At the end of the day, Peloton is a gym membership pretending to be a tech company.

We fully admit the product is exciting and unique in the market, but Peloton still faces the same problem that keeps every gym owner up at night.

People just don’t stick to a workout schedule.

Peloton is built on a business model that breaks even on the bikes with the hopes that big money is made on recurring monthly fees for digitally distributed classes.

However, with the average gym losing 50% of members within the first year, even the best technology hasn’t proven it can keep people engaged long term.

Peloton has been a smashing success, but at an IPO valuation of $10 billion, the company will have to literally take over the market for investors to avoid a loss.

To justify a valuation of $10 billion, we would have to live in a world where 40% of U.S. households with a gym membership now own a Peloton instead, up from 3% today.

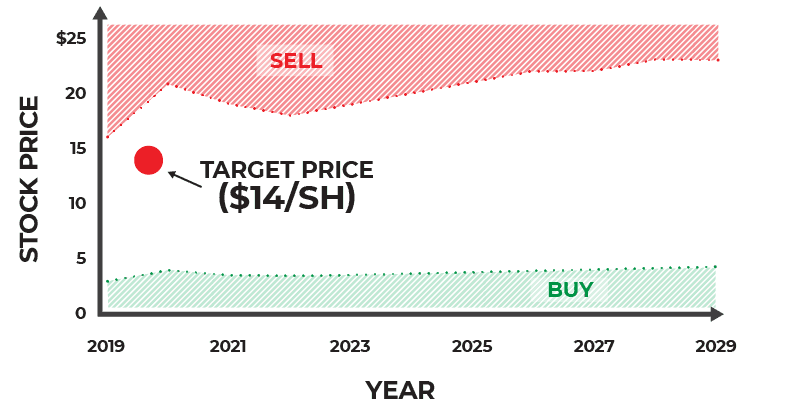

Peloton may be the best piece of home exercise equipment ever invented, but at $29/sh the company is pricing in a penetration rate never achieved in history by a consumer good.

We think the company will struggle as a public company and recommend investors steer clear, or bet on a fall in price as the fundamental value is at best $14/sh and more likely $7/sh.

The Peloton Business Model Explained

Peloton management realized long ago that the exercise equipment game is hard.

For this reason, they built a business model that effectively breaks even on the sale of the equipment hoping that once the bike or treadmill is in your basement you will be easier to hook on a lucrative ongoing monthly subscription.

They are the first company to successfully use technology to digitally beam an exercise class experience to your home.

Thanks to technology, Peloton can now offer half a million people a live spinning experience while only paying for one studio and one instructor. This is economies of scale on overdrive.

However, the Peloton of today still has to deal with the costs of running a large business, which go beyond just a studio and an instructor.

Peloton made about $1,500 on each subscriber in 2019, but because they’ve ramped up headcount and R&D to prepare for public company life, they ultimately lose $870 on every single customer they add.

The key for Peloton is to reach a size where corporate costs per subscriber are dwarfed by the cash generated from equipment sales and monthly subscriptions fees.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]We estimate the company will breakeven by the middle of 2022 once they hit 2 million subscribers, up 300% from 600,000 today. [/su_panel]| Peloton Economics per Subscriber | 2019 |

| Lifetime Value of a Subscriber | $1,280 |

| Cashflow from Bike/Tread | $1,115 |

| Advertising Cost per user | ($921) |

| Cashflow | $1,474 |

| (-) R&D per user | $608 |

| (-) G&A per user | $1,740 |

| Corporate Costs | $2,347 |

| FCF from Equipment and Subscription | ($873) |

Source: Grizzle Estimates

The Smoking Gun: Retention

As much as Peloton management likes to tell us they are revolutionizing exercise through technology, no technology can overcome the problems inherent in the subscription fitness business model.

We’ve all been there.

You sign up for a new gym membership energized by your New Year’s resolution to finally get in shape:

Week 1: “I’m going to crush it” – 4 days at the gym

Week 2: “Crushing it!” – 7 days at the gym

Week 3: “Can’t make it this Thur/Fri because of work drinks” – 4 days at the gym

Week 4: “I’ll go tomorrow” – 3 days at the gym

It’s not your fault, the human brain just seems to have problems sticking to a task, especially exercise.

To drive home the point, we came across a video review of the Peloton Tread done by a writer at website The Verge.

The writer had the motivation of training for an upcoming 5k run, but within two weeks she was already fading on her resolve.

In the final week of the month, she was down to three runs from a peak of six only two weeks before, a decrease of 50%.

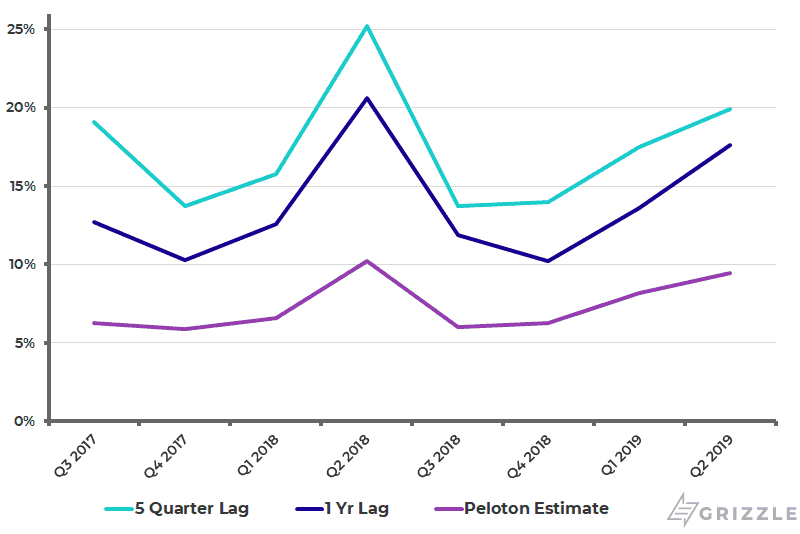

Actual Workout Schedule from The Verge’s Peloton Review

According to the International Health, Racquet & Sportsclub Association (IHRSA), even the best global fitness clubs lose 34% of new members within a year.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]On average the fitness industry has to replace half the customer base each year just to keep membership stable. [/su_panel]

According to Peloton management, the company is absolutely crushing the industry with a retention rate of 93%.

However, digging into how they actually calculate that number we can see some serious liberties are being taken.

Peloton’s attrition numbers (# who cancel) count subscribers who quit in the quarter but divides them not by the number of members who originally joined from that group but by the current membership instead.

[su_panel background=”#C6E1FF” color=”#110076″ border=”px none ” shadow=”px px px ” radius=”4″ text_align=”center” class=”dw-editor-note”]If 100 members joined last Christmas and 20 have quit so far, attrition should be 20%, however, because 400 new members joined recently, Peloton reports retention as 20 lost over 480, or only 4%![/su_panel]Attrition is actually 20% not 7% as Peloton Reports in the S-1

When you look at retention the right way, we estimate Peloton’s retention rate is more like 80% (20% quit over 12 months”.

To Peloton’s credit, 80% is potentially the highest retention rate in the industry.

This means that Peloton is currently losing only 1 in 5 members in the first year compared to a typical gym that loses half their members every year.

Attrition is still a big problem and is the reason why Peloton is not a typical technology disruptor, even though they claim to be.

Attrition requires Peloton to continually spend marketing dollars to replace members who quit, keeping them from building a truly repeatable source of high margin revenue.

We think the attrition rate at Peloton is close to an all-time low and will only go higher.

As the recent blistering growth slows and the company loses some of its high-class cachet due to ubiquity, attrition will increase closer to the industry average.

How Big is Peloton’s Market?

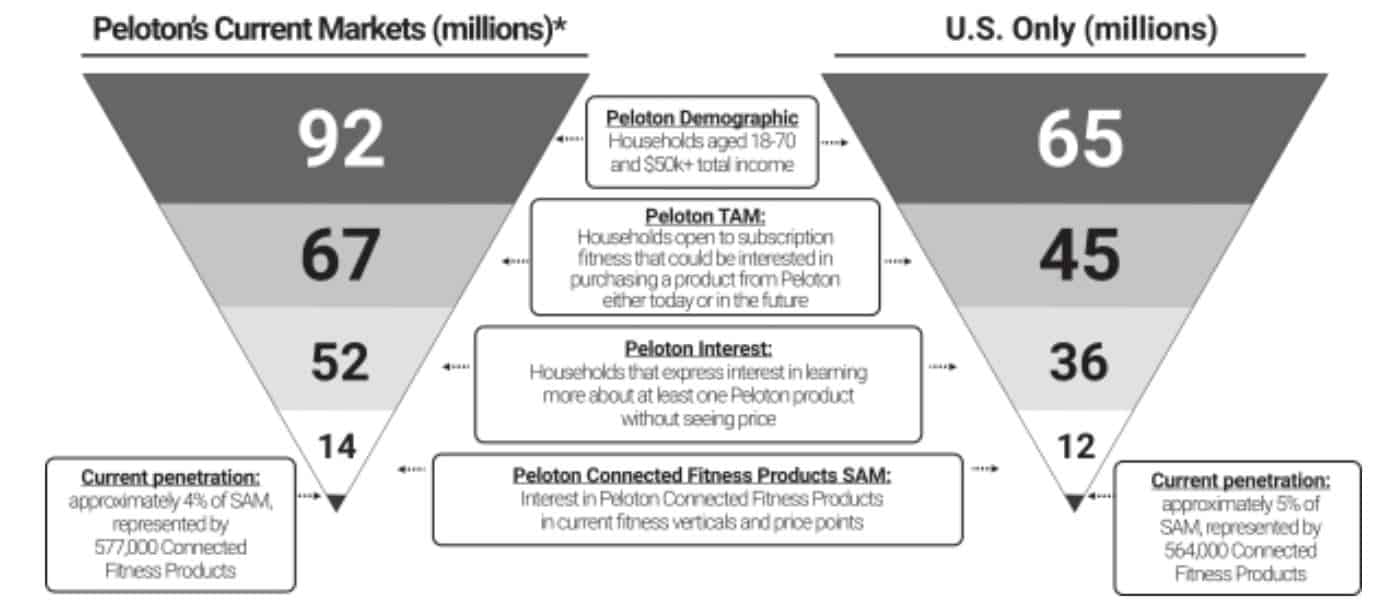

In the IPO filing Peloton estimates their immediate addressable market is 12 million households in the U.S. and another 2 million abroad.

These are consumers directly interested in purchasing a Peloton product.

Even 12 million potential customers is an aggressive goal as it would represent 50% of all U.S. households with a gym membership.

Zooming out even more, management thinks 100% of households with more than $100,000 of disposable income (36 million in the U.S.) have at one time expressed potential interest in a Peloton product and could be future customers.

Peloton is effectively telling us they think every person with a gym membership could one day own a Peloton.

Possible but highly unlikely.

Peloton’s Estimate of Market Size

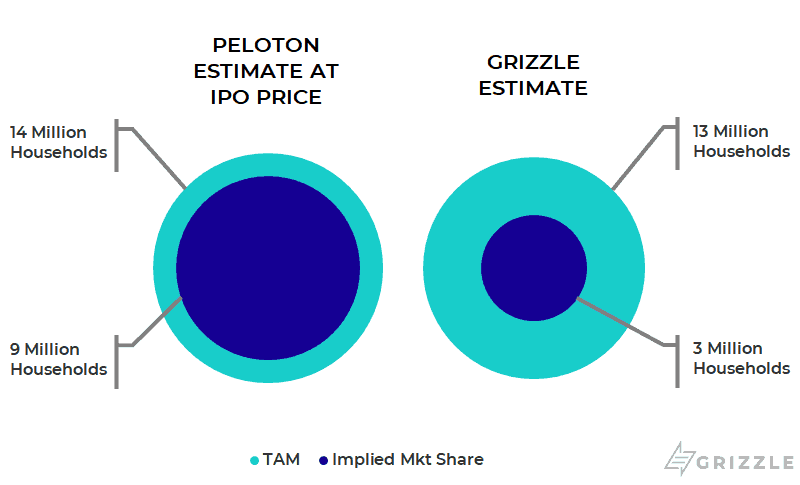

Throwing out what management wants us to think, our preferred market potential is based on annual sales of exercise equipment.

According to the Sport & Industry Fitness Association (SFIA), $5.5 billion of similar exercise equipment was sold to consumers and gyms in 2018.

We estimate sales will grow to $7.5 billion by 2030.

We are talking bikes, treadmills, ellipticals and any other equipment that could likely be replaced with a Peloton.

To justify a $29/sh stock price, Peloton would have to capture 83%, or $6.2 billion of retail and gym equipment sales, in effect upending the entire gym ecosystem.

There is no way this is going to happen.

Even if we looked at the entire equipment market, worth $10.5 billion, Peleton would need a market share of 60% to be worth $29/sh.

We think the company can realistically capture 30% of its addressable equipment market, up from their current market share of 16%.

Market Size Estimate, Peloton vs Grizzle

A $10 billion Dollar Company Peloton is Not

If Peloton goes public at the indicated offering price of $27-$29/sh, it would value the company at almost $10 billion dollars.

Whichever way you look at value, relative to other stocks or on a fundamental basis, Peloton is overpriced.

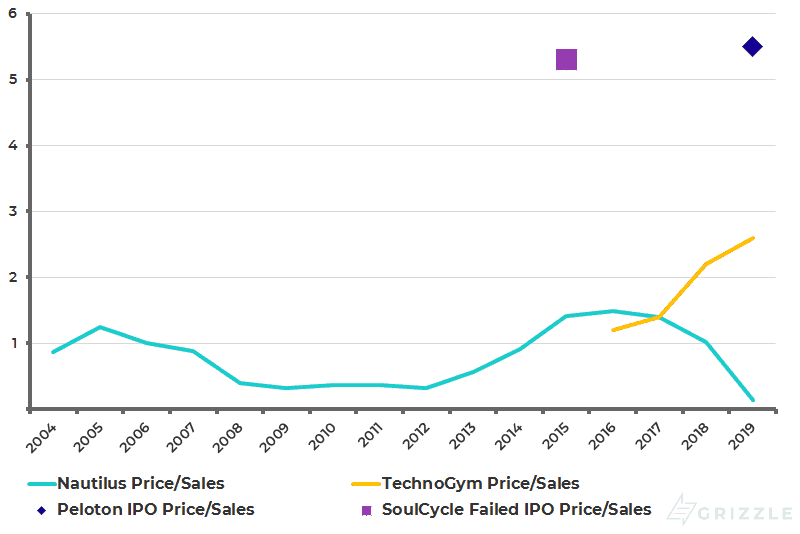

If we compare Peloton’s forward price to sales multiple to peers, it’s coming out of the gate at a premium price.

Nautilus (NYSE: NLS), one of the only publicly-traded competitors to Peloton has never traded above 1.5x next year’s revenue even when it was growing at 25-30% a year.

SoulCycle, another private competitor, attempted to go public in 2015 at a price to sales of 5.3x, but the IPO never found enough buyers and was scrapped for good in 2018.

Peloton is hoping investors have short-term memory loss as it looks to be trying for a valuation that previously fell flat with investors.

From a relative value approach, Peloton is worth far less than $10 billion.

Forward Price to Sales of Peloton and Competitors

Looking at the value of Peloton on a fundamental basis, we also struggle to get anywhere close to $29/sh.

Based on the exercise equipment market we defined in the section above, there is $7.5 billion of sales up for grabs by 2030.

If as we expect, Peloton achieves a 30% share in its market or $2.3 billion in annual sales, the stock is only worth $14.00/sh, 50% lower than the IPO price.

Below is a chart showing the buy and sell bands for this stock over time.

Though we think Peloton is only worth $14/sh at most longer-term, if you do decide to trade Peloton use this visual guide to determine when you should buy, sell or hold.

Visual Guide to Investing in Peloton

A Look the Capital Structure

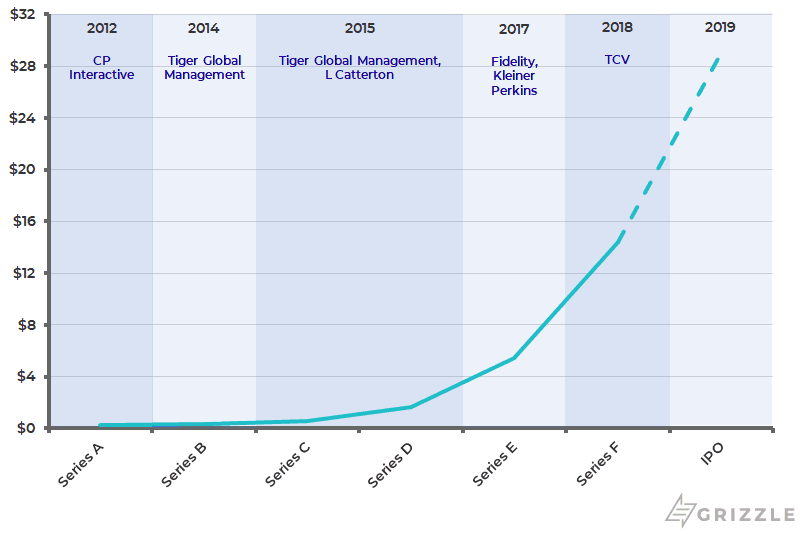

Peloton has been through six funding rounds raising $940 million.

The latest round, series F raised $550 million in August 2018 at a price of $14.44/sh.

The $29/sh IPO price is a huge jump from the last funding round which will likely create some uncertainty among institutions if $29/sh is a fair price for the stock.

Between all six rounds, insiders have an average cost basis of only $4.51 with 25% of shares issued at only $0.45/sh. Insiders are sitting on 6x-64x returns.

Peloton Funding Rounds

Lockup Expiration Details

181 days after the stock registration becomes “effective”, the majority of insider shares can now be sold. This date falls on March. 24, 2020.

Under certain circumstances the lock-up period will expire 120 days after the filing of the S-1, falling on Jan. 24, 2019.

Given the low cost basis of insiders, we expect at least some of the 84 million shares issued below $0.50 will be sold once the lockup expires.

The impact on the stock will all depend on short interest and the daily volume at the time.

Wrapping it All Up

Peloton has truly come closer than any other product to bringing the gym experience into your own home.

But though the product may be amazing, it requires significant ongoing commitment from the customer.

Consumers rarely stick with exercise goals and for that reason, Peloton has to work harder and harder just to maintain revenue let alone grow it.

For this reason, we think Peloton will struggle as a public company.

Once investors realize Peloton is on the New Year’s resolution treadmill just like every other exercise company, both the multiple and the stock price have a long way to fall.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.