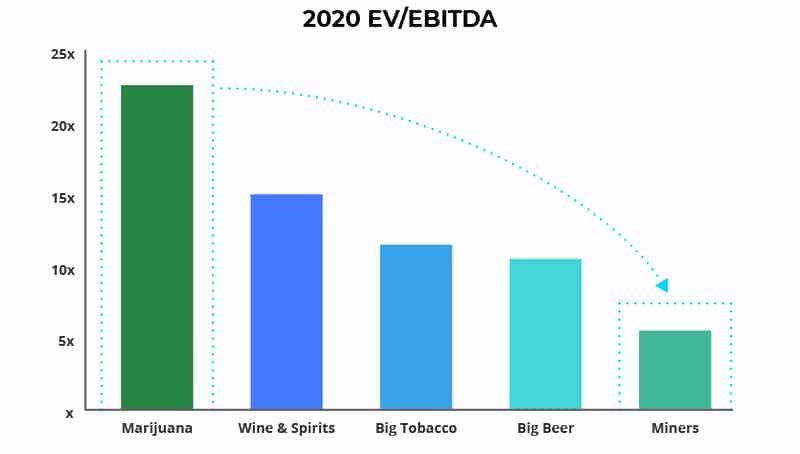

Marijuana stocks are trading on 2019-2020 EV/EBITDA multiples of 48x and 18x respectively, in the 98th percentile of multiples across all stocks in North America – implying extreme levels of overvaluation. The analyst community argues big tobacco, wine and spirits are the real proxies for the marijuana market, but at multiples of 11.5x and 15.0x EV/EBITDA respectively, they provide no valuation support at these levels.

IN THIS REPORT WE ARGUE THAT AN INDUSTRY LIKE MARIJUANA WITH LITTLE PRICING POWER AND MINIMAL BARRIERS TO ENTRY SHOULD TRADE MORE IN LINE WITH COMMODITY PRODUCERS AT 5-6X EV/EBITDA, REPRESENTING BASE CASE DOWNSIDE TO STOCKS OF UP TO 65%.

WHAT IS THE CATALYST THAT WILL POP THIS BUBBLE?

When extreme valuations are the central point of contention (as is the case for the marijuana sector), the market doesn’t need a specific catalyst to correct, all it takes is simply a change in the broad market psychology (profit taking / risk off) to correct hyper-inflated stock prices. The tepid market environment this week was an excellent case study in highlighting how quickly investors unload marijuana stocks in a risk-off environment.

Even if the market euphoria continues, we think the point of no return is fast approaching. Historically, retail prices peak 1-6 months after the date of legalization and consistently decline thereafter. This points to a window of late 2018 to early 2019 when prices will begin falling faster than analysts and the government expect, driving revenue and earnings misses from the marijuana stocks. If prices don’t decline, legal volumes will stagnate as consumers keep buying from the black market, causing earnings misses as well.

IF THE MARKET ANTICIPATES THESE RISKS 6 MONTHS IN ADVANCE, AS IT USUALLY DOES, THE STOCKS ARE MEANINGFULLY EXPOSED TO EXTREME DOWNSIDE NOW.

DEMAND

How Large is the Marijuana Market in Canada?

To estimate demand, we need to know how much Canadians consume and how often. Official usage data in Canada is limited, but combining statistical data from both the Parliamentary Budget Office (PBO), the state of Colorado and the U.S. government, we can arrive at a reasonable assumption.

PREVALENCE

In Colorado, 16% of the population consumes marijuana annually, according to a national survey on drug use. The PBOC estimates 12% of Canadians have used in 2015, and the rate of use will increase to 14% by 2021. Looking at a histogram of smoking prevalence, we see Canadians smoke less heavily than their counterparts in Colorado, supporting the view that less of the population will ultimately become smokers compared to Colorado.

USAGE PER DAY

Using smoking prevalence rates from the U.S. National Survey on Drug Use and Health (NSDUH) and reported grams consumed on days of use, we arrived at an average usage rate of 0.5 grams per day for the average user in Colorado. The PBOC study in Canada found similar daily usage rates.

FINAL DEMAND

Applying 0.5 grams per day to the estimated 4.7 million midpoint of Canadian users in 2018, we arrive at total market demand in Canada (medical and recreational) of 860,000 kg per year, growing to 1,000,000 kg by 2021. This estimate is generally in line with the analyst community and government sources.

SUPPLY

The Canadian Market is Already Oversupplied

Demand numbers look significant, but the black market is already supplying more marijuana than Canadians can consume. According to Statistics Canada estimates, Canada’s net exports of marijuana were $900 million in 2017. The cannabis market is oversupplied by almost 20%. This means the black market is likely producing almost 900,000 kg/year, which is enough to meet even the highest demand estimates for the legal market in 2018.

BY 2021, CANADA COULD BE PRODUCING 1,900,000 KG/YEAR WHEN ONLY 1,000,000 KG/YEAR IS NEEDED. THIS IS A LEVEL OF OVERSUPPLY THAT WILL TAKE YEARS TO WORK THROUGH AND WOULD BE CRIPPLING FOR MOST, IF NOT ALL, COMPARABLE AGRICULTURAL SECTORS.

Legal Producers (LPs) are Pretending the Black Market Doesn’t Exist

Legal producers are rapidly expanding to increase capacity and meet potential legal demand. Looking at only the top 10 largest producers, they will have fully operational capacity of at least 650,000 kg by 2019, equal to 75% of demand. By 2021 legal supply will equal or exceed consumer demand. Additionally, most legal producers have land they already own right next door to greenhouse space that could easily add another 400,000 kg of annual supply in a 1-2 year period, if needed.

LPs Can Easily Pay for New Capacity With Equity

Building enough greenhouses from scratch to supply peak Canadian demand of 1,000,000 kg/year only costs $1.8 billion. The current market cap of the top 10 producers is over $21 billion and they have $2.5 billion in cash alone, enough capital to supply 2x the peak Canadian demand. This sector is a textbook case of overcapacity.

Bottom Line

Canada is about to be flooded with marijuana. Legal producers are building capacity quickly and will have to engage in a price war with the black market to win the market share they need to satisfy investor expectations. Either prices are going to fall significantly or volumes will stagnate. Neither is good for stock prices.

PRICES: HOW LOW CAN THEY GO?

The Path of Wholesale Prices Has Only One Trajectory. Down.

After doing a deep dive on the history of the U.S. recreational market, we think wholesale Canadian prices are going to follow a very similar path. The Canadian market structure is almost a mirror image of Colorado prior to legalization.

The Canadian government has no limit on the number of licensed producers with 74 approved so far and 208 producers under final review for approval, according to the federal government2. There’s also a waiting list of at least 1,000 more going through the approval process. Even if a few large growers emerge as the dominant players, they still must compete on price with the black and grey markets if they want to capture a significant chunk of recreational and medical demand.

Looking at the wholesale prices of the three legal recreation states in the U.S., we see prices are in freefall as the industry matures. Marijuana in Colorado sold for as low as $2.64/gram in the summer of 2017 with the low end of deals happening at only $2.20/gram. Washington wasn’t much better at $3.08/gram. Oregon is the only state to hold up, but marijuana was only legalized there in late 2015 and there are still legal supply shortages in 2017.

Market expectations for retail prices are wildly optimistic

Analyst’s stock valuations are being driven by assumptions of a $7-$8/gram retail price, down only 10% by 2021. [This is roughly in line with the Parliamentary Budget Office outlook for the same period.3]

LOOKING AT THE TWO MOST MATURE LEGAL STATES IN AMERICA, COLORADO AND WASHINGTON, RETAIL PRICES HAVE FALLEN BETWEEN 33%-70% IN THE THREE YEARS SINCE LEGALIZATION.

Recreational marijuana was legalized in Colorado in January 2014. With over 3 years of operational history, the Colorado legal market is the most mature in North America. Using pricing data from 30% of dispensaries and over 2,000 individual flower prices a few months into legalization, the recreational price averaged $16/gram and was a quarter of total sales in the state. On the medical side prices averaged $9/gram, below recreational marijuana due to tax differences. Medical sales made up three quarters of total marijuana volume sold for a blended medical and recreational price per gram of $12.65.

Supply was still scarce in the early days of the legal market and was not keeping up with demand. As a result, there was a scarcity premium built into the prices as there likely will be in the early days of legalization in Canada also.

Colorado Marijuana Prices in the Early Days of Legalization

Fast forward to 2017. From the per gram data available in the chart below, recreational prices have fallen over 56% in 4 years to $6.92/gram and ended 2017 at only $5/gram, according to BDS Analytics, while the medical price is down 53% to $4.20/gram, which also saw the same price compression. Even though some buyers are willing to pay a premium for certain strains, competition is still driving the average retail price down day after day after day.

Washington

Prices in Washington fell 2% a month on average since legalization and are now down 70% in 3 years.

BUT IT GETS WORSE. THE FUNDAMENTAL STEADY STATE PRICE OF BOTH WHOLESALE AND RETAIL MARIJUANA IS MUCH LOWER THAN WHERE PRICES TRADE TODAY.

WHOLESALE PRICES

Cash Costs

The publicly traded LPs in Canada grow marijuana for about $1.00/gram. This reflects all costs including labour, energy and raw materials to bring the plant to harvest. Testing, oil production and packaging adds another $0.50/gram while shipping to individual customers costs an additional $1.25/gram for an all-in industrial cost of $2.75/gram. Once LPs begin selling mostly to government-owned stores or in bulk to retail locations the shipping cost will likely fall by approximately $0.50, bringing the total cash cost to ~$2.00/gram.

Capital Costs

The publicly traded LPs can build greenhouses for $1.80/gram of capacity. At current prices, an apartment-sized greenhouse could recoup its initial investment in 4 months and after expenses would start making 3x the money spent to build the greenhouse annually. That is a return of 300%. Longer term we assume this industry’s cost of capital will be in line with other commodity producers at around 10%. The ultimate equilibrium price for marijuana will be where the return on investment equals the cost of capital.

TO ACHIEVE A 10% RETURN ON YOUR INITIAL STARTUP CAPITAL, THE PRICE OF WHOLESALE MARIJUANA WOULD ONLY HAVE TO SELL FOR $2.69/GRAM. $2.69/ GRAM IS STILL ENOUGH PROFIT FOR THE GROWERS TO STAY IN BUSINESS, MEET DEMAND AND KEEP THE LEGAL INDUSTRY IN BALANCE. This price looks very possible compared to wholesale prices in the U.S. that have traded as low as $2.20/gram.

RETAIL PRICES

Based on our research, a realistic estimate for the startup costs of a retail dispensary is around $100,000 with $50,000 of inventory (30lbs a month of sales) and another $50,000 for licensing fees and startup costs. FOR A RETAILER TO MAKE A 10% RETURN ON THEIR $100K INVESTMENT THE RETAIL PRICE OF MARIJUANA WOULD ONLY HAVE TO BE $4.35/GRAM. Again, we can back up our estimate with data from Colorado where medical marijuana was selling for close to $4.20/gram in 2017 and is still 50% of the legal volumes sold.

The Ability to Grow Marijuana at Home Creates Another Ceiling for Price

First-hand evidence we collected from novice home growers in Colorado and California point to a home grow cost of only $0.57/gram, compared to a retail price of ~$8.30/gram in Canada. Experienced home growers have costs closer to $0.35-$0.40/gram.

A HOME GROW COST OF ONLY $0.57/GRAM WOULD SAVE THE AVERAGE CANADIAN CONSUMER $4,500 OFF RETAIL IF THEY GREW 4 PLANTS. These are big savings for the average smoker. The median income in Canada for an individual is $27,600, so the savings from a home grow is equal to 16% of yearly earnings.

$0.57/GRAM MAY SEEM CHEAP, BUT PRICES COULD EASILY BE EVEN LOWER. A study by the Drug Policy Research Center found that growing marijuana outdoors easily achieves a yield of 575 pounds of flower per acre, which is a cost of only $0.02-$0.08/gram depending on the all-in cost per acre. Yes, you read that right, $0.02 a gram. If laws change over time to allow outdoor growing at scale, the overall cost structure could fall dramatically, putting additional downward pressure on retail and wholesale marijuana prices.

Supply and Demand Aren’t the Only Risks to LP Pricing

PRODUCT DIFFERENTIATION IS GOING TO BE VERY DIFFICULT WITH GOVERNMENT LABELING AND MARKETING RULES

LPs are going to have a very difficult time differentiating themselves and charging premium retail prices when over ~70% of the Canadian population will likely be buying their marijuana through government run and regulated channels (Ontario, Quebec, Manitoba and online sales in Alberta). Marijuana labeling rules across Canada will largely require opaque bottles and uniform product labeling, making it difficult for consumers to tell the difference from one product to another.

Government buyers will drive a hard bargain one way or another

Proposed legislation will see up to 70% of the population required to buy marijuana through government-controlled channels: Ontario, Quebec, Manitoba and online sales in Alberta. The government’s second most important mandate after public health is to transfer demand from the black to the legal market. However, if legal marijuana isn’t competitive with untaxed illegal supply, government stores will have no buyers. This outcome is looking likely on day 1 of legalization with street prices currently below legal prices and the government hasn’t even enacted the proposed $1/gram excise tax.

If legal supplies aren’t selling, the government will then have to bring down retail prices to drive legal volumes. And it will be legal producers, not the government, who will be taking a hit on margins. Every $1/gram price cut would hit producer margins by 10%.

The Bottom Line for Retail Prices

In a completely free market, LPs are going to have to consolidate the market quickly and find ways to differentiate their products or else competition will grind retail prices down 50% or more over the next few years. The analyst community thinks prices will only fall 35% at most by 2021, so the stock prices have massive downside to them if retail prices fall 45%- 60% in the next year or two as we expect.

The black market also has the advantage of avoiding an almost 20% tax on legal supply, providing a cost advantage that increases the lower prices due to the flat $1/gram excise tax proposed by the government and the 13% sales tax. Even if we see a rapidly consolidating industry, the legal producers still need to undercut the black market on prices to achieve their sales volume targets and avoid disappointing investors. The direction of prices is down.

RARE EARTH BUBBLE PART DEUX: MULTIPLES ARE THROUGH THE ROOF

So What Was the Rare Earth Bubble?

The rare earth bubble was a short-lived investor mania in 2010 driven by the Chinese government’s decision to limit exports of rare earth metals. China mines most of the supply of rare earth metals worldwide, so this decision caused a spike in prices. North American rare earth company stock prices and valuations went parabolic as investors believed prices would stay high forever. Rare earth miners raised money frantically to increase capacity as fast as possible. Ultimately, businesses found ways to use less rare earths in their manufacturing processes and the Chinese government relaxed export restrictions, causing rare earth prices to crater. Molycorp, the rare earth poster child, is a cautionary tale of what can happen to a stock when expectations run far ahead of reality.

What is the Right Multiple for Marijuana Stocks?

We argue that for an industry with no pricing power the multiple should at best be in line with oil and gas producers or diversified miners at 4x-6x. But realistically, this is a farming business with minimal profitability and significant volatility in earnings, deserving an even lower multiple. There’s a dearth of publicly traded farming companies for a reason.

When thinking about the right multiple we need to judge the industry on three factors:1) Pricing power 2) profitability and 3) barriers to entry.

1) Pricing power

Do marijuana companies control the price of the product and can they raise prices without customers switching to the black market, growing at home or quitting use of the product altogether.

The answer is a resounding no. The industry has no demonstrated pricing power. There are 74 licensed producers in Canada, over a thousand applications in process and 208 applications in final review, according to the federal government4. The government does not limit the number of players in the space so if one producer decides to raise the price of marijuana, there are 73 other cheaper options to choose from. The low startup costs to home growing, government labeling and marketing restrictions, and a well-developed black market create serious challenges to maintaining market share and pricing.

With the cost of farming continually falling as the industry’s growing practices become more sophisticated, growers can offer lower street selling prices and still maintain the same profitability. Yet another reason marijuana prices will only go in one direction, down.

2) Profitability and growth

The more cash a company generates at the end of the day, the higher the multiple should be. Internet giants like Facebook and Google have very high margins (50-60% EBITDA margins) and because of this they trade on multiples of 19x and 14x. Grocery stores, on the other hand, operate with razor-thin margins of 4-5% and it shows in their multiples (3.8x on average).

Legal producers are growing marijuana for ~$2.35 and selling it for $8.21 on average. That’s a gross margin of 70%. Too good to last. These margins are even higher than big tobacco at 60%, and big marijuana is still far from the oligopoly structure of big tobacco. Big tobacco operates in an industry with significant brand awareness built over decades of advertising and marketing. They sell a product that is incontrovertibly addictive with amazing pricing power and they operate in a highly consolidated industry with only 6 players controlling the entire global market.

In contrast, the marijuana industry has built no brand awareness and sells a product that some may argue is habit forming, but is nowhere close to as addictive as nicotine in cigarettes. The industry is still wide open to competition and has the added threat of home growing and the black market to keep a cap on prices.

3) Barriers to entry

Canada has higher regulatory barriers to entry than the U.S. due to the slow approval time of licenses, but in the last 9 months license approvals have picked up dramatically with 36 new production licenses granted compared to only 44 outstanding prior to May 2017. As of December 1st, 2017, 208 more licenses were in the final stages of approval, according to the government.5

Barriers to entry are extremely low due to the minimal startup capital needed to start a competing legal production business. On an industrial level, a cultivation and sale license in Canada costs less than $5,000 and will likely fall further. In Colorado, license fees started at $22,000 in 2014 and are now down to $7,300. Greenhouse startup costs are also low,

$5,000 to build enough indoor capacity for 20 regular clients, anyone who can obtain a production license can easily start pricing their product cheaper than competitors to steal away clients.

At the consumer level, barriers are even lower. All you need is $50 per plant for the seedling, potting soil, clippers and a pot, and you have your very own marijuana supply. BARRIERS TO ENTRY DO NOT GET MUCH LOWER THAN THIS.

The market is pricing marijuana stocks like they are highly profitable enterprises, with strong pricing power, high barriers to entry and significant intellectual property, in perpetuity. In reality, none of these characteristics are true now, or will be true in the future. Don’t confuse marijuana with big tech, there is no intellectual property to be found in this industry.

A Quick Note on Commodities

Marijuana flowers are a commodity. A commodity is something widely available and unspecialized. One lump of coal is the same as any other, just like oil, copper, coal, tomatoes and many other agricultural goods and metals.

Even though the THC content and strain can vary, as long as the knowledge and technology to grow specific types are freely available (which they are) then all marijuana is a commodity. Even when marijuana is refined into oils or gel caps the technology to make these new products is easily available to all, so the commodity label still applies.

Multiples Matter

To see how big a difference the multiple makes, here are the implied stock prices for the top 10 marijuana producers when we use a 15x multiple in line with wine and spirits manufacturers, 11x in line with tobacco producers and, finally, a 5.5x multiple in line with commodity producers globally.

Legal vs. Black Market: The Battle for Market Share

The analyst community talks about supply and demand as if the marijuana market was brand new. What they fail to mention is that supply already meets demand in the Canadian market. Way back when legalization was only a pipe dream, the black market was successfully supplying consumers and still does today. We estimate the black market has a 98% market share in Canada as of YE 2017. For the legal producers to dominate the market as the stock prices imply, legal marijuana will have to be priced competitively with the black and grey markets, and even then, legal supply could struggle to gain market share.

Looking at a government study that collected 9,000 anonymously reported street purchases on Price of Weed from 2011-2015, we can see the black-market price has been relatively stable, demonstrating reliable and sufficient supply from illicit growers.

Proposed government tax rates will push legal prices above the black market, keeping consumers from buying legal marijuana

Data from the recent PBOC report showed illicit marijuana prices are in line with the legal medical market as of 2016. However, the government is planning to impose a $1/gram excise tax, which at the current medical price of $8.30 is equivalent to a 12% duty. An all- in legal price of $9.30 per gram puts legal marijuana well above the midpoint of the illicit market. Recent street prices, according to Price of Weed and Statistics Canada, are selling for $7-8/gram, 20% below future legal prices.

The government itself admits that only 60% of the population at most would be willing to pay over a $1/gram more for legal vs illicit marijuana.

The government also admits that legalization will bring about falling prices in the illicit market as the risk premium for operating in an illegal industry is no longer justified:

“Ultimately, PBO believes that average illicit cannabis prices will face downward pressure when legalization occurs. Profit margins for illicit cannabis are thought to be high, so as to compensate producers and sellers for the risk premiums in engaging in an illegal activity.

With legalization, and particularly in the absence of strong enforcement, of the illicit market the risk premiums will be lower. This will encourage prices to fall. Illicit market actors may also be compelled to voluntarily reduce their margins to compete with the legal market and protect market share.” – PBO Marijuana report, November 2016

If black-market prices are already cheaper than after-tax legal supply, and are expected to fall even further, what rational consumers are going to buy legal?

The legal market in Canada is going to see one of two outcomes:

- Retail prices fall significantly like in Washington as legal supply ramps up, driving black market buyers to the legal market and benefiting legal

- Rapid consolidation or government limits on licenses will keep pricing relatively high, but consumers will choose cheaper black- market marijuana over the expensive legal varieties, leaving legal volumes to stagnate potentially for

EITHER OUTCOME IS MUCH MORE BEARISH THAN STOCK PRICES ARE EXPECTING, ALMOST ASSURING EITHER PRICING OR VOLUMES WILL DISAPPOINT, CRUSHING STOCK PRICES IN THE PROCESS.

MEDICALLY SANCTIONED GROW- OPS PROVIDE ANOTHER BIG SOURCE OF SUPPLY TO COMPETE WITH THE LEGAL MARKET

Individual grow-ops are already having a significant impact under the current medical marijuana laws in Canada, according to a recent data release from Health Canada.

According to the data, there are 600 “supergrowers”, people who have obtained prescriptions, allowing them to have at least 244 plants and 35 kg of dried bud on hand at any one time. This is far more than one person could smoke in a year, but is currently still within the law. From a recent newspaper expose in the Globe and Mail6 we know some of these supergrowers are growing far more than they are legally entitled to possess.

Even if we assume each supergrower is following the rules and growing only 244 plants at a time, this would amount to almost 18,000 kilograms of production. These greenhouse operations are likely able to fit 4 growing seasons into a year, leading to a total production impact from supergrowers of up to 70,000 kilograms a year. PEOPLE WITH ONLY 6% OF THE MEDICAL MARIJUANA LICENSES ARE GROWING MORE MARIJUANA THAN THE CURRENT PRODUCTION OF THE TOP 10 LARGEST LEGAL PRODUCERS IN CANADA.

The government must commit to cracking down hard on the illegal industry and on medical loopholes or else legalization will only make it easier for the grey market to continue supplying consumers and undercut fully taxed legal prices.

Pharmaceutical Demand Will Not Save the Industry

Analysts and investors often point to the potential of marijuana as an over the counter pain medicine akin to Tylenol or Ibuprofen as a reason demand could explode, justifying revenue targets and multiples and maintaining premium prices.

The potential for pharmaceutical use of marijuana is very real with prescription spending in Canada 4x as large as marijuana spending. However, prescription and non-prescription pain medicine sales are only $300 million of the $40 billion spent on prescription medicine in Canada.7 Not as large an opportunity as originally thought.

Production Costs of CBD are Still Too High to Compete With Mainstream Pain Medicines

The active ingredient in Tylenol, acetaminophen, only costs $0.22/gram to buy at retail (50 grams costs $11 at the pharmacy). Contrast this with the active ingredient in marijuana used for pain management, CBD. It generally takes 5-6 grams of dried material to produce 1 gram of 95% pure CBD oil. The cost of dried plant matter alone to produce a gram of CBD oil, not even including the cost of extraction and processing is $12/gram, while the selling

price at retail is over $100/gram. Regardless of how effective a gram of CBD is compared to acetaminophen, the industry is going to have to make breakthroughs in growing and manufacturing practices to compete on price with currently available pain medications. Pharmaceutical grade marijuana is still years away from mainstream adoption.

CONCLUSION: THE RISKS ARE SIGNIFICANT

The Canadian cannabis sector has all the hallmarks of a classic commodity stock bubble: euphoric investors, outspoken promoters and extreme valuations. Even if legal producers can meet their ambitious capacity targets, bring cash costs down 30%, sell marijuana for

$7/gram (down only 5% from today), and trade on a tobacco company multiple (11x), there is zero upside in legal producer stocks overall.

EXPLAINING THE 3 CASES

Upside Case

$7/gram retail price, 42% EBITDA margins, capacity in line with management guidance and an 11x EV/EBITDA multiple.

Base Case

$4.50/gram retail prices, 42% EBITDA margins, capacity in line with management guidance and a 5.5x EV/EBITDA multiple

Downside Case

$4.50/gram retail price, 20% EBITDA margins, capacity in line with management guidance and a 5.5x EV/EBITDA multiple.

The larger the future capacity the more overvalued the stock.

Buying stocks that are priced for perfection is rarely a path to riches. Buyer beware.

DISCLOSURE

Grizzle publishes the highest quality investment research and analysis. Our research is backed up by hard data. Our focus is to identify tangible investment opportunities with meaningful upside for our readers. We stand by our rigorous analysis and always put our money on the line. This means we may take a position for or against the securities featured in this report after we have completed our research. With that said, here are some important additional legal disclaimers:

You agree that the use of Grizzle is at your own risk. In no event should Grizzle be liable for any direct or indirect trading losses caused by any information available on this site.

The materials on the site are not an offer to sell or a solicitation of an offer to buy any security, nor shall any security be offered or sold to any person, in any jurisdiction in which such offer would be unlawful under the securities laws of such jurisdiction.

Grizzle makes no representations, and specifically disclaims all warranties, express, implied, or statutory, regarding the accuracy, timeliness, or completeness of any material contained in this site. You should seek the advice of a security professional regarding your stock transactions.

1 “Cannabis Stats Hub”. Statistics Canada

2 LeBlanc, Daniel, “Ottawa to More than Triple Cannabis Licences to Boost Production”. The Globe and Mail, 19 Dec. 2017 3 “Cannabis Stats Hub”. Statistics Canada

3 LeBlanc, Daniel, “Ottawa to More than Triple Cannabis Licences to Boost Production”. The Globe and Mail, 19 2017

4 McQuigge, Michelle, (The Canadian Press) and Armina Ligaya. “Health Canada Nearly Doubles Number of Marijuana Production Licences in Second Half of 2017.” com, 20 Dec. 2017

5 Hayes, Molly and McArthur, Greg. “Personal Marijuana Grow-Ops Emerging as Targets for Organized Crime, Globe Investigation Finds.” The Globe and Mail, 1 2017

6 Prescribed Drug Spending in Canada, 2016, Canadian Institute for Health Information

7 National Health Expenditure Trends, 1975 to 2017, Canadian Institute for Health Information

GET OUR LATEST MARIJUANA INVESTMENT RESEARCH FOR FREE

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.