The advice here remains to stick with the “back to normal” trade despite the scare over the mutating virus in Britain which has increased nervousness in recent weeks as regards the pandemic.

To state the obvious, viruses mutate all the time and, so far as this writer can tell, there is no concrete evidence as yet that this new version is more dangerous or that it will render the vaccines ineffective.

Meanwhile, the vaccine rollout continues.

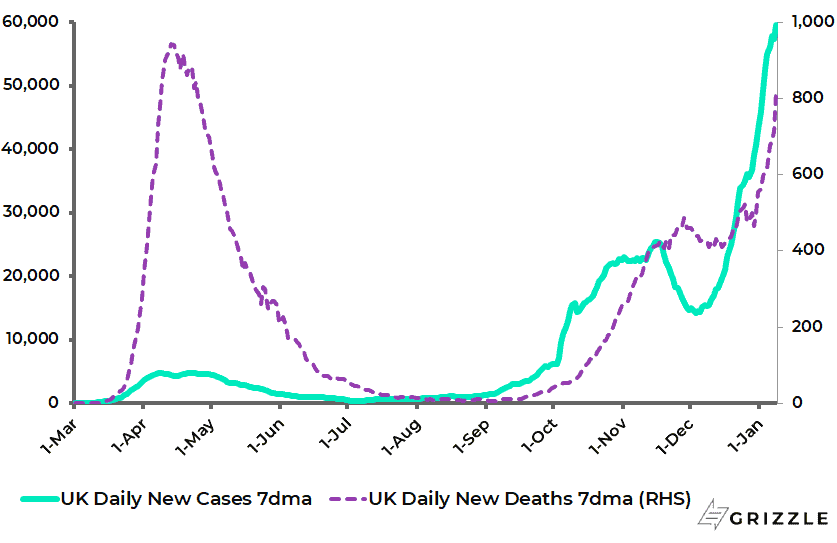

Still, there seems little doubt that the new variant of Covid-19, known as B.1.1.7, is more infectious.

The 7-day average daily case count in the UK has surged more than four-fold from 14,284 in early December to 59,508.

UK 7-day Average Daily Covid New Cases and Deaths

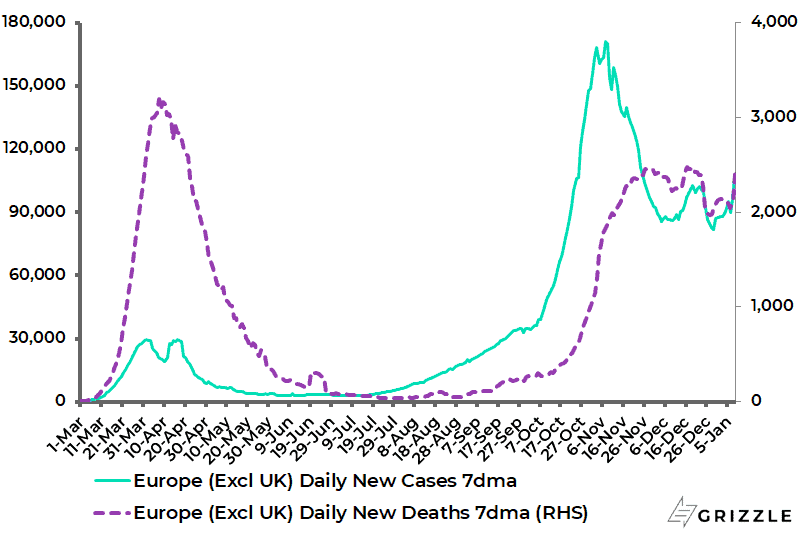

This contrasts with the situation in the rest of Europe where cases are currently running 37% below their second wave November peak.

Europe (ex-UK) 7-day Average Daily Covid New Cases and Deaths

The Rise of the “Passive Put”

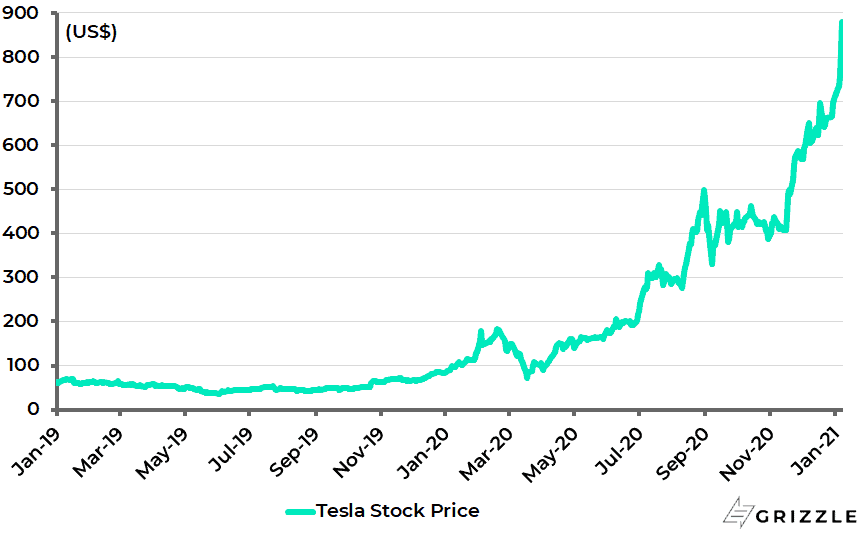

Returning to the markets, the entry of Tesla into the S&P500 on 21 December is a reminder of the ultimate absurdity of the passive investor indexing game in the sense that capital is allocated to an investment just because it is in an index.

And passive funds made up an enormous 48% of assets under management in US equity funds as of March 2020, according to a recent Federal Reserve Bank of Boston study (see Boston Fed working paper: “The Shift from Active to Passive Investing: Potential Risks to Financial Stability?” by Kenechukwu Anadu, Mathias Kruttli, Patrick McCabe, and Emilio Osambela, 15 May 2020).

For the record, Tesla went into the S&P500 at 1.7% of the US$30tn index.

This writer has read estimates that the announcement on 16 November that the company would be included in the index led in the intervening weeks to about US$60bn worth of buying of the stock.

It is further the case that Tesla’s dramatic almost tenfold appreciation since March last year in the run-up to the S&P500 inclusion has also been in part driven by its inclusion in a growing number of fashionable ETFs since the nature of Tesla’s electric vehicle offering means it can be included in ESG and technology-related ETFs, unlike conventional carmakers even if the latter are fast coming out with their own electric vehicle models.

Tesla Share Price

If the indexing phenomenon ultimately leads to gross misallocation of capital as should be expected in such an exercise in investor socialism, it is also an extremely powerful one in the short to medium term; as anybody who has tried to short Tesla knows to their financial cost.

This is why investors now need to factor in what can be described as the “passive put”.

That is in addition to the by now extremely familiar “Fed put” which was given a new lease of life last year by Federal Reserve chairman Jerome Powell, otherwise known as the Reverse Volcker.

The “passive put” is a useful concept to keep in mind going forward.

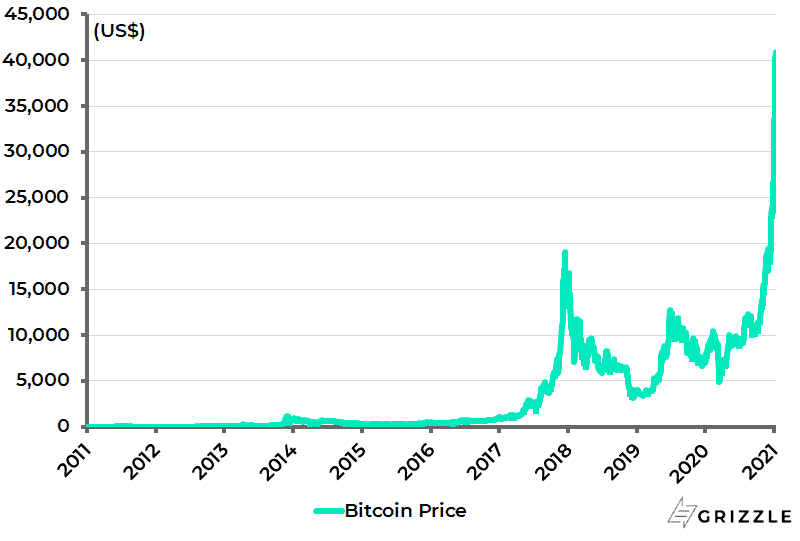

Bitcoin is In Blue Sky Territory

Meanwhile, the long-established trend that investors are driven to invest in a stock the more it goes up in price, and the more “liquid” it becomes, also has extremely bullish implications for Bitcoin.

Apart from the technical “blue sky” created by Bitcoin’s breakout to a new all-time high on 16 December, thereby taking out the old 2017 high, the more liquid trading in Bitcoin becomes the more it is an increasingly viable “store of value” for the many institutional investors, not to mention hedge funds and family offices, who want such a hedge.

Bitcoin Price

In this respect, it is worth again looking at the updated numbers.

The total market capitalisation of Bitcoin is now US$762bn, after its doubling in the last three weeks since breaking the 2017 high last month, which compares with estimates of US$12tn of above-ground gold or indeed the US$659bn market capitalisation of Tesla the day before its S&P500 inclusion.

The Biggest Risk to Shorting Tesla is Bitcoin

With the S&P Index conclusion now completed, the biggest risk to shorting Tesla today is probably that the wonderfully maverick Elon Musk announces tomorrow that he is investing some of his company’s US$14.5bn cash balance as at the end of 3Q20 into Bitcoin.

This is also what any number of cash-rich companies could do, which in America primarily means Big Tech.

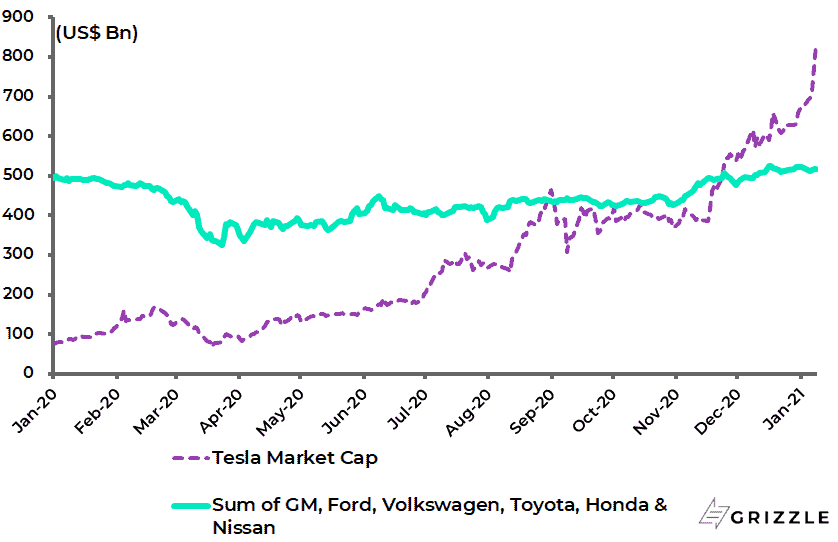

Meanwhile, to return to the long-discussed topic of Tesla’s perceived overvaluation, Tesla’s market capitalisation at the time of S&P500 inclusion was bigger than the combined market caps of Toyota, Volkswagen, General Motors, Ford, Honda and Nissan.

Tesla Market Cap vs Combined Market Cap of GM, Ford, Volkswagen, Toyota, Honda and Nissan

Yet all these companies are now busy investing serious amounts of money in electric vehicles, lured by various incentives, be they subsidies or fines.

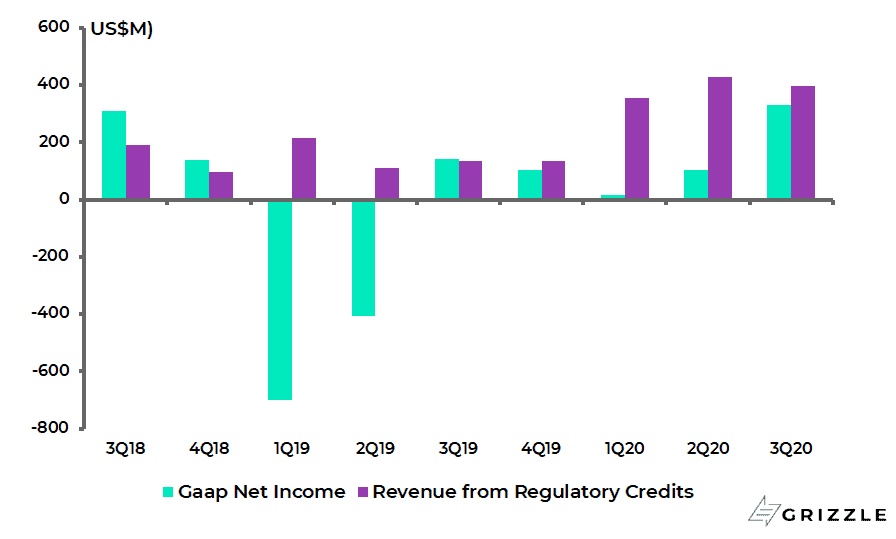

Yet, so far as this writer understands the dynamic, Tesla only generates profits at present by selling tax credits.

So in this respect, as noted in an excellent article in the Wall Street Journal last August, the irony is that Tesla is worth more than most of the industry it relies on for the subsidies that are the only reason it has been able to report five consecutive quarters of profits (see following chart and The Wall Street Journal article: “The Tesla Secret” by Holman Jenkins, 4 August 2020).

Tesla net profit and revenue from regulatory credits

The views expressed in Chris Wood’s column on Grizzle reflect Chris Wood’s personal opinion only, and they have not been reviewed or endorsed by Jefferies. The information in the column has not been reviewed or verified by Jefferies. None of Jefferies, its affiliates or employees, directors or officers shall have any liability whatsoever in connection with the content published on this website.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.