Bottom Line

Ever since we identified this ‘fantasy fitness’ company, we knew it would not end well, yet even we were surprised this quarter by how little time it took for growth to start slowing.

Peloton is attempting to support an astronomical $8.6 billion valuation and that requires perfect execution.

Execution is not what we got, however, with revenue beating slightly, but the company guiding to lower gross margins this coming year and revenue that was 10% below what we were expecting, and we are negative on this stock!

As a result the stock is down about 5% as we write this.

New guidance released with earnings implies a 15% lower stock price longer term than we were already assuming, not a good first look as a public company.

High flying stocks like Peloton can never escape the law of gravity no matter how hard they try.

When investors expect global fitness domination as they do today, even if Peloton becomes a very successful fitness platform it won’t be nearly enough to keep the stock price above $20/sh.

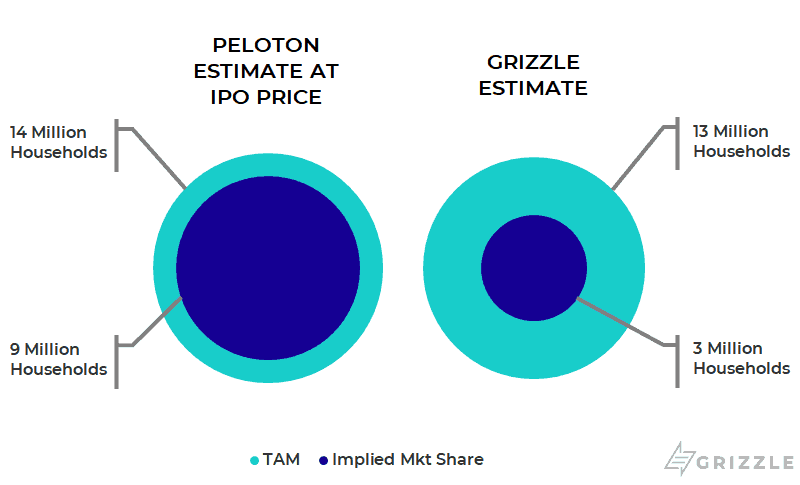

Stock Price Implies 10x Increase in Subscribers

Quarter after quarter, year after year, we are going to see subscribers quit the platform in larger and larger numbers.

We estimate Peloton has a quit rate of 22%, less than half the industry average. A reversion to the average is ongoing and inevitable.

Acquisition costs will increase, growth will slow, and the stock market multiple will fall from 5.8x today to somewhere closer to 2.5x, in line with global fitness peers like TechnoGym.

At that point investors will be looking at a $6 stock, not a $26 stock, and they won’t be happy.

| Company | P/S | Rev Growth |

| Peloton | 5.9x | 60% |

| Technogym | 2.8x | 13% |

| Nautilus | .1x | 0% |

Important Takeaways From the Earnings Report

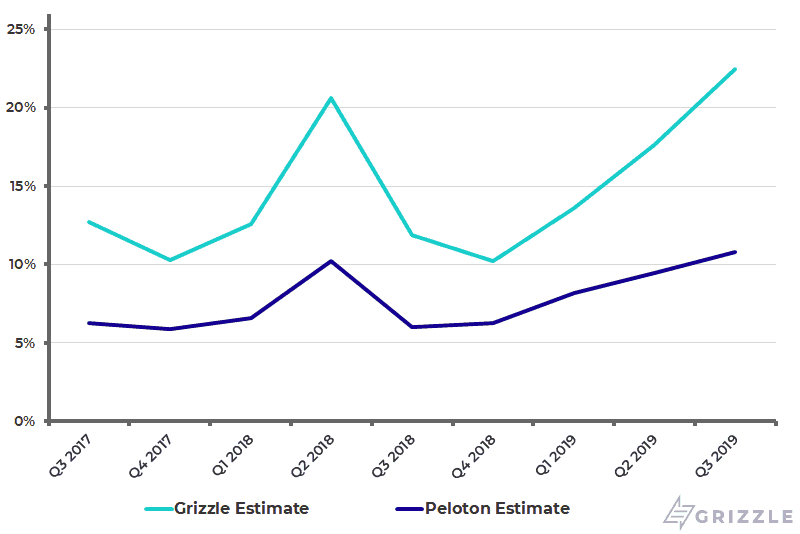

Investors should be most concerned this quarter with the rising quit rate.

More customers quitting means the company will receive less months of high margin subscription revenue and must spend more on advertising to bring in new subscribers.

The company expects next quarter’s quit rate to be up 80%+ from the year before, so this trend will continue.

On cue, acquisition costs this quarter hit $1,044 per subscriber this quarter, up 15% from the same period a year ago.

Higher acquisition costs equal higher marketing costs equal lower profit margins.

Peloton Quit Rate

Growth is also slowing with revenue guidance for next quarter looking at only 60% growth compared to 103% this quarter.

Slowing growth will likely continue as they saw huge results in the last few quarters leading up to the IPO from a boost in advertising and word of mouth due to media coverage of the IPO.

Peloton is priced to perfection and the company needs growth to continue at a torrid pace coupled with strong profitability just to keep the stock above $20/sh.

A price to sales multiple far above any competitor doesn’t help.

This multiple will definitely fall over time creating a headwind to the stock that only faster revenue growth can overcome.

What to Do With the Stock

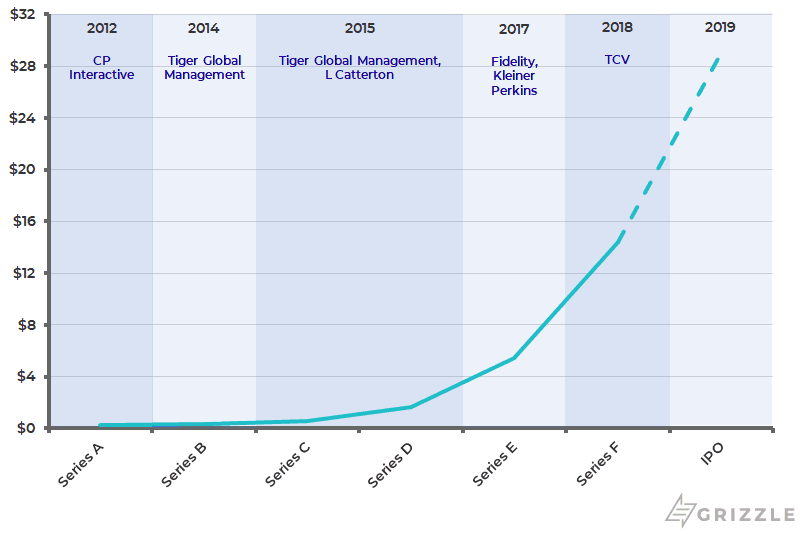

Peloton investors now have to contend with a share unlock coming on either Dec. 26 or Feb. 24, 2020, depending on certain circumstances.

The cost basis of insiders is only $4.51 as a whole with 25% of shares with a $0.45 cost basis. We think it’s likely some insiders want to lock in these huge gains once the lockup expires, putting additional downward pressure on the stock.

History of Funding Rounds

The share unlock will provide an opportunity to put on a cheap bet against a stock whose fundamentals currently look as good as they will ever get in our view.

Investors who can’t bet against this stock should continue to steer clear, while those who want to go short will have the share unlock and weakening fundamentals on their side.

Full Disclosure: The author sold shares of PTON short after conducting extensive due diligence on the stock.

The opinions provided in this article are those of the author and do not constitute investment advice. Readers should assume that the author and/or employees of Grizzle hold positions in the company or companies mentioned in the article. For more information, please see our Content Disclaimer.