Investor attention on emerging markets normally focuses for good reason on economic success stories like China and India. But this writer recently visited for the first time Pakistan which has gone to the IMF 13 times in the past 30 years. With such a track record expectations were naturally low. It was therefore interesting to learn of the resilience of the country’s private sector with debt concentrated very much at the government level.

Minimal Debt Points to a Strong Recovery

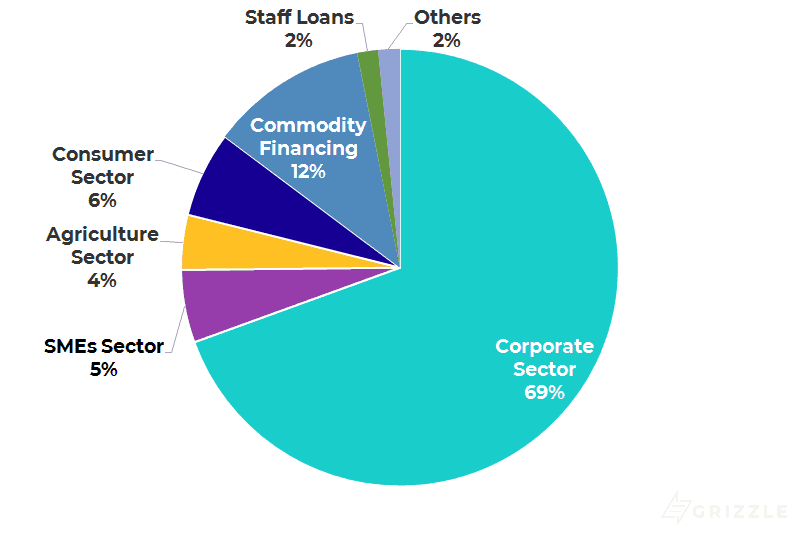

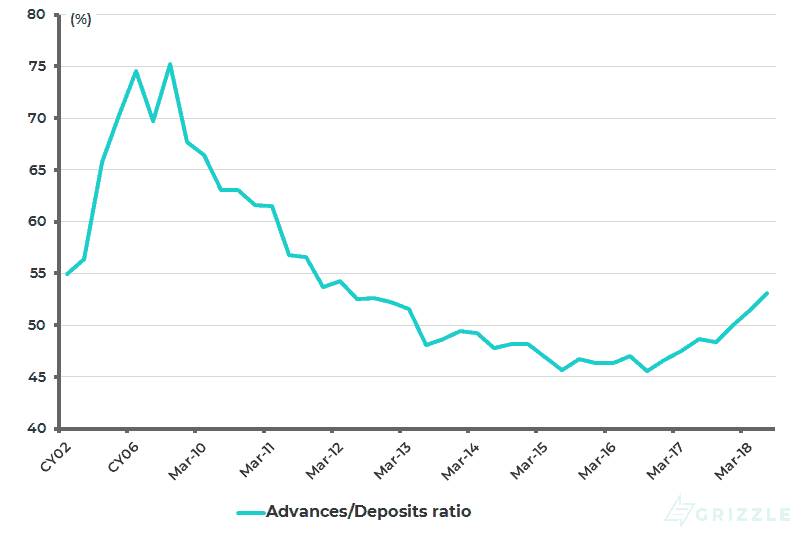

Consumer loans and SME loans accounted for only 12% of total bank loans (PKR498 billion and PKR422 billion respectively) at the end of 2Q18, while the loan-to-deposit ratio of the banking system is only 53%, down from 75% in 2008 (see following charts). Meanwhile, 69% of bank loans are to the corporate sector. But it is not leveraged, with corporate debt totaling only 16% of GDP.

Pakistan gross advances by segment (End 2Q18)

Pakistan loan-to-deposit ratio

The lack of private sector debt is important since it means the economy can recover quickly from its latest crisis once the current hole in the balance of payments is plugged, as is likely to be the case by a combination of China and IMF funding, combined with some extra support provided by Saudi Arabia. Pakistan secured last month a US$3 billion direct deposit and a US$3 billion deferred oil payment facility from Saudi Arabia. This US$6 billion package amounts to about half of Pakistan’s FY19 estimated net financing gap.

The risk here, of course, is that the Trump administration politicizes the latest IMF negotiation as regards Pakistan, as it has threatened to, by making the China-Pakistan Economic Corridor (CPEC) an issue.

Pakistan Riding High on the One Belt One Road

Pakistan is so far the major beneficiary of China’s so-called One Belt One Road (OBOR) program. But this risk was greater two or three months ago given that Donald Trump now looks like he wants to meet Xi Jinping at the G20 Summit in Buenos Aires at the end of this month. This time the request is for about US$6-8 billion from the IMF to fill the gap this year and next.

The IMF team has been in Islamabad, Pakistan’s capital, since Nov. 7. It is also the case that a significant part of a classic macroeconomic adjustment has already taken place with the Pakistani currency, the rupee, having depreciated by 21% against the US dollar since Dec. 2017 to PKR134/US$, while interest rates have been hiked by 275bp to 8.5% (see following chart). The new government, elected in August, has also increased average tariffs for electricity and gas by 11% and 30% respectively.

State of Pakistan policy rate and Pakistani rupee/US$ (inverted scale)

The Economics of Pakistan

Most observers expect around another 5% depreciation of the currency and perhaps another 150-200bp of rate hikes, though the magnitude will primarily be influenced by external developments such as the trend in the US dollar and the oil price. Like its neighbour India, Pakistan is also dependent on imports for its energy consumption.

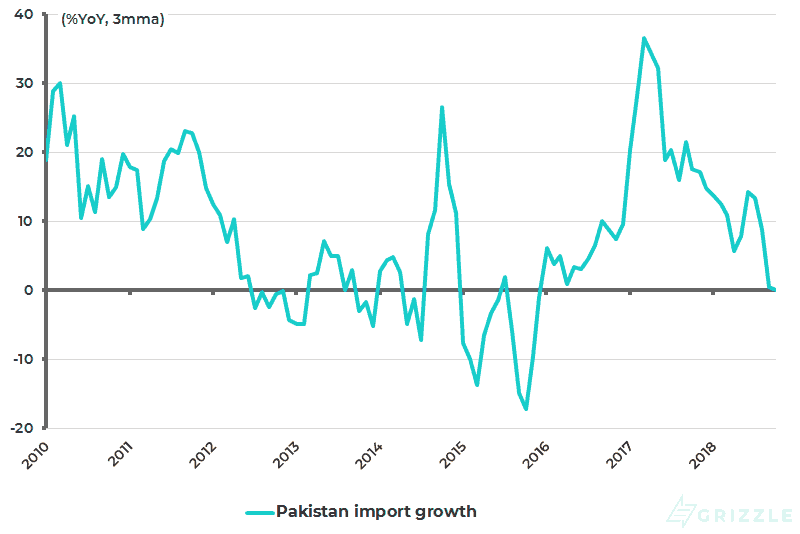

The good news is that import growth is now slowing as the weaker currency impacts. Imports of goods declined by 1%YoY in October in US dollar terms and were up 7.6%YoY in the first ten months of 2018, compared with a 22.3% increase in 2017 (see following chart).

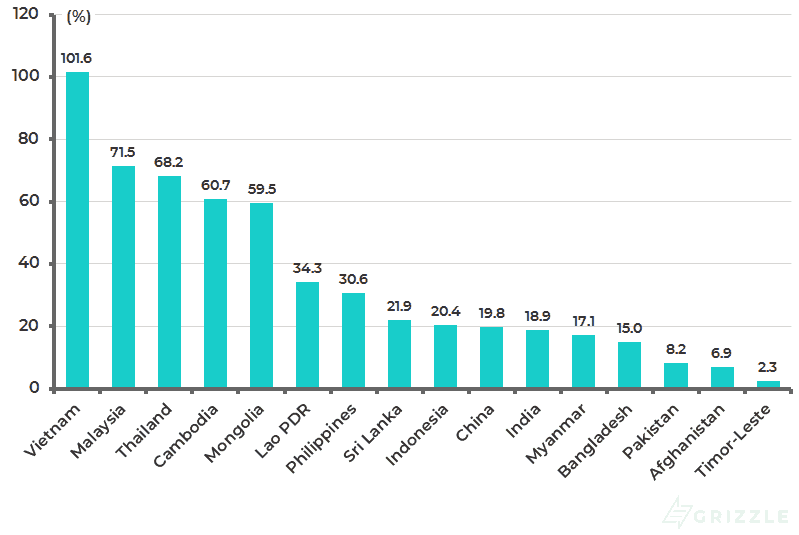

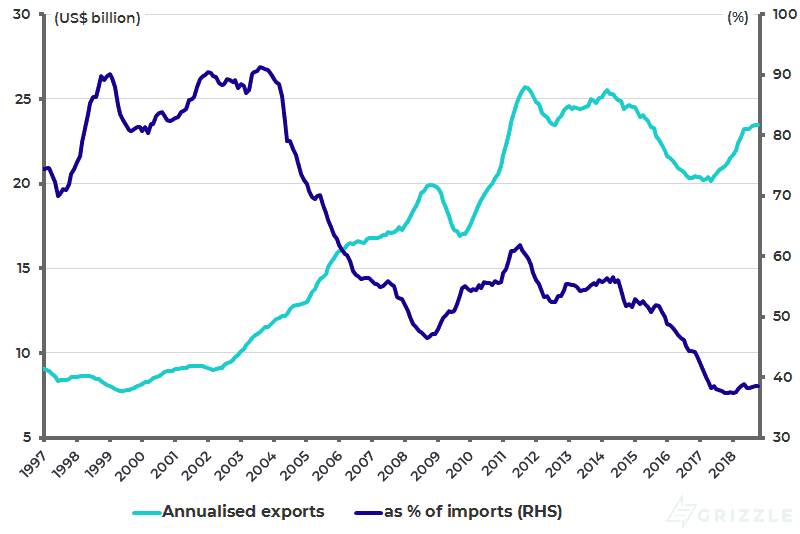

The bad news is that Pakistan suffers from a chronic lack of exports which is why it keeps having these balance of payments crises. Indeed exports of goods and services as a percentage of GDP were only 8.2% in 2017, among the lowest in the world (see following chart). Exports of goods have been relatively static since 2011 running at around US23 billion a year (see following chart).

Pakistan import growth

Exports of goods and services as % of GDP

Pakistan annualized exports as % of annualized imports

Pakistan’s Trade Issues

As a result, exports finance less than 40% of imports (mostly energy and capital goods), leading to the periodic balance of payments crises. It is generally agreed that a doubling of the exports by an additional US$20 billion would go a long way to solving Pakistan’s chronic balance of payments problem in an economy where private consumption accounts for 82% of nominal GDP.

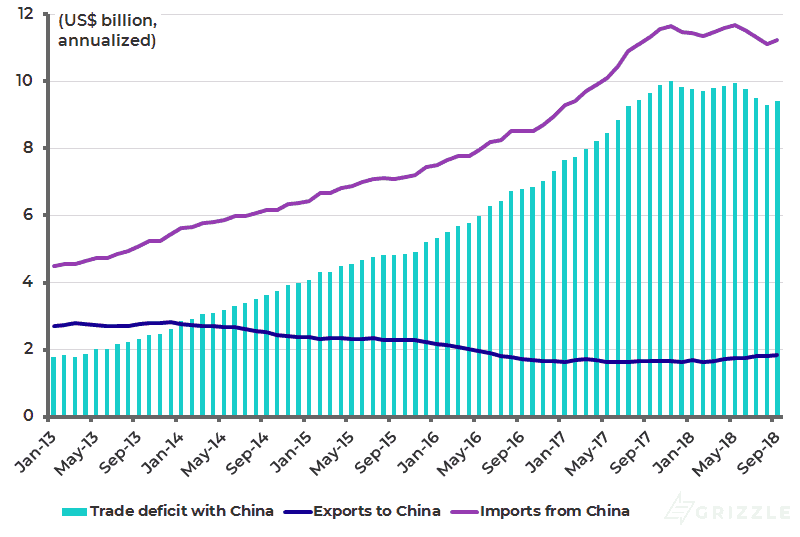

The need to boost exports is where China comes in. Meetings in Karachi suggest that the next stage of CPEC, after the infrastructure build of the past three years, will see Chinese investment more focused on setting up production in special economic zones and on investing in agriculture, an area where China sees huge potential given the lack of modernization. It is also the case that a further deterioration in the US-China trade relationship if it happens, in terms of the implementation of the threatened tariff increases in January, would probably benefit Pakistan. This is because it is likely to accelerate plans to move low-cost production to Pakistan.

For now at least Pakistan has not really benefitted from CPEC from a trade perspective. In fact, Pakistan’s annualized trade deficit with China has surged from US$1.8 billion in early 2013 to US$10 billion in late 2017 and is now US$9.4 billion (see following chart).

Still in the ‘big picture’ China has pledged to invest US$60 billion in Pakistan under the CPEC program for clearly strategic as well as economic reasons, and therefore has every incentive to try and make Pakistan work. On that point, the word is that the new government of Prime Minister Imran Khan was given a list of things to do on the official visit to Beijing earlier this month. This is important since the new party in power, the Pakistan Tehreek-e-Insaf (PTI), has never been in government before and therefore lacks practical experience.

Pakistan trade with China

What about the stock market? The attractive point is low valuations and high dividend yields. The market is on 6.9x forecast calendar 2019 earnings based on a universe of 47 stocks and a 2019 forecast dividend yield of 8.2%. Meanwhile, from a flow of funds perspective, foreign investors have sold a net US$1.58 billion since 2015 (see following chart). This is a combination of both Pakistan going from a 9% weighting in the MSCI Frontier Index to a minnow in the MSCI Emerging Markets Index (0.1%), and rising bearish sentiment ahead of the devaluation and related monetary tightening.

Foreign net buying of Pakistan equities

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.