Digital Fitness Provider Peloton (NYSE:PTON) reported earnings for the quarter ending March 31st that beat expectations while raising guidance for the fiscal year 2020 by 12%.

The stock is up 1% after hours as investors digest solid earnings against forward guidance that the company is essentially sold out of bikes until the end of June at the earliest.

Revenue came in at $524 million, a beat to consensus of $424 million and management guidance of $415 million.

Revenue growth of 65% was down from last quarter’s growth of 77%.

The EPS loss of -$0.20 met consensus. Analysts were looking for a loss of -$0.20.

Management is spending heavily on marketing which is driving sales but also increasing bottom-line losses.

These last two quarters are the best of the year with Christmas gifting, New Years’ resolutions and now people stuck at home because of Coronavirus quarantine.

Peloton now has 886,000 connected subscribers, beating mgmt guidance by 5%.

The growth rate of this business has peaked in our opinion and both the retention rate and losses will continue to disappoint as we move through 2020.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]Peloton has a ton of positive sentiment going for it yet the stock can’t seem to break through the mid-30’s. The stock is too expensive for the profits and subscriber growth it will show in the coming 4-8 quarters. All it takes is one weak growth quarter and this stock is headed much lower. We are not buyers at these levels. [/su_panel]

All the Problems with Peloton

Peloton is an excellent product don’t get us wrong, the problem lies with the stock.

The stock market is pricing Peloton like it takes over the entire North American fitness market replacing most of the gym equipment in homes, hotels and even at the gym itself.

This stock is priced as if a trip to the gym is about to become obsolete.

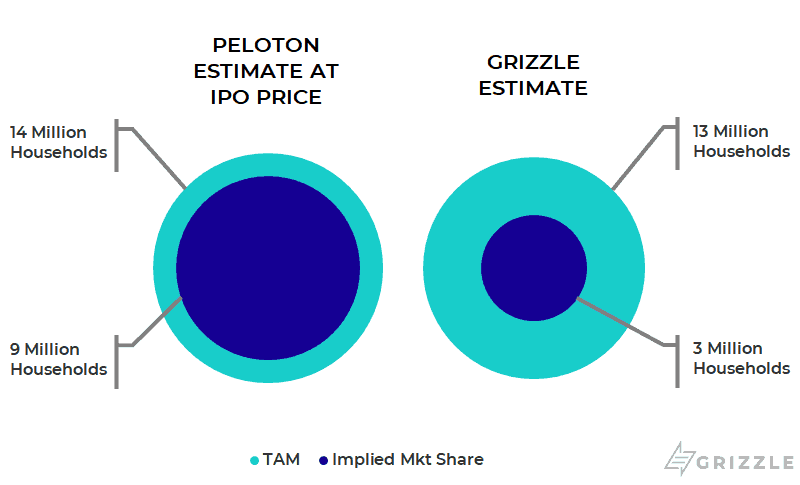

Stock Price Implies 10x Increase in Subscribers

Peloton Priced Like a Major Streaming Platform

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]As a mature (i.e. no growth) streaming company, Peloton would have to maintain a user base of 62 million subscribers paying $12.99 a month to justify the current $13 billion ($37.00/sh) valuation.[/su_panel]| Subscribers Needed to Justify an $11.5 Bn Valuation | |

| Current Market Cap (mm) | ~13 |

| Mature P/E Multiple | 16x |

| Implied Net Income (mm) | $804 |

| Net Income Margin | 8% |

| Implied Revenue (mm) | $9,727 |

| Streaming Cost/Month | $12.99 |

| Total Subscribers (mm) | 62 |

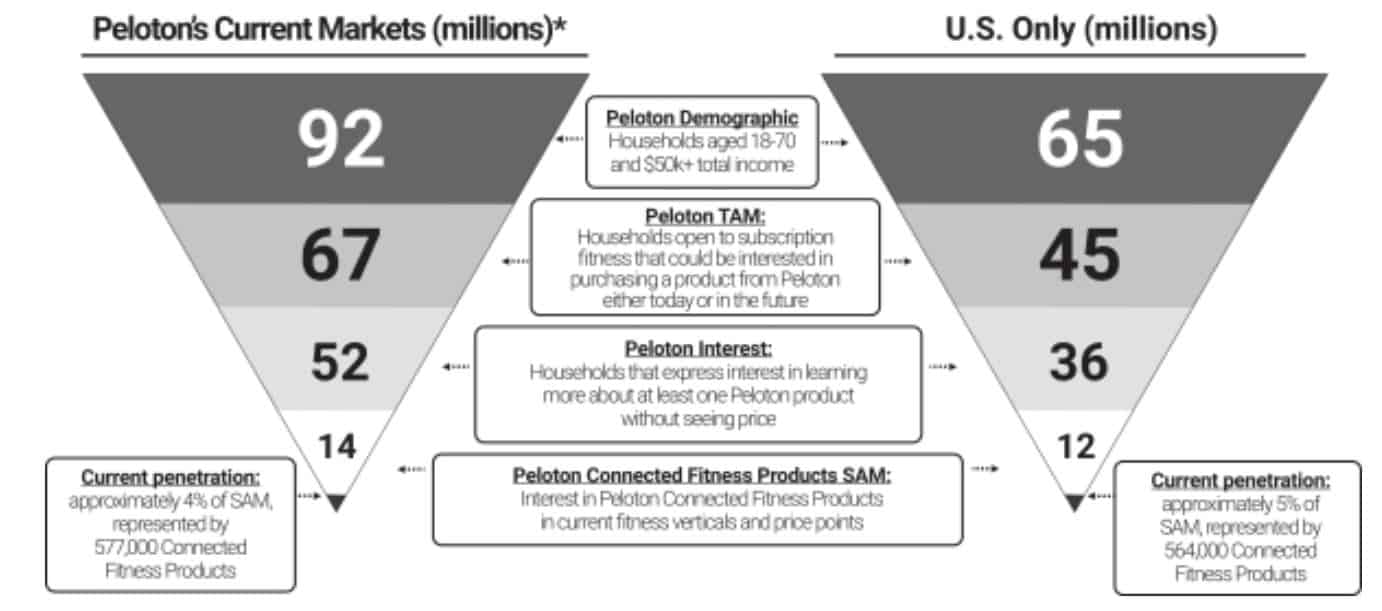

62 million people would represent 95% of gym memberships in America and 92% of the total addressable market according to the company’s own materials.

[su_panel background=”#ebebec” color=”#05011c” border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]62 million would make Peloton larger than Disney+ at 54.5 million and more than half as large as Amazon video at 100 million, both highly unlikely. [/su_panel]

The Quit Rate is Headed Higher and So Are Customer Acquisition Costs

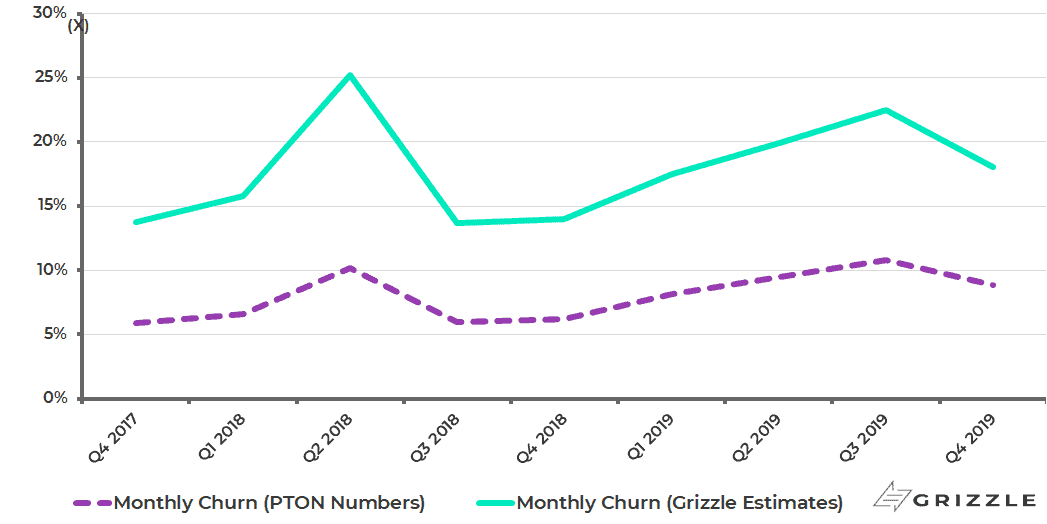

We estimate Peloton has a quit rate of 22%, less than half the industry average. A reversion to the average is ongoing and inevitable.

Acquisition costs are also increasing, growth is slowing and the stock market multiple will fall from 5.6x today to somewhere closer to 2.5x, in line with global fitness peers like TechnoGym.

At that point, investors will be looking at a sub $20 stock, not a $33 stock, and they won’t be happy.

Peloton Price to Sale Multiple Way Above Peers

| Company | P/S | Rev Growth |

| Peloton | 5.6x | 60% |

| Technogym | 2.8x | 13% |

| Nautilus | .1x | 0% |

Our quit rate is higher than what Peloton reports to the market because they count the number of people who quit as a % of this quarter’s subscribers not the subscribers from the period when the users who quit originally signed up.

Say for example you joined Peloton in December with 100 others and quit a year later. Over those 12 months 1,000 more people signed up for Peloton.

By the time you quit Peloton reports you as 1 person who quit out of 1,000 subscribers even though you are 1 of 100 original people to join.

This way of counting understates the quit rate by 90% (1% quit rate vs .1%).

We think the real quit rate is somewhere closer to 22% and rising, much higher than the 11% reported by the company.

This quarter the quit rate decreased to 0.74% from 0.90% last quarter but up from 0.52% at the same time last year.

When Peloton adds a ton of subscribers the churn rate goes down based on the way Peloton calculates it.

The churn rate will continue to march higher.

Peloton Quit Rate

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.