Shares of PayPal Holdings Inc. (NASDAQ: PYPL) declined sharply Thursday after the online payment system reported mixed financial results for its most recent quarter. More critically for investors, PayPal lowered its full-year revenue forecast despite reporting a healthy pickup in new active accounts.

Q2 Earnings Summary

- Earnings: $0.72 per share

- Revenue: $4.31 billion

PayPal’s second-quarter earnings came in at $0.86 per share, topping the median estimate of $0.75 per share. It was the fourth consecutive quarter that PayPal exceeded earnings expectations, according to Zacks.

Where the company ran into some difficulty was in the revenue department. Second-quarter sales were valued at $4.31 billion, missing estimates of $4.33 billion. The company says it expects full-year revenue to be between $17.6 billion and $17.8 billion. Analysts had expected $17.92 billion.

The revised revenue range represents annual growth of 14% to 15%, which is one percentage point below the previous estimate, according to CNBC.

PayPal’s other results were equally mixed. The company’s total payment volume hit $172.36 billion, higher than the $171.49 billion expected. But payment volume for its online app came in at $24 billion, well below the $28 billion expected.

Still, PayPal managed to add nine million new active users last quarter.

Looking beyond the immediate financial results, PayPal is poised to reap the benefits of new business partnerships with the likes of Facebook and Uber. The company is also said to be working on its own blockchain-based payment service, a clear sign it is willing to adopt disruptive technologies instead of fighting them. This is promising given PayPal’s comparatively high fees relative to services like Transferwise.

PYPL Stock Slides

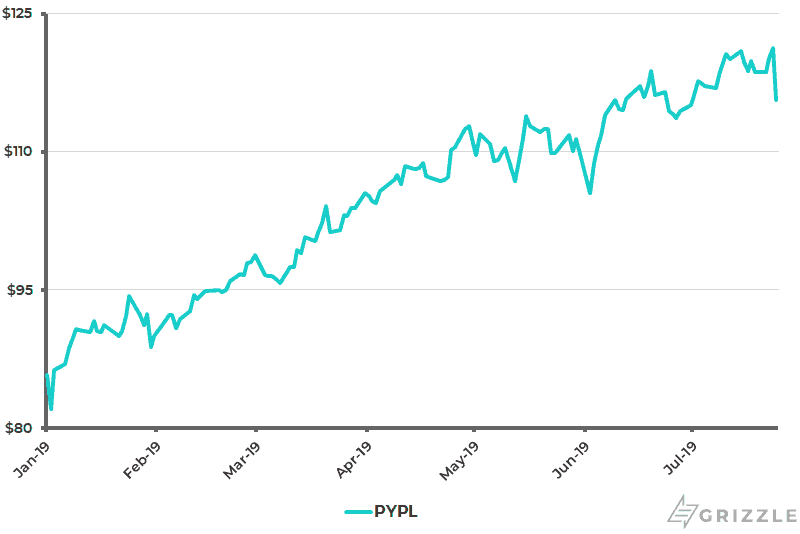

PayPal’s stock price has declined sharply in the wake of the second-quarter earnings call, which was held after the bell on Wednesday. PYPL was down as much as 6% through the first half of Thursday’s session, reaching a low of $113.24. It has since pared some of those declines but is still down more than 4%.

PYPL has vastly outperformed the S&P 500 and Nasdaq, gaining over 40% this year and touching new all-time highs. The stock is up nearly 50% from its December 24 settlement low of $77.06. At current values, the stock has a total market capitalization of $135.7 billion.

Conclusion

In the age of e-commerce, betting against PayPal probably isn’t a good idea. The company is one of America’s leading payment platforms, which means its business will scale with digital commerce. The company’s total payment volume is increasing at a double-digit percentage pace year-over-year, which is a strong sign it is benefiting from the rise of e-commerce.

Disclaimer: Author holds no investment position in PayPal at the time of writing.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.